Timber's Fastest Asset

World Tree Technologies is using a quick-growing hardwood to compress decades-long timber cycles into an investable real estate timeframe

World Tree Technologies is using a quick-growing hardwood to compress decades-long timber cycles into an investable real estate timeframe

The investor intelligence platform for GPs raising capital from PERE, family offices, and RIAs. Now with a live API, real-time Signals, and direct CRM integrations.

World Tree Technologies is using a quick-growing hardwood to compress decades-long timber cycles into an investable real estate timeframe

Signal Line Partners is leading a capital formation effort to bring institutional and family-office capital into the World Tree platform. On July 8, Signal Line partner and former Invesco CIO Darin Turner will join Thesis Driven for a live session exploring the opportunity. Register here.

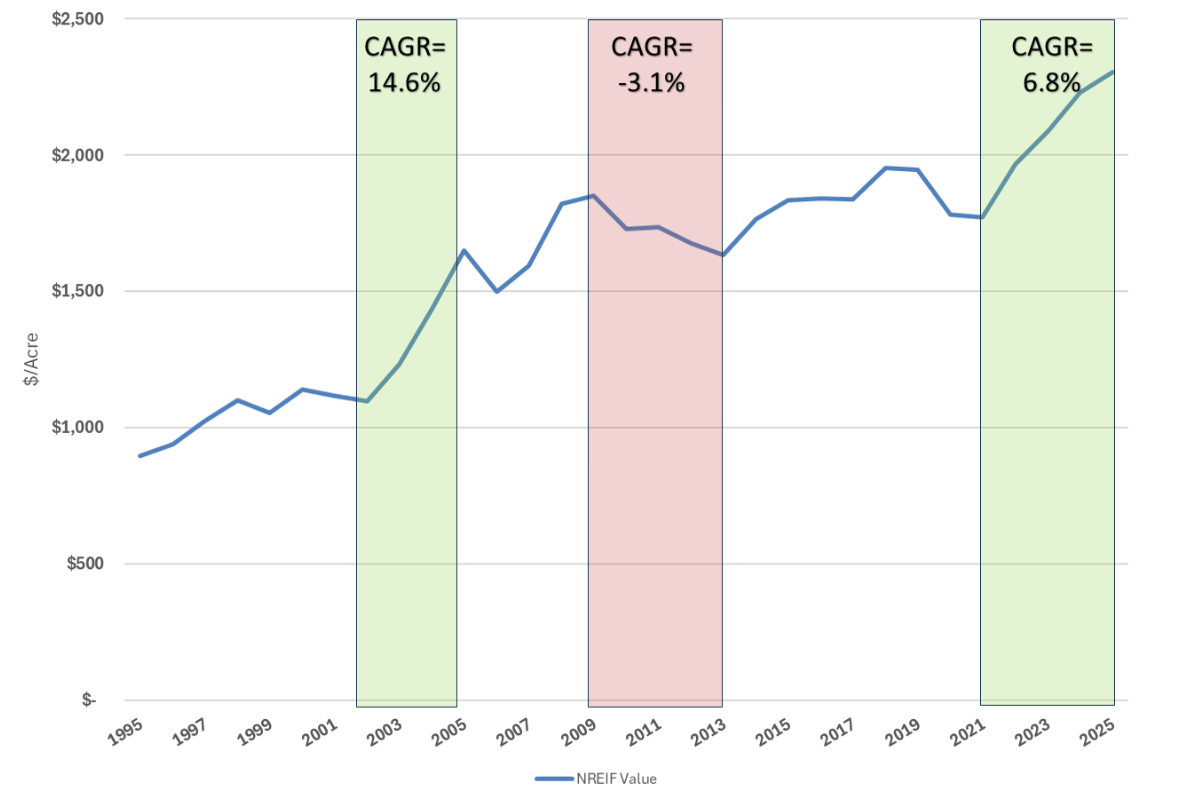

For more than three decades, timberland has been a fixture of institutional portfolios, and for good reason. The NCREIF Timberland Index has delivered annualized returns above 8 percent with low correlation to public equities, fixed income, and conventional real estate, a combination that is genuinely rare among real assets.

