Who is Investing in Real Estate Tech? 2026 Edition

Our annual list of firms actively investing in real estate technology companies

Our annual list of firms actively investing in real estate technology companies

One week out, the people building the next generation of real estate assets are gathering in one room. Thesis Driven&

A study of the importance - and feasibility - of family-friendly units

Editor’s note: As regular Thesis Driven readers know, I believe we must design cities that work for families. And a big part of making cities great for families is building apartments that meet their needs. No one has pushed harder for this than multifamily developer and my friend Bobby Fijan, who recently released an excellent report with the Institute for Family Studies based on a survey of over 6,000 Americans. I asked Bobby to explore the report and what it means for cities and developers in today’s Thesis Driven. -BH

There’s a sad vicious cycle in American cities: Young people drawn by the culture and opportunity of city life move-in in droves, and developers build lots of apartments for these people. This population influx leads to thriving, revitalized cities. But instead of getting married, starting families, and building roots to continue growing in the very cities they moved into, many young adults delayed family formation, and when they do have children, they move out.

It’s a tragedy: cities attract a generation in their 20s, only to watch their children disappear from the census rolls.

Are these things connected? Is there a way urban apartments can be built to be more family-friendly? Can this product be justified to real estate investors and lenders? And, most importantly, would it make a difference?

Our new report published at the Institute for Family Studies seeks to answer these questions. Our co-authored report is based on a nationally representative survey of over 6,000 Americans ages 18 to 54. We explored their apartment preferences by using randomized tests of real floorplans and rendered images. The study comes to a clear conclusion:

Bedrooms matter. Americans, and particularly Americans who want to have children, systematically prefer floorplans with more bedrooms over open floorplan layouts, even without any change in total square footage. It turns out that wanting “extra room” for a baby means a literal room with four walls, not a more spacious room with a larger square footage. And Americans are willing to pay more for them.

Today’s letter will cover:

The apartment mix we see today is the product of two forces: immediate market conditions and the structural conservatism of real estate investment.

After decades of suburban expansion, the urban core began to reassert itself in the early 2000’s as the place where opportunity clustered. The “creative class” of young, educated, and ambitious poured into downtowns, fueling both cultural vitality and economic growth. This effect accelerated in the ZIRP-era, resulting in the twenty largest metros capturing nearly half of all post-recession job growth in the US.

Developers responded with record apartment construction. As of today, apartments with >20 units make up more than one-third of all new housing units in the country. (Let it be known that while there IS a serious housing crisis in the country, apartment developers are playing their part in fixing it!)

But most of the product looked the same: “luxury” buildings dominated by small studios and 1BRs. In some submarkets, they accounted for 70 percent of new apartment supply. In Seattle, nearly two-thirds of apartments under construction are micro-units (<441 sf). Family-sized apartments, especially 3BRs, have remained in the low single digits of new apartment supply.

On its face, that choice was rational: smaller units do generate higher rent per square foot. And with rising construction costs and low interest rates, these projects penciled well.

Rising demand. Supply being built to meet that demand. All good? Sadly not.

Despite the influx of young single people with good high paying jobs, cities saw their fertility rates continue to decline, down 15% since 2010, and their child populations dwindle. This “urban family exodus” started before COVID and has only accelerated since. Since 2020, large urban counties have lost more than 8% of their under-5 population.

Until now, most apartment developers (but particularly their investors and lenders) have functionally assumed they can’t play in that family-sized apartment space. “Families don’t want to live in apartments,” they believe, and families moving out is viewed as confirmation of that assumption. But this idea actually isn’t what stops developers from building family-friendly units.

Large scale housing investments represent a uniquely cautious industry focused on delivering tax and risk-adjusted returns. As an industry, real estate is very efficient at deploying large sums of capital. Risk-averse investors want to be sure that units are leasable and can achieve their projected rent.

Thus, real estate investors have strong incentives to repeatedly build highly similar projects and structures that previously proved to satisfy common building code rules and deliver minimally satisfactory profits. That a different building design might increase profits 1% is less important than the risk that an untested building design could result in a massive, virtually unrecoverable loss.

Construction of speculative new configurations of units would, therefore, be confined to smaller “Missing Middle” type structures. But very few of these apartment structures are built. One estimate suggests that the average new apartment-building project has over 230 units. Of the 4.5 million occupied, rented apartment units built since 2010 in buildings with five or more units, the U.S. Census Bureau’s American Community Survey shows that 51% were in buildings with 50 or more units, and another 19% were in buildings with 20 to 49 units. Even when individual buildings have under 50 units, they are often part of a much larger development totally dozens or hundreds of units.

