CapitalStack 2.0: 7,500 Real Estate Investors, Piped Directly Into Your CRM

The investor intelligence platform for GPs raising capital from PERE, family offices, and RIAs. Now with a live API, real-time Signals, and direct CRM integrations.

The investor intelligence platform for GPs raising capital from PERE, family offices, and RIAs. Now with a live API, real-time Signals, and direct CRM integrations.

One founder's account of the structural reasons autonomous AI property management SaaS gets crushed, and what the right model actually looks like

Every accepted attendee at the August 4 Capital Markets Summit gets a dedicated concierge to schedule investor-operator meetings before you arrive

The asset class tapping the $20 billion US camping market is entering its next phase

Don’t miss Thesis Driven’s Buy Box Roundtable for accredited & institutional investors on Outdoor Hospitality next Wednesday, June 25th featuring investors & entrepreneurs from the industry. Register here.

Few travel experiences stir the imagination—yet feel logistically out-of-reach—quite like waking up steps from a pristine ridge line, coffee in hand, with Wi-Fi strong enough for a 10 a.m. Zoom.

The Kampgrounds of America (KOA) 2024 Camping & Outdoor Hospitality Report counts 75 million U.S. households that camped at least once last year, up roughly 11 million since 2019. Yet the vast majority still pitch tents on uneven ground, use BYO bathrooms, and hope the weather cooperates—conditions that limit length of stay and keep many would-be guests at home.

Historically, those comfort gaps—and the zoning, utility, and cap-ex hurdles needed to close them—have throttled growth. Building roads, septic, and 100 keys of hard lodging in sensitive environments can cost as much per room as a select-service hotel while still earning lower average daily rates (ADRs). Meanwhile, “glamping 1.0” operators discovered that Instagrammable tents alone don’t guarantee repeat visitation or double-digit yields once novelty fades.

But the new generation of “Outdoor Hospitality 2.0” operators are going all-in, offering immersive nature experiences that build on the successes–and aim to address the shortcomings–of prior iterations. On one end, large upscale concepts like Sojourner are designing fully serviced, four-star retreats built around nature as the core amenity experience. On the other, brands like Ramble are developing nature-focused campgrounds with turnkey design and amenities that appeal to modern campers.

In both cases, these operators are doubling down on what the 1.0 wave hinted at: that nature, if done right, is not a novelty but a repeatable, defensible asset class.

With ~16,000 privately owned U.S. campgrounds—and the largest US brand (KOA) at just 3% market share with ~500 campgrounds under their brand umbrella—there’s reason to believe the outdoor hospitality market has significant room to run.

Today’s Thesis Driven letter will explore:

Thesis Driven is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

A roadside franchise and a cartoon bear. The modern camping industry took shape in the early 1960s, when a Billings-based entrepreneur spotted a stream of road-trippers headed for the Seattle World’s Fair and started charging $1.75 to pitch a tent on the banks of the Yellowstone River. He called the concept Kampgrounds of America, or KOA. By standardizing hook-ups, bathrooms and a little camp store, KOA proved that travelers would pay for predictable comforts in the wild, and it grew quickly through franchising to become the country’s first national outdoor-lodging brand.

Not long after, Wisconsin motel owner Doug Haag asked what would happen if a campground felt less like a roadside pit-stop and more like an all-ages resort. The answer was Yogi Bear’s Jellystone Park Camp-Resorts (1969), a network that layered mini-golf, pools and Saturday-night hayrides onto the KOA template—and showed that theme and programming could nudge families to stay a week instead of a night.

For the next three decades, however, the product barely evolved. Pads of gravel, communal bathhouses and bingo under the pavilion remained the norm. As land prices crept up and labour tightened, many mom-and-pop owners under-invested, and the category ceded share to rapidly expanding select-service hotels and, later, to DIY vacation rentals that offered four solid walls and private bathrooms. By the early 2000s the campground business was sizable—roughly a $20 billion domestic spend—but stagnant: fragmented ownership, thin margins and little brand innovation kept institutional investors at bay.

Around 2010, Instagram—and a restless millennial cohort—changed the calculus of the old-school campground model. A handful of start-ups inserted design, privacy and curated food into the gap between rustic camping and budget hotels.

Emerging from the pack of mostly mom-and-pop operators were AutoCamp, Under Canvas, and Getaway. Under Canvas pitched safari tents near national-park gates; AutoCamp lined up polished Airstreams under redwoods; and Getaway (now Postcard Cabins) scattered tiny cabins within a two-hour drive of major metros. Guests gladly paid hotel-level ADRs for a “bucket-list” night under the stars, validating both price and demand.

