The Thesis Driven Innovation 100, 2026 | #51-100

Meet the 100 people shaping the future of the built world

Meet the 100 people shaping the future of the built world

A 90-minute tactical workshop for real estate professionals and vendors who want to get the most out of conferences

After years of false starts and regulatory confusion, a few serious projects are pointing toward what this technology can actually deliver for real estate

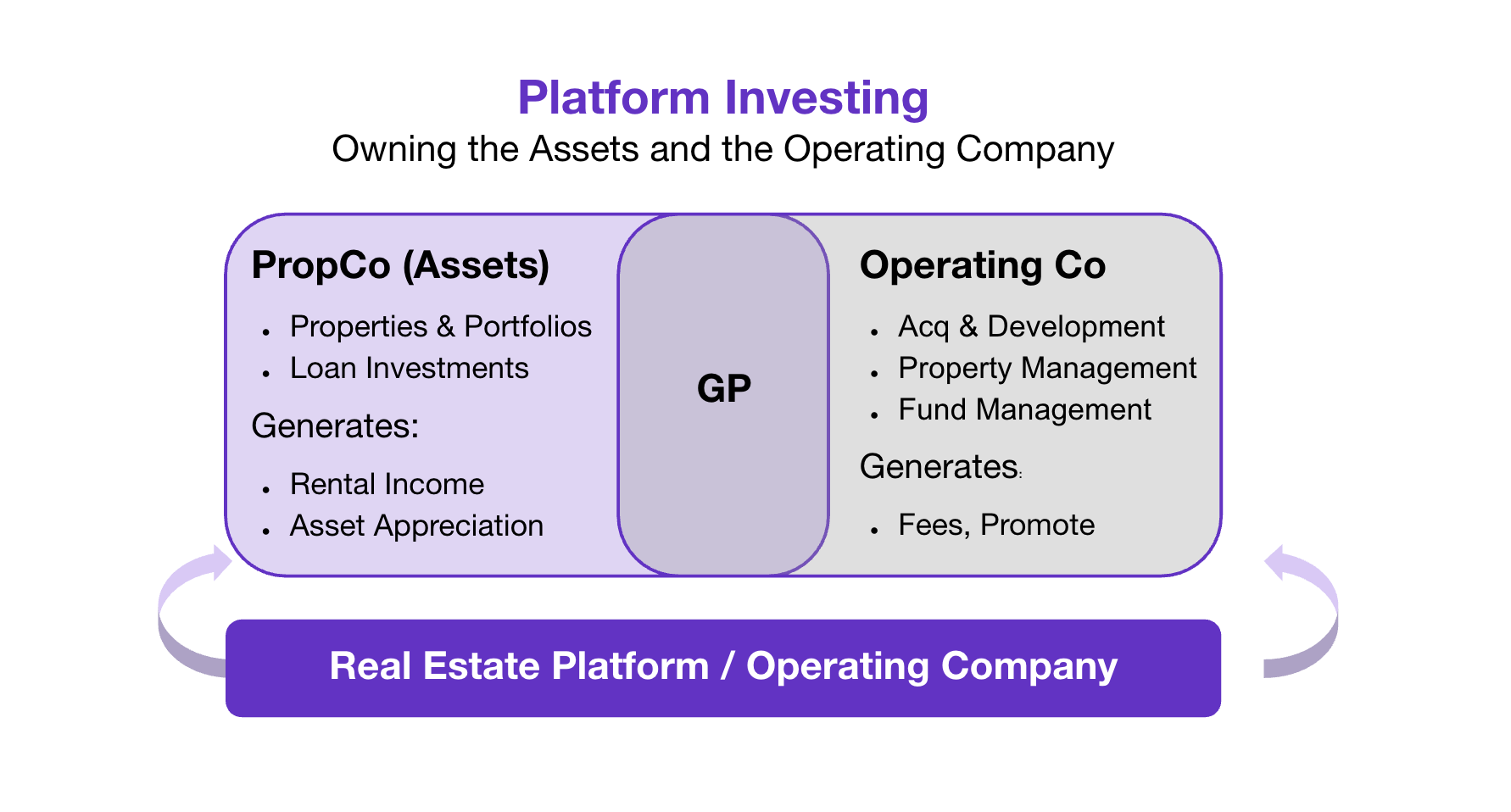

Backing both the real estate and the operating businesses of middle-market real estate companies