But market conditions have begun to shift. Unit turnover is costly, and it’s becoming harder to cover that up with rent growth. In the heady days of 2021 and 2022, with 20% year-over-year rent growth and 3% cap rates, apartment developers could afford to not care about the costs of turnover. “We’ll just stick to what’s working” was a disciplined choice. But now, as the pipeline of new projects delivers, rents are softening while turnover, vacancy and insurance continue to erode profits.

Buildings that have been (unintentionally or intentionally) designed for churn no longer look like safe bets … they look like liabilities.

This is the moment when real data on renter demand for a new housing type, one that supports longer tenancy and a new tenant demographic, matters.

For our survey, we wanted to ensure we assessed floorplans that could be applicable to as many apartment buildings as possible. In practice, this meant that the only floorplans that were selected for the survey were ones that already existed in many large, institutional size buildings. While there may be housing types with superior layouts (point access block, courtyard, rowhomes, triple deckers, etc), the double loaded corridor is the dominant building form of rental housing in the US, and so we assessed designs compatible with that type of building.

Prioritizing applicability also meant the sample needed to be designed to be maximally persuasive to the real gatekeepers of innovation in housing: investors and lenders. Therefore, we chose to use sizes of apartments that are already being commonly built, so that an investor and developer would not need to change unit count to implement the designs we test.

We gave respondents a choice between 2 floorplans that were identical in size and shape, differing only in the number of “rooms.” Respondents saw more colorful versions of these floorplans, as well as renders of their common spaces, because we weren’t confident that they would be able to visualize an apartment just from a floorplan. The six floorplans are shown below in their most intuitive, head-to-head comparisons (though we also tested floorplans of different sizes against each other as well: unsurprisingly, bigger apartments won out).

If you look at these layouts, the key point is how similar they are. In the 750 and 1100 size examples, both of the master bedroom suites are identical. And in both cases the living room is also the same size. The ONLY difference is whether or not there is a small extra room. This tradeoff comes at the expense of some closet space and direct bathroom access. Therefore, we know that the respondents are isolating the choice in these comparisons to a very narrow subset of design features.

For the 1200 square foot comparison, the difference is more substantial, but because there are windows on 2 sides, the extra room is a true additional bedroom. The primary cost is that the living room loses access to the corner windows. Which could be a meaningful sacrifice, if the building had a view in a scenic city.

With this basic setup, we tested willingness to have a(another) child, the relative importance of various amenities, willingness to pay for more bedrooms, and other elements of the design choice. (For the full analysis please read the entire 40-page paper.)

But for our purposes today, three figures from the paper show our findings clearly:

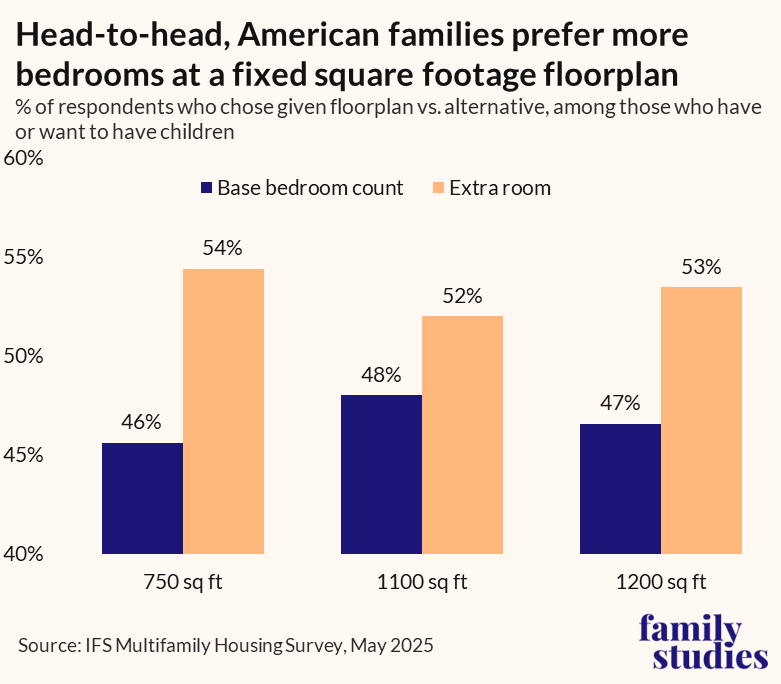

In the chart above, when people who have or are interested in having children are asked to choose between a 750 square foot unit with one bedroom vs. a bedroom and a separated den, 46% chose the one-bedroom, while 54% chose the room with the den. For the 1100 square foot unit, 52% chose the two bedroom with den, and for the 1200 square foot unit, 53% chose the three bedroom. That’s pretty intuitive—family-minded people would want an extra bedroom.