Endowments and pension funds have allocated to it for decades, but family offices and high-net-worth investors, for the most part, have not. The reason is straightforward: time.

That is beginning to change. World Tree Technologies, a Hermosa Beach, California company, has spent the past decade commercializing paulownia, a hardwood genus native to East Asia and cultivated there for more than two thousand years. The trees grow 10 to 20 feet in a single year, reach harvestable size in 8 to 12 years, and regenerate from the stump after cutting for as many as five to seven additional harvest cycles without replanting. The wood carries a Class A fire rating under ASTM E84 without chemical treatment, weighs one-third as much as oak, and is dimensionally stable and naturally water-resistant.

Japanese craftsmen have used it for furniture and cabinetry for centuries. What has been missing is supply at institutional scale in the Western Hemisphere.

World Tree has assembled 8,000 acres across 375 farms in five countries, developed 25 to 30 proprietary genetic varieties across three research labs and seven nurseries, and built a commercial sales pipeline that delivered its first large-scale harvests in late 2025.

Signal Line Partners, led by former Invesco CIO Darin Turner, is leading the capital formation effort behind World Tree's expansion into institutional and family-office markets.

This letter covers:

Timber's return mechanics are straightforward.

Investors fund the planting and management of trees, which accumulate biomass that translates directly into board feet of merchantable lumber, realized as revenue at harvest. Unlike a building, which appreciates based on market forces largely outside the owner's control, a standing forest adds 2 to 8 percent in biological volume every year regardless of whether the economy is expanding or contracting. A forest, in other words, grows its own value.

That biological return, layered on top of commodity pricing at harvest, is what makes timber perform well across economic cycles. In recessions, trees keep growing. In inflationary periods, lumber prices rise alongside construction costs. The NCREIF Timberland Index has delivered consistent risk-adjusted performance for more than 30 years, and timber has functioned as a portfolio hedge during every major downturn since the early 1990s.

Timber Investment Management Organizations, known as TIMOs, including Hancock, Weyerhaeuser, and Merrill & Ring, manage tens of billions in timberland for endowments, pension funds, and sovereign wealth funds. They operate on 20 to 40-year rotation cycles with minimum allocations in the tens of millions, placing the asset class well beyond the reach of most private capital.

A family office that plants red oak today will not see a harvest until the 2050s. The capital is illiquid, the biological risk compounds annually, and the generational timeline means the investors who fund the planting may never be the ones who realize the return. The product, in other words, is attractive. The terms have been prohibitive.

Paulownia elongata, the species at the center of World Tree's program, grows 10 to 20 feet in its first year and reaches harvestable size in 8 to 12 years, roughly one-third the rotation of conventional hardwoods. After harvest, the tree regenerates from the stump through coppicing, sending up new shoots that grow to the next merchantable log. Independent forestry literature documents five to seven harvests from one root system, with each subsequent rotation shorter than the last because the established root mass drives faster regrowth.

What separates paulownia from other fast-growth species such as eucalyptus and hybrid poplar is its commercial profile. Both grow comparably fast but eucalyptus and poplar produce pulp and biomass rather than quality lumber. Paulownia yields a genuine specialty hardwood suited to furniture, cabinetry, siding, musical instruments, and marine and acoustic panels. It weighs one-third as much as oak, shrinks less than half as much under dimensional stress, resists moisture naturally, and carries a Class A fire rating under ASTM E84 without chemical treatment, making it a direct substitute for cedar, ash, and redwood in construction and millwork.

"Paulownia is the fastest-growing tree that produces a quality hardwood," says Doug Willmore, CEO of World Tree Technologies. "Eucalyptus grows fast but makes pulp. Poplar grows fast but makes pallets. Paulownia grows fast and makes furniture and siding. That distinction is what makes our business so exciting."

The addressable end markets are substantial. U.S. wood furniture is a $92 billion industry; global musical instruments reach $17.5 billion; and U.S. boatbuilding adds another $15.5 billion.

World Tree's realized sale prices are running at or above $5.89 per board foot, and specialty applications such as surfboard cores fetch as much as $18. One acre of paulownia can sequester up to 15 tonnes of CO2 per year, roughly 10 to 15 times the rate of typical U.S. forest land. Carbon is not the primary revenue driver, but the sequestration profile adds optionality as embedded-carbon accounting frameworks mature.

