Tokenized Real Estate: Separating Opportunity from the Hype

After years of false starts and regulatory confusion, a few serious projects are pointing toward what this technology can actually deliver for real estate

After years of false starts and regulatory confusion, a few serious projects are pointing toward what this technology can actually deliver for real estate

A new session on how AI is transforming the mechanics — and economics — of raising real estate capital

After years of false starts and regulatory confusion, a few serious projects are pointing toward what this technology can actually deliver for real estate

As the blockchain industry evolves, it’s coming into contact with more parts of the real world economy. This often involves some combination of concern regarding the reputation of that industry and uncertainty around how exactly it will add value for a given use case. Especially in sectors with lots of capital at stake and significant reliance on trust, the addition of a new element that is not well understood can seem like a distraction at best or an unacceptable risk at worst.

Tokenized real estate can be a tough sell from the perspective of both investors and operators. At Groma, in addition to the work we’ve put into developing our core real estate strategy, we’ve spent a lot of time thinking about where tokenization adds the most value. Ultimately, while there are many small wins to be found in terms of accessibility, efficiency, and transparency, our view is that improving real estate’s utility as collateral is likely to be the most significant improvement tokenization can offer.

This letter will explore the broad and divisive topic of real estate tokenization. We’ll cover:

Tokenization is the process of turning some element of an existing asset into a digital token recorded on a distributed digital ledger called a blockchain.1 The technique can be applied to physical objects like gold or collectibles, or to financial assets like dollars or securities. It can also be used to represent full ownership of an asset, or to split an asset's economic features apart, separating income from appreciation, for instance.

Worth noting: the earliest crypto tokens, and the ones that still make up a sizable majority of value held on chain, are not actually examples of tokenization. Bitcoin, Ether, Solana, and various smaller tokens (including memecoins) are purely digital assets; their value is derived from the utility of the blockchain networks they run on, not from any underlying assets backing them.

Of asset-backed tokens, the largest category by far is stablecoins like USDT (issued by Tether) and USDC (issued by Circle), most of which are pegged to the dollar and backed by dollar-denominated assets like short-term Treasuries and cash equivalents. These function essentially as dollar proxies on the blockchain, and they represent the clearest example of tokenization that has achieved genuine scale—USDT alone carries a market cap north of $140 billion. Other tokenized real-world assets (RWA) are a fast-growing but still relatively small part of the broader digital asset space.

Advocates of tokenization point to a variety of benefits:

Accessibility: Some assets, especially in real estate, are simply too costly for the average investor to own outright. Advocates sometimes claim that tokenization reduces this barrier to entry by enabling fractionalization of large assets—while ignoring the reality that fractionalization has long been available via traditional financial structures like funds and REITs.

Some of these vehicles are only available to institutional or accredited investors, but tokenization doesn't solve that problem. As the SEC has stated repeatedly, an investment made in a common enterprise with profits expected from the managerial efforts of others doesn't cease to be a security merely because it is made via blockchain and recorded in tokenized form. Issuers and brokers who transact in tokenized securities have to comply with the same laws and regulations as those who transact in traditional securities.

Efficiency: By default, blockchain transactions execute automatically and near-instantly through "smart contract" logic, meaning self-executing digital agreements. Many traditional financial systems are moving toward faster settlement—the US securities industry switched from T+2 to T+1 settlement in 2024—but closing that gap entirely would require changing the intermediated structure of these legacy systems, which involves real tradeoffs. And while tokenized transactions aren't costless, they can be much cheaper than traditional payment processing, especially on blockchain protocols that prioritize efficiency over decentralization.

Transparency: The vast majority of crypto assets are held on public blockchains, meaning that the wallets holding these assets and transactions between them are publicly visible and inspectable. It’s still possible to obfuscate ultimate beneficial ownership via proxies, but the overall picture is still far more transparent than the walled gardens that predominate in the traditional financial industry.

Composability: Blockchain's flexibility and relatively permissive access structure make it easier to "compose" underlying assets into more complex structures. Splitting yield and appreciation is one such application, as are various lending and borrowing use cases. These functions exist in the traditional financial system, but they are often unavailable or prohibitively expensive for retail investors. Someone with $100M in their brokerage account can borrow against those holdings at a competitive rate; someone with $50k likely can't. Many on-chain systems enable this kind of structure for much smaller balances.