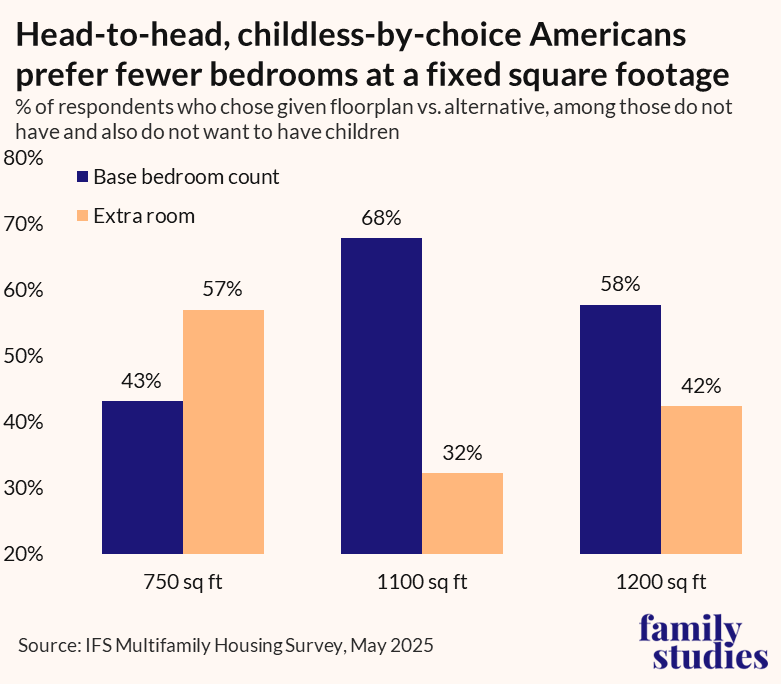

But the next chart shows the same floorplan preferences, now reporting results only for respondents who don’t have and don’t want to have children. In that circumstance, it is still the case that a majority of respondents prefer the layout with the extra room in the 750 square foot layout. But for the 1100 square foot unit, only 32% chose the two bedroom with the extra room, and for the 1200 square foot unit, 42% chose the three bedroom option. Even the childless-by-choice prefer to have at least two rooms in the apartment! They may not value a 3rd room as in the two larger floorplans, there really is broad demand for at least two separated rooms.

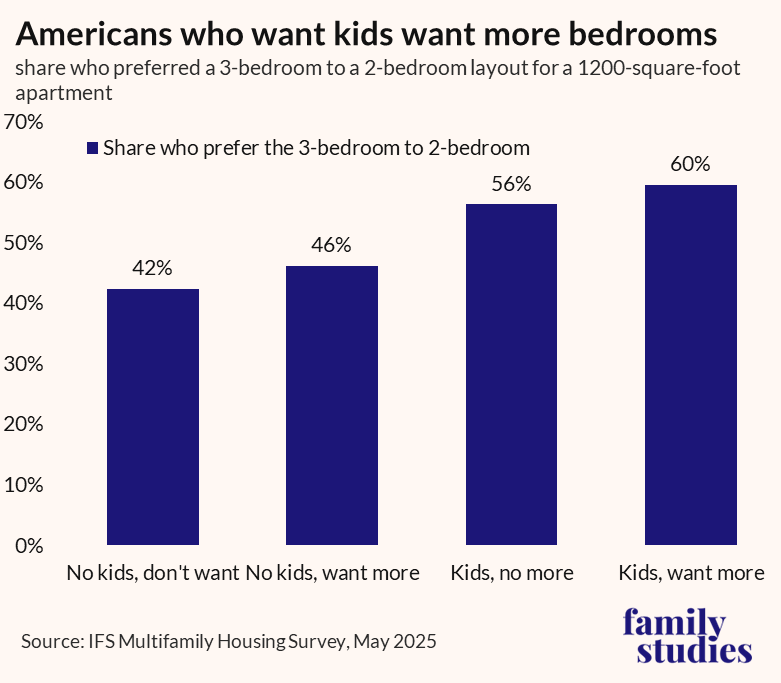

Finally, this chart focuses just on the 1,200-square-foot apartment comparison and how preferences shake out by detailed parenting status. Preferences for more bedrooms scale directly with actual or desired family size. Among the childless, there is a net preference for fewer bedrooms, but among those who have children, there is a net preference for more bedrooms. The childless who want kids slightly prefer the 2-bedroom over the 3-bedroom, but this simply reflects the fact that 2-bedrooms with all the extra space a 1,200-square-foot apartment entails is plenty for a first child.

