The Thesis Driven Innovation 100, 2026 | #51-100

Meet the 100 people shaping the future of the built world

Meet the 100 people shaping the future of the built world

A 90-minute tactical workshop for real estate professionals and vendors who want to get the most out of conferences

After years of false starts and regulatory confusion, a few serious projects are pointing toward what this technology can actually deliver for real estate

Rising rates have made development increasingly challenging. What’s happening in the market now and what role can innovation play?

Today’s Thesis Driven is a guest letter by Jonathan Scherr, founder & CEO of Juno. A special thanks to Emily Mills Marineau and Natasha Sadikin, to Meg Spriggs at Lendlease, and to Dave Chattman at Related for their contributions.

2023 marked one of the most challenging environments for institutional real estate development. While big tech has kept the stock market surging, a slow-forming crisis has been looming over ground-up development. On the heels of one of the most aggressive interest rate increases in recent history, large-scale apartment development is down nearly 30% from this time last year and commercial property values have been softening meaningfully toward the end of the year. The real estate development industry spent much of the past year struggling to make any projects work, and few actually got there.

As we turn the page into a new year, we’ll break down some of the fundamentals of ground-up multifamily development and why 2023 was so challenging. In this letter, we will:

I will be simplifying a lot in this letter, so I’ll ask for forgiveness from real estate development professionals for any oversimplification.

The role of risk

It may sound obvious, but development (the act of creating a building from scratch) is riskier than buying a building that already exists, which means it needs to command a higher return for that risk. When investors buy a building, they literally have an asset that has some value. But developers merely start with a piece of raw land. That land must get permitted, a building needs to get designed on top of it, and a general contractor (and subcontractors) need to build the building on budget and on time.

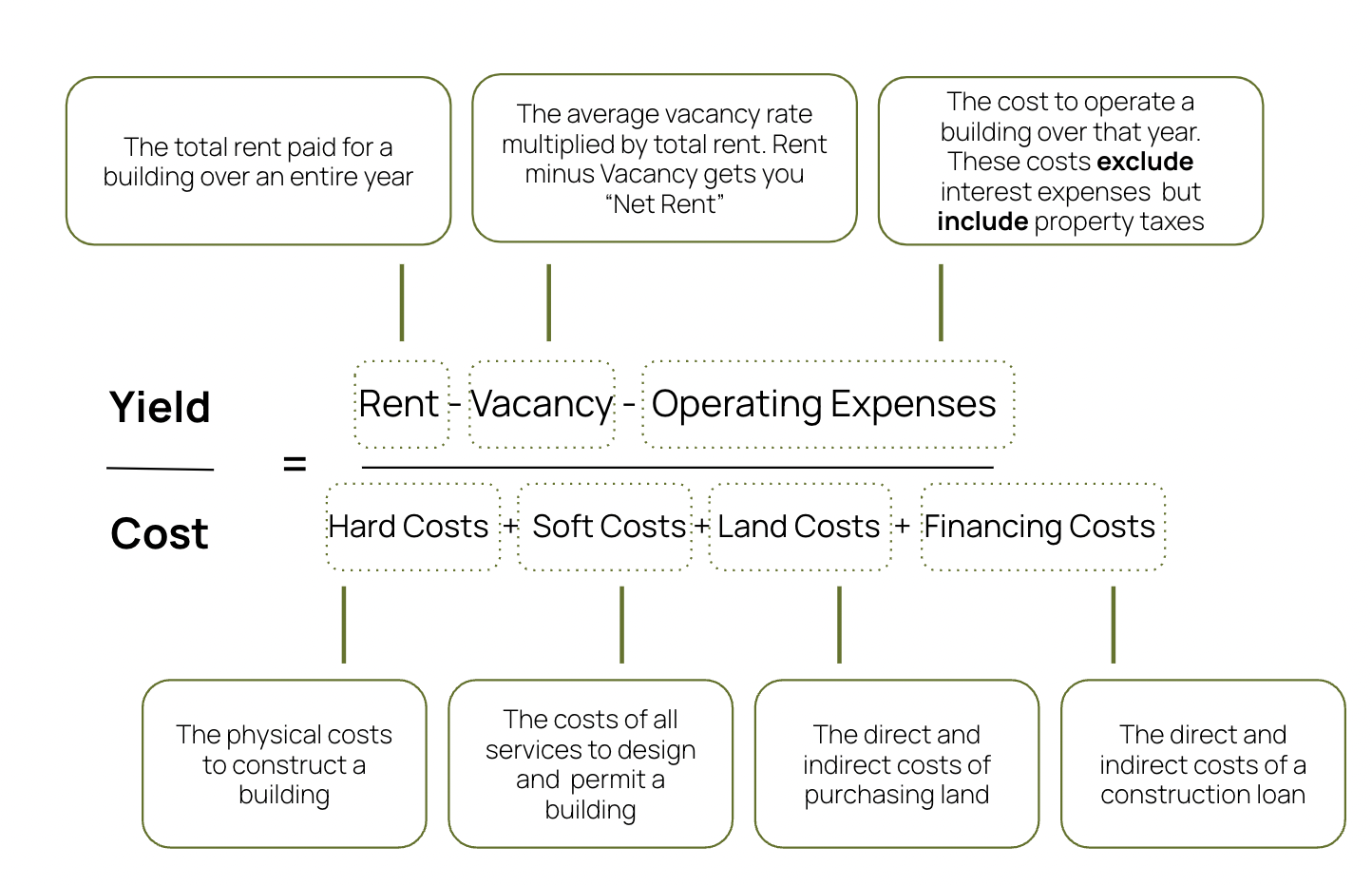

Developers and their investors consider many different metrics when they evaluate a development opportunity, but the primary metric that developers consider is Yield-on-Cost (YoC). Yield-on-Cost is the income a building will produce divided by the all-in development costs to achieve that income. It doesn’t consider how much of a mortgage the property has, but rather just looks at how well it will perform relative to the cost to get that performance.

In a simplified way, the YoC equation is as follows:

Let’s take an example of a 100-unit apartment development that a developer may consider building with the following assumptions:

After years of false starts and regulatory confusion, a few serious projects are pointing toward what this technology can actually deliver for real estate

Developers have more options than ever to capitalize early deal expenses. Here's why that matters.

Can a new lease securitization concept solve the OpCo capitalization problem?

Covering the future of real estate and the people creating it