The combination of commercial-grade wood quality and a sub-12-year rotation makes paulownia the first timber species that can be underwritten within a traditional real estate investment horizon.

World Tree is the largest commercial grower of paulownia in the Western Hemisphere, a position it has built over nearly a decade of planting, genetic research, and commercial development.

Planting began in 2016, and the company now manages more than 8,000 acres across 375 farms in five countries: the United States, Mexico, Costa Rica, Guatemala, and Vietnam. The stated tree portfolio is valued at $300 million, with 27 staff across all operations. The first commercial lumber delivery shipped in December 2025, and large-scale harvests are underway this year.

The company's competitive moat is genetics. Genotype-to-site matching is the dominant driver of survival in plantation forestry. Nine years of proprietary research across three labs and seven nurseries has produced 25 to 30 site-specific varieties, each a clonal selection matched to the soil, climate, and altitude conditions of a particular farm, generating a survival rate of 88 percent.

"Our real business is genetics," says Willmore. "If the wrong variety goes into the wrong site, survival drops and the economics fall apart. Getting that match right, consistently, across five countries and hundreds of individual farms, is what took a decade to build. It is not something a competitor can replicate by planting trees."

The commercial pipeline is taking shape. Vintage Woods has signed and placed its first order, and Thermalwood Canada, Glacier Millworks, and Windsor One are in late-stage negotiations, representing more than $5 million in potential annual revenue.

Investors can access the World Tree platform through two structures. The first is equity in the operating platform itself, which carries exposure to three revenue streams: management fees ranging from $400 to $3,000 per acre contracted monthly, development fees of 3 to 5 percent per project at close, and a profit share of 18 to 25 percent of lumber proceeds at harvest.

The company projects approximately $224 million in aggregate revenue through 2035, with exit paths including acquisition by major timber companies, lumber producers, and private equity buyers.

The second structure is the Eco-Tree Program, a Reg D offering through which investor capital funds specific paulownia farms and shares in harvest proceeds.

Farmers take 50 percent of gross profits (harvest revenue less harvest costs, as defined in the PPM), and investors receive the greater of 30 percent of gross profits or a full return of their capital, whichever is larger, with World Tree earning the remainder. The target return is 6 to 7 times invested capital, with distributions beginning in years 8 to 12 following harvest and sale. The minimum investment is $50,000, with volume-tier pricing available at higher commitment levels.

Both structures carry potential tax advantages. Eco-Tree investors may receive passive loss deductions estimated at approximately 55 percent of their investment over 10 years, and investments are eligible for Donor-Advised Funds and Self-Directed IRAs.

"Family offices keep telling us the same thing," says Darin Turner of Signal Line. "They want exposure to timber, they understand the asset class, but they have never seen a vehicle that fits their timeline or their check size. That is what this platform was designed to solve."

Global lumber demand is projected to quadruple by 2050, and the supply side is already under significant stress. U.S. hardwood production has fallen an estimated 20 percent since 2023 on sustained mill curtailments and closures. Emerald ash borer has killed tens of millions of ash trees across the eastern United States, western red cedar faces widespread disease, and 95 percent of original old-growth coast redwood is gone. Lumber futures in January 2026 traded at $614 per thousand board feet, 75 percent above pre-2019 averages.

In the time it takes cedar or redwood to produce a single harvest, a paulownia acre can be cut three or more times from the same root system, producing several times the board feet per decade while the species it competes with grow scarcer and more expensive.

The addressable North American market across construction, millwork, furniture, cabinetry, musical instruments, marine, and siding totals approximately $170 billion.

"We planted eight thousand acres over the past decade because we knew the conventional species would not keep up with demand," says Willmore. "The first harvests are happening now, and every year the gap between supply and demand gets wider."

Meet the 100 people shaping the future of the built world, Part III

Meet the 100 people shaping the future of the built world, Part II

Why the next generation of real estate fund managers will be built on video reels and newsletters

As the spigot of institutional capital remains dry for many real estate sponsors, family offices have become an increasingly sought-

Covering the future of real estate and the people creating it