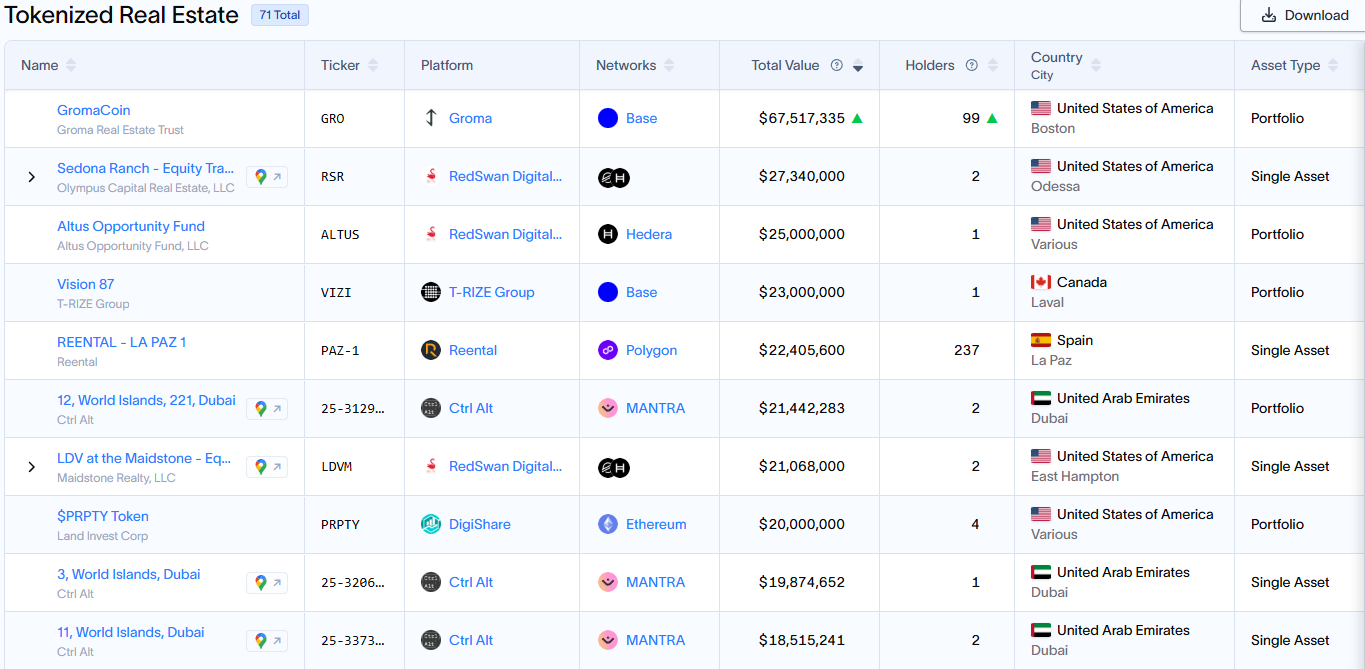

Real estate is the world's largest asset class, with roughly $400T in global value. It's also one of the most illiquid, with $10-15T held in private markets and only $2-3T in publicly traded forms. That gap presents an obvious opportunity for tokenization. Yet a comparatively small percentage of real estate assets have been tokenized—just less than $500M worth, as of this writing.

It's not surprising that real estate sponsors and asset managers have been hesitant to incorporate blockchain functionality into their businesses. Many still view the blockchain industry with skepticism born of its well-publicized frauds, scams, and crashes. If you have billions in investor capital under management, the path of least resistance is to simply stick to your existing strategy and not risk adding new features that could spook investors.

And many of the advantages of tokenization are less applicable for the large investors who drive decision-making in real estate. If a pension fund with $500B to deploy wants to borrow $5B against $10B of its real estate holdings, it can call up a banker and make that happen (the banker will probably be grateful and offer a competitive rate to boot).

As in other parts of the blockchain industry, some early real estate tokenization projects have been sloppily run, or worse. RealT, for instance, raised nearly $100M via real estate token sales, but failed to adequately maintain the properties in question or even to secure the relevant deeds in some cases.

