AI for Real Estate Acquisitions

We've been building AI acquisitions agents with real estate GPs. On August 13, we're opening the hood in a live 2-hour workshop

We've been building AI acquisitions agents with real estate GPs. On August 13, we're opening the hood in a live 2-hour workshop

The carry trade is dead, and capital is moving to whoever can manufacture cash flow. Takeaways from a day with more than 250 investors and operators in emerging real estate.

Private wealth has passed the institutional market, and most sponsors have no idea how to reach it. A workshop on raising from family offices and RIAs.

Why the small multifamily residential class is positioned to pick up where single-family rentals left off

Over the past decade, single-family rentals (SFR) emerged as a significant institutional real estate asset. But the combination of rate hikes and heightened competition has led to a sharp decline in institutional activity in the SFR sector. As a result, investors are increasingly looking to slightly larger properties—small multifamily—for the next big investment opportunity. Today, we’ll explore how and why the small multifamily sector is gaining interest among institutional owners and where it might go from here.

Multifamily real estate has had a complex few years. The disruption caused by the pandemic drove millions of people out of cities, forcing residential landlords, used to consistently climbing rents over the past few decades, to deeply discount their units in order to maintain occupancy. Then renters flooded back, but so did regulatory overhead, mortgage rates, and costs of doing business, from insurance to maintenance and repairs.

Although demand for urban living began picking up again in 2022, driving rents to new heights in nominal terms, the Federal Reserve’s decision to raise interest rates in response to inflation has made financing/refinancing real estate purchases, whether for owner-occupiers or for investment, significantly more expensive, putting downward pressure on residential real estate values even as rents continue to climb.

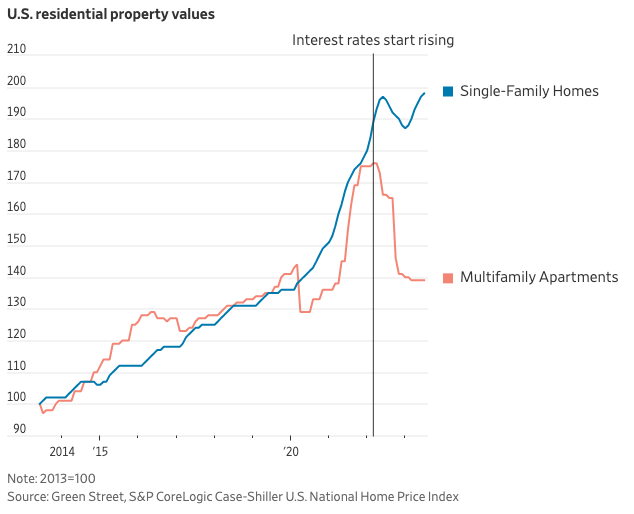

As shown in the graph above, trade prices for multifamily real estate have dropped precipitously following rate hikes, while those of single-family homes have continued to climb, albeit more slowly than before the hikes. In large part, this is due to a different buyer pool. Millions of individuals are vying for single-family homes alongside institutional purchasers, whereas primarily institutions, operating under stricter financial return parameters, are active in the multifamily space.

The continued rise of single-family home prices is driving down yields and making scattered-site SFR less attractive to returns-conscious institutional buyers. Cap rates in the space have dropped considerably, and many of the largest players have shifted from being net buyers to net sellers. At the same time, the combination of climbing multifamily rents and stagnant sticker prices suggests a latent opportunity within a broadly undervalued class, but which subset presents the best opportunity along other dimensions?

We've been building AI acquisitions agents with real estate GPs. On August 13, we're opening the hood in a live 2-hour workshop

EG is applying the American real estate private equity playbook to Australia, starting with medical office

Our annual list of firms actively investing in real estate technology companies

Predicting six new real estate marketplaces to rise over the next decade

Covering the future of real estate and the people creating it