Each brand scaled beyond its original locations, cultivated brand loyalty, attracted institutional growth capital, and formed strategic partnerships with major hotel chains.

In 2018 KSL bought a controlling stake in Under Canvas and later injected a further $25 million for expansion. AutoCamp secured a $115 million growth round from Whitman Peterson to roll out its Airstream-and-cabin model nationwide (AutoCamp was also the first of the three to form a strategic partnership with Hilton Hotels, integrating with Hilton Honors and leveraging its global distribution system to bring luxury glamping to the mainstream). Starwood Capital led Getaway’s Series B before the brand—re-christened Postcard Cabins—was acquired by Marriott International in December 2024, signaling that the world’s largest hotel company now views outdoor lodging as an extension of its core portfolio rather than a quirky side bet.

While those deals crystalized that branded outdoor stays can deliver hotel-like RevPAR and loyalty when the guest experience is consistent, “Version 1.0” also revealed structural difficulties that—to date—has held back the scale of many smaller operators, specifically:

Today, the 1.0 leaders and new emerging outdoor hospitality models are iterating on previous versions both strategically and structurally, planting flags at opposite ends of a clear barbell.

By the time Instagram tent photos started feeling stale, operators and investors alike had a clear checklist of what the next chapter had to fix. Permanent bathhouses and buried utilities were too expensive. Permitting dragged on for years. And once guests had posted their sunset shot, many never came back.

But the new generation of outdoor hospitality operators aims to address those challenges with a combination of technological and operating innovations:

Those three shifts set the stage for a clear barbell strategy. At one extreme sit luxury eco-resorts that charge hotel-suite money for tented lodges and private plunge pools. At the other are authentic, design-forward campgrounds that promise a friction-free, repeatable stay for under $200 a night.