Some of this is downstream of regulatory uncertainty. As Congress, the SEC, and the CFTC have sought to create more precise definitions for different types of digital assets, many risk-tolerant blockchain projects have decided that it's better to seek forgiveness than permission and plowed ahead with deployment and fundraising in the hope that a) they will evade regulators' notice; b) regulators will end up agreeing with them; or c) they will be able to abscond with their bags before enforcement catches up with them. These projects are more likely to seek to operate outside of US jurisdiction or to raise capital from less sophisticated investors who won't demand the level of diligence and disclosure expected by institutions.

The picture is not entirely bleak, and the policy environment in particular has shifted considerably over the past year.

Under the 2021-25 tenure of Gary Gensler, the SEC was notoriously hostile to the blockchain industry, refusing to articulate clear boundaries between securities, commodities, and other categories within the digital asset space. Congress entertained market structure reform during this period, but the only crypto-specific legislation that made it out of the legislature, one overturning a piece of Gensler-issued guidance, was vetoed by President Biden2.

This state of affairs changed dramatically after President Trump took office. Trump immediately issued a raft of pro-crypto executive actions and then appointed the crypto-friendly Paul Atkins as SEC chair. Congress has been friendly to the industry as well, passing the stablecoin-enabling GENIUS Act in July 2025 with bipartisan support and working toward long-awaited market structure reform.

With regulators and elected officials well-disposed to the blockchain industry and regulatory clarity coming into view, traditional financial institutions have been leaning into partnerships with crypto-native projects and building out their own in-house blockchain assets and services as emphasis shifts toward tokens with durable real-world value. Stablecoins are still the largest RWA category by far, but debt products, corporate equities, and real estate are all gaining ground.

Figure is a fintech platform that originates and aggregates consumer loans (primarily HELOCs) and connects those loans to investors using its capital markets infrastructure. The full lifecycle of each loan is automated via smart contracts, making these loans easier to package and trade while reducing friction and delays for borrowers. At the same time, it is providing real-estate-linked yield in the 8-9% range to on-chain lenders, beating the mid-3s returns that currently predominate in standard stablecoin lending.

The platform has leaned heavily into compliance. It operates a FINRA-registered broker-dealer and alternative trading system (ATS) and has issued multiple SEC-registered tokenized securities. Sitting between hundreds of thousands of borrowers and a diverse array of lenders and loan securitizers, it has established a robust bridge between the mortgage industry and on-chain finance. Figure's own revenue comes from fees and spread earned on the tokens it issues and from the other financial services it provides as part of the loan lifecycle.

Parcl is, in effect, an on-chain derivatives market that enables users to speculate on real estate prices at the city or neighborhood level. Like Figure, it doesn't strictly tokenize real estate ownership, but it provides a way for users to gain economic exposure to underlying real estate fundamentals. Users can take long or short positions in a given market, meaning that it may become a useful tool for hedging once it reaches sufficient scale. A notable downside of this model is that, since gains made by longs must be matched by losses made by shorts, it is at best zero-sum (and negative-sum after fees).

Parcl runs on decentralized finance (DeFi) rails, which can make it difficult to slot into traditional market structure roles like exchange, ATS, or broker-dealer for which centralized control is necessary. That hasn't prevented a partnership with Polymarket to support real estate prediction markets, however.

Groma (of which I am a co-founder) starts with a concept that is relatively simple from a legal/regulatory perspective: REIT shares, but tokenized. We seek to add value by leveraging3 blockchain's composability. GromaCoin is a tokenized share in the Groma Real Estate Trust (GromaREIT), a US-registered REIT. It aims to provide competitive income and appreciation via a novel investment thesis and AI-enabled operations, and we've raised roughly $200M of equity into it and our closed-end funds on the strength of these elements prior to any value-add from blockchain. GromaCoin is currently the largest tokenized real estate asset.

In our view, the area where a buy-and-hold asset like GromaCoin stands to gain the most from tokenization is its utility as collateral, rather than improved transaction costs or settlement times. Real estate has been arguably the world's favorite collateral asset for centuries: it carries durable, near-universal value, and it is very hard to run away with. This is true even when it is non-diversified and costly and time-consuming to liquidate, as with individual properties.