Don’t miss Thesis Driven’s Buy Box deep dive on Capitalizing Real Estate Platforms with Madison International next Wednesday, February 25th. Register here (for accredited & institutional investors only).

Real estate is having an identity crisis.

For the better part of the past decade and a half, the industry treated buildings like financial instruments: buy at a cap rate, finance cheaply, mark up on cap rate compression, and repeat. Underwriting was an exercise in toggling discount rates, exit caps, and rent growth—not about whether the real estate company operating the asset had the right operating system to outperform.

Now, that playbook is breaking.

Tenants and users are asking more from the “real estate product,” forcing commercial real estate to move from a financial asset toward an operating asset, where value is increasingly created not just in the physical building, but in the platform that sources, operates, and scales it.

So if value is migrating into the operating layer (i.e., a real estate company’s systems, data, sourcing, property ops, capital markets capability, etc.), then the best companies should trade at higher enterprise values than the underlying bricks-and-mortar would suggest.

And if that’s true, then capital providers who can invest in both the assets and the operating company can manufacture a return profile that looks meaningfully different from traditional PERE.

That’s the opportunity Madison International Realty is leaning into with its Platform Program (MIRPP), a strategy designed to provide flexible capital to middle-market, vertically integrated real estate platforms, combining (i) real estate investing with (ii) participation in operating-company economics, including EBITDA growth and potential multiple expansion.

In this letter, we’ll examine:

Platform investing can mean different things depending on who you’re talking to. In its simplest form, it’s capital stepping above the asset level and into the operating business—funding not just properties, but the operating team and systems that produce them.

A more useful way to frame it is by looking at what problems the capital is solving.

In today’s market, there is a spectrum of liquidity needs at the platform level: recapitalizing legacy partners, providing LP liquidity, solving redemption queues, restructuring balance sheets, forming OpCo/PropCo structures, seeding new funds, or supplying co-GP capital for larger mandates. The common thread is that the constraint isn’t always asset quality—it’s platform capacity. Growth, succession, and institutionalization all require capital that traditional deal-by-deal structures struggle to provide.

So why is this opportunity emerging now?

Several forces are converging at once. LP consolidation has thinned the capital landscape for mid-sized managers, as institutions double down on fewer relationships. Vertical integration has become more valuable as execution risk has risen—operators who control sourcing, development, operations, and capital markets internally are structurally advantaged. And importantly, platform capital needs are “all-weather”: partner liquidity, GP balance sheet recapitalization, and growth funding don’t pause just because transaction volumes do.

Where this gets most interesting is in the middle market—the stage Madison believes is both undercapitalized and misunderstood.

As firms scale, their capital needs evolve alongside them:

The underwriting lens shifts accordingly. Early-stage platform bets often hinge on the real estate thesis and the operator’s potential. Late-stage GP stakes are largely corporate finance exercises—underwriting fee durability and enterprise value.

The middle market sits in between. It’s the accelerator phase: an existing portfolio, a proven track record, and an operating company still being built in real time. So investors aren’t just evaluating property performance but also assess hiring plans, governance frameworks, capital formation strategy, margin scalability, and incentive design.

That dual underwriting burden is what makes the space challenging—and why, for the right capital partner, it remains one of the most mispriced opportunities in real estate today.

In Madison’s hybrid investment strategy, capital is deployed first and foremost into real estate, but paired with a meaningful stake in the operating company. That translates to an allocation framework where roughly 60–80% of capital sits at the asset level, complemented by 20–40% invested into the OpCo.