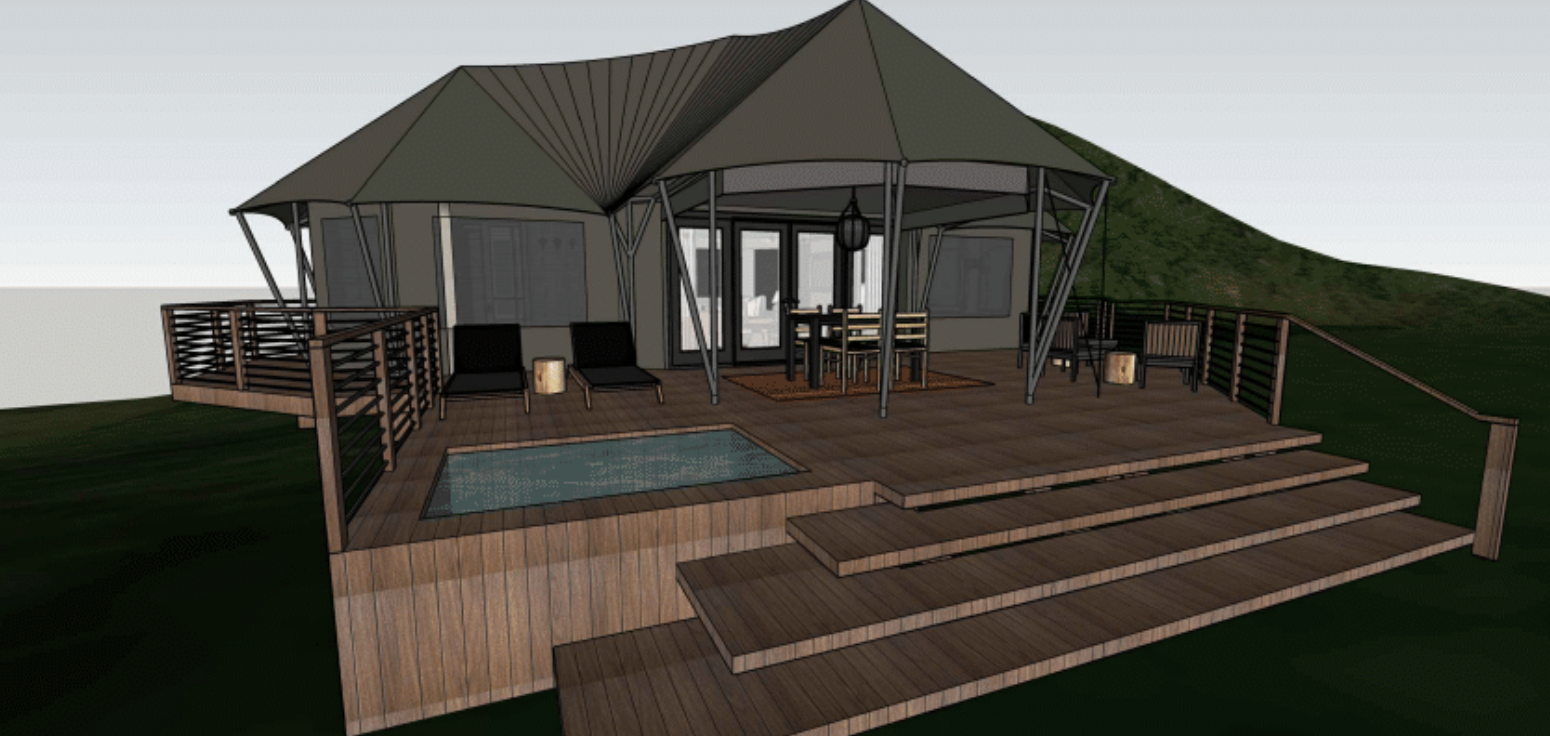

If the original glamping wave felt like a glamorous sleep-over, Sojourner feels more like checking into a four star resort that happens to have canvas walls.

Founders Andy Murphy and Dionis Rodriguez met at Harvard Business School but arrived from different corners of hospitality: Murphy built Zaina Lodge, West Africa’s first safari lodge and learned modular construction the hard way, while Rodriguez spent twenty-five years structuring hotel investments on three continents. Together they’ve set out to prove that genuine luxury and deep immersion in nature are not mutually exclusive.

Their flagship project rises on 200 wooded acres with unobstructed views of Shenandoah National Park, an hour-and-a-half from Washington, D.C. Each of the 144 suites is craned in fully finished—spa bath, plunge pool, wood-burning stove, even a small kitchen—and opens onto elevated decks that keep wildlife wild and guests dry.

A full-service restaurant, meeting pavilions, pools, kids’ club, and 15,000 square feet of spa and wellness round out the offering. Early surveys support peak-season rates of $900 to $1,200 a night; and underwriting suggests mid-teens cash yields once stabilized. Because so few U.S. parcels combine iconic views, affluent drive-time demand, and permissive zoning, Sojourner’s land pipeline is itself a moat—and a bargaining chip for future acquisition by an experiential REIT or major hotel brand.

On the other end of the barbell, Colorado-based Ramble aims to scale authentic nature experiences. Founder Matt Oesterle’s “aha moment” came on a pandemic road trip when every campground his family tried felt more like parking lots than nature escapes.

Inspired, Matt set out to reimagine the camping experience for modern travelers. Backed by experience scaling a tech company to $85M in ARR, he built a team of specialists in design, land use, and data. Ramble’s brand draws on outdoor credibility, with ambassadors like Tommy Caldwell and Sasha DiGiulian.

Ramble campgrounds are intentionally small—typically 25 to 75 sites—to preserve a village feel. Each campsite is generous, bathrooms and group amenities cluster in the centre, and trailheads start at the property edge. Prefabrication of all structures (including custom bathrooms with hot outdoor showers and flush toilets) keeps all-in costs below $65,000 a key. Nightly rates hover between $59 and $249, with upsells that range from firewood to branded gear to a roving electric ice cream cart, and even at conservative occupancy rates the model throws off 12-plus-percent unlevered cash yields.

The first two parks went from raw dirt to opening day in under four months and already boast a 4.9-star average rating and a Net Promoter Score of 91—top one percent for consumer brands. Scale that across 50 parks and Ramble looks less like a boutique experiment and more like a roll-up target for Sun Outdoors or Equity Lifestyle.

Outdoor hospitality has moved beyond the novelty phase.

Rapid growth in camping demand—11 million new U.S. households since 2019—is being met by better-designed, modular products that deliver hotel-grade comfort in natural settings. Meanwhile, global brands are voting with their balance sheets: Marriott’s purchase of Postcard Cabins and Hilton’s booking-channel alliance with AutoCamp are unmistakable signals that big-box lodging wants a stake in the outdoors.

Key takeaways for the industry:

If you’d like a deeper dive and are an accredited or institutional investor, join us for “Beyond the Tent: Investing in Outdoor Hospitality” a live, 60-minute round-table with leaders from Sojourner, Ramble, and Whitman Peterson. We’ll unpack operating metrics, capital structures, and market timing—then open the floor for Q&A.

—Paul Stanton

How a new model for rural communities built on shared identity is driving both demand and backlash

Small, founder-led experiential resorts are achieving high occupancy and premium pricing, but they don’t fit traditional capital models.

A data-driven approach to unit mix, layouts, amenities, and marketing helped one Gowanus Wharf project lease faster and at higher rents in a crowded market

How CERES is bringing the European “gourmet cluster” model to U.S. residential development, with food and culinary culture at the center of daily life

Covering the future of real estate and the people creating it