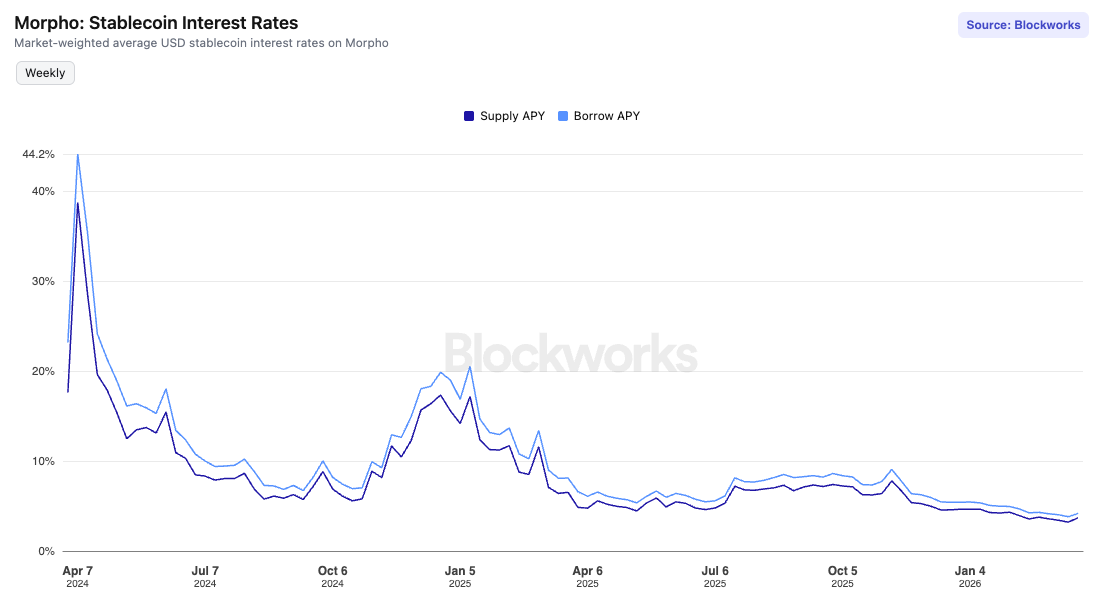

We expect that removing these limiting factors will enable even more efficient borrowing, unlocking novel use cases. For instance, Morpho, a decentralized lending protocol, currently enables collateralized borrowing at an average APY of 4.15%.

Cheap debt opens up a range of possibilities. Looping, in which stablecoins are borrowed against an asset to purchase more of that same asset, which is then used to back more borrowing, is a popular strategy. Given GromaCoin's total annual return of 7.85% for 2025, we expect some of our holders will take advantage of it.

We’re particularly excited about a tool that we call rentvesting. Rentvesting allows renters to turn their payments into leveraged exposure to GromaCoin. If GromaCoin’s value goes up, they keep the delta; if it goes down, it’s GromaCorp’s liability4. In the background, we’re borrowing stablecoins to fund the program and paying off interest with the revenue from the newly created shares. If that revenue5 exceeds the interest, GromaCorp keeps the spread. We see this as both a great way for renters to efficiently build wealth and significant untapped source of equity capital.

With only one millionth of global real estate value tokenized and lingering doubts about the seriousness of the crypto industry, real estate tokenization is still in its infancy. At the same time, an improving policy environment, greater institutional buy-in, and increasingly sophisticated on-chain infrastructure and expertise are opening up new opportunities for investors and asset managers.

A key part of this process will be identifying the blockchain applications that genuinely add value and those that don’t. We hope this letter has helped address some of those questions and provided a foundation for thinking through the rest.

Notes:

1A thorough explanation of what blockchain is, how it works, and how it has evolved since the invention of Bitcoin in 2008 is beyond the scope of this essay. For an accessible technical overview, I’d recommend 3Blue1Brown’s writeup; for coverage of current events, I’d recommend our friends at Castle Island Ventures.

2Reportedly at the behest of Warren-aligned staffers in the administration.

3Pun intended.

4Importantly, GromaCorp is the operating company, not the REIT itself.

5Which includes both GromaCoin dividends and our asset and property management fees.

6US renters spend roughly $650B on rent annually; capturing a small portion of this would be transformative for our AUM growth, to put it mildly.

For an industry built on spreadsheets and market analysis, asset management may be the next AI target.

AI comes for property diligence – with major implications for real estate acquisitions

A tiff between two proptech darlings is a proxy battle for AI’s growing role, with multifamily operators stuck in the middle

For multifamily operators, the AI gap is shifting from technology to execution

Covering the future of real estate and the people creating it