That blend is the connective tissue between two underwriting disciplines that historically lived in separate silos: real estate private equity and growth equity.

One anchors returns in tangible assets and downside protection; the other creates upside through enterprise value creation. Madison’s investment thesis is that the most optimal risk-adjusted outcomes come from pulling both levers together.

The distinction becomes clearer when compared with traditional middle-market PERE. The conventional playbook is asset-centric: source properties at attractive basis, execute a value-add business plan, apply leverage and structuring at the deal level, and exit into a deeper capital market once stabilization is achieved. Returns are generated almost entirely through asset appreciation and cash flow growth.

Platform investing layers another dimension onto that model. The capital isn’t just solving for a capitalization event—it’s solving for scale & compounding. The investor’s return profile reflects that broader mandate:

Madison often frames this as “combining property and platform economics,” with an explicit eye toward EBITDA expansion and multiple re-rating as the operating company institutionalizes.

The strategy sits between two more established forms of platform capital:

The middle market sits squarely between those poles. It’s growth equity applied to real estate platforms that already work but haven’t fully scaled, where the machine exists, but it’s still being built while running.

Madison’s argument for why it belongs in that lane draws on its institutional DNA. The firm has spent more than two decades structuring liquidity solutions across the GP-LP ecosystem through its secondary investment business. That vantage point, built at the intersection of capital needs, ownership transitions, and complex structuring, is now being applied upstream in growth-capital partnerships with operating platforms.

Madison is designing capital solutions that help companies become institutional platforms while seeking to participate in the value created along the way.

Puma is a UK-based real estate credit platform focused on originating first-lien senior secured development loans, typically in the £20-100 million range.

It’s a segment of the market that sits in a financing gap: traditional banks have limited development lending capacity due to regulatory capital requirements, while it remains too small—and too operationally intensive—for large global credit funds to prioritize. As UK banks have pulled back from development lending under regulatory pressure, that gap has widened, creating space for specialist non-bank platforms to scale.

Rather than structuring a simple capital allocation into Puma’s loan book, Madison made a dual-layer platform investment—capitalizing both the assets being originated and the operating business that originates them as a strategic partner to Puma.

The firm made a significant growth capital investment split across two linked investments:

The fund commitment established institutional infrastructure around Puma’s lending strategy and helped create a seed portfolio. That capital helped Puma launch and institutionalize a discretionary fund product that could grow AUM beyond its legacy lending business.

Meanwhile, the OpCo investment created a business partnership to drive enterprise value in an aligned way. Madison acquired a 24.5% ownership stake, secured a board seat, and created an aligned governance & exit framework to further the goals of Puma long-term. In other words, they weren’t just funding loans—they were underwriting the platform’s ability to source, diligence, and scale those loans over time.

This two-pronged structure is the essence of middle-market platform investing. The asset investment builds the fee engine and track record, while the OpCo stake seeks to capture the value that engine creates.

Explained simply, the financial engineering works in three layers:

It’s real estate investing and growth equity investing fused into a single capital solution.

Madison’s Platform Program is focused on the U.S. and Europe, with the program initially constructed around a targeted portfolio of 8–10 platform investments and an overall capital base in the range of $1 billion.

Madison brings institutional scale that’s atypical for middle-market platform investors, with roughly $5.8 billion of AUM. It has also spent more than two decades executing its core strategy in the real estate secondary market, a business that sits at the crossroads of GP liquidity, LP restructuring, and ownership transitions—the same pressure points that often trigger platform recapitalizations

The Platform Program itself is led by Managing Director Mo Saraiya and Directors Vince Clark (US) & Akaash Shah (Europe). As Saraiya has framed it in conversations around the strategy, “the goal is to provide liquidity and growth solutions to strong management teams through a bespoke combination of asset-level and entity-level investment.”

In practice, that mandate means underwriting two businesses at once: the real estate portfolio that exists today, and the operating company that must scale to create the next generation of investments and operational execution.

Geographically, Madison operates across a global footprint spanning New York, Los Angeles, London, Frankfurt, Luxembourg, Amsterdam, Singapore, and South Korea. For operating partners, that reach translates into more than branding—it opens relationship channels to global LP capital, cross-border capital markets insight, and institutional connectivity that can accelerate platform growth.

Alongside balance sheet size, Madison tends to position itself as a strategic capital partner, bringing infrastructure that middle-market platforms often haven’t fully built yet. That includes expertise around:

That support often sits behind the scenes—helping institutionalize reporting, refine governance, or structure future fund vehicles in ways that resonate with global capital allocators.

This toolkit becomes particularly valuable when paired with the types of platforms Madison gravitates toward. While the firm looks across sectors, its “ideal partner” profile tends to share several characteristics:

And critically, Madison places a premium on vertical integration. Platforms that control sourcing, execution, and operations internally make it easier to identify where enterprise value is being created—and where scaling capital can have the most impact.

Platform investing is part of a broader capital markets recalibration in which investors are increasingly prioritizing durable economics over cyclical beta. In an environment where cap rate compression is no longer doing the heavy lifting, capital is migrating toward strategies that can manufacture return through structure, scale, and operating leverage.

Madison’s view is that this shift is still early.

Over time, they expect liquidity for entity-level positions to deepen—driven in part by LP appetite to move successful platforms into open-ended vehicles, and by the gradual maturation of a secondary market for platform equity stakes. As that liquidity develops, platform ownership becomes less of a long-duration hold and more of a capital markets tool that can be actively managed, recapitalized, or monetized.

If that trajectory holds, several structural changes begin to take shape across the industry.

1. More operators will build with platform optionality in mind. Historically, many real estate firms were built simply to own and operate assets. Institutionalization, product expansion, and capital markets sophistication often came later—if at all. Going forward, that sequencing flips. Platforms are increasingly being designed from inception to do more than hold properties. They’re built to launch investment vehicles, raise third-party capital, institutionalize reporting and governance, and ultimately be valued as operating companies in their own right. That shift has downstream implications: finance infrastructure, leadership depth, technology systems, and incentive structures all move from back-office considerations to enterprise value-drivers.

2. More LP return enhancement will come from structure—not just asset selection. Madison often illustrates this through scenarios where fee participation, promote sharing, and platform scale layer incremental return streams on top of project-level IRRs. The underlying insight is intuitive: if you can earn returns from the real estate and own a share of the platform producing that real estate, you’ve effectively created a second engine of compounding.

3. Underwriting and structuring of platform investments is becoming its own specialization. Middle-market deals in particular require fluency across disciplines—asset underwriting, corporate financial analysis, incentive design, governance structuring, and exit engineering. It’s a hybrid skill set that blends real estate private-equity with growth equity investing.

That complexity is precisely why the opportunity persists. In seed-stage platform investing, investors can grow into the discipline alongside the operator. In late-stage GP stakes, the infrastructure is already built. But in the middle market—the lane Madison is targeting—the platform is scaling in real time. Scaling friction is real, structuring precision matters more, and capital partners need to arrive with a fully formed playbook on day one.

As platform investing matures, that playbook may become more standardized. For now, it remains one of the clearest frontiers where real estate and corporate investing continue to converge—and where differentiated capital can still shape outcomes, not just participate in them.

We’re excited to dig deeper with Mo & Vince on Wednesday, February 25th at 3pm EST to discuss Madison's platform investing strategy, how they partner with operators, and where they see opportunities today.

Register here (for accredited & institutional investors only).

How Angeleno is structuring deals and executing projects in a market where affordable housing is notoriously difficult to build

What marketing and leasing audits reveal about multifamily's hidden performance problem

From all-electric skyscrapers to floating offices and carbon-neutral urban development, these firms are redefining the future of the built world

Covering the future of real estate and the people creating it