There are two important things to take away from these three charts. The first is straightforward: People who are open to having a(nother) child prefer apartments with extra rooms. So, in order to build housing that is “family friendly,” developers should implement those changes by building more apartments with another four-walled room in the unit.

The second is less obvious but even more actionable because it doesn’t depend on goodwill or long-term intentions: At the 750 square foot unit size, building a “+Den” meets the preferences of both groups, making it a safe bet to build regardless. In the 750 square foot example, people who do not want children have a greater preference for a 1BR that has an extra room. Perhaps to use as an office, for guests, or a place to store their ski gear.

750 square feet is the average size of a new 1BR apartment. But the ratio of “standard” 1BR layouts to 1BR+Den is over 99:1. There is a massive undersupply in the market of “+Den” apartments. It’s an extremely uncommon layout. Even in Seattle, which currently has the most “microunits” of any market in the United States, 750 square feet is in the fifth percentile of size for all TWO-bedrooms. Clearly, a 750 square foot 1BR+Den can easily pencil within standardly accepted sized units.

Some of the 1BR+Den undersupply is due to dens that are termed as “Windowless Bedrooms,” which are not legal in certain markets, most notably New York City. But they are allowed in many markets, including San Francisco, Seattle, Austin, Dallas, Miami, Chicago, Philadelphia, and Boston (though always good to check with a local architect).

Even in the example of the 1100 square foot 2BR comparison, though the childfree respondents vastly prefer the traditional 2BR layout, the market is still significantly under supplied to fulfill a 30% preference of this group for the 1BR+Den.

Where there is unmet demand, product should be built to meet it.

So the demand exists, what could it “look” like? Here are 3 examples on how to implement it:

Unit Mix

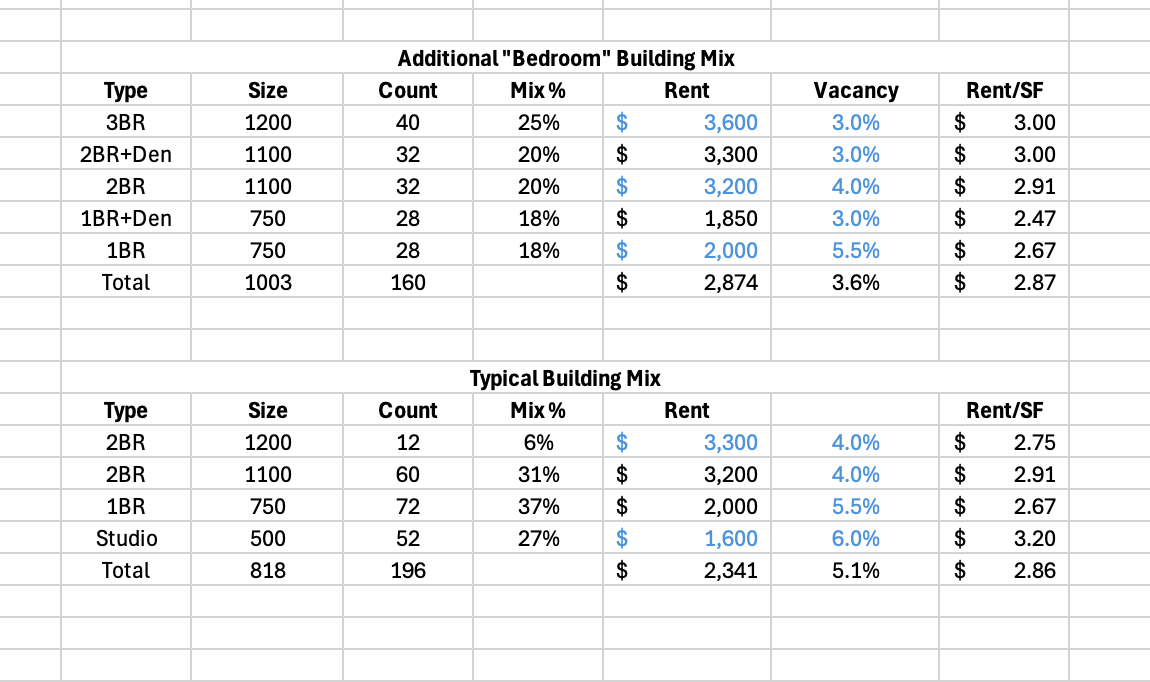

For a typical institutional size building, 5 stories ground floor amenities, 196 units it would be fairly common to see a mix like this. By simply shifting some of the unit mix towards “+Dens” and converting corner units to 3BR instead of split 2BR a build could achieve higher rent per square foot, and lower stabilized vacancy (due to lower turnover of larger bedroom count units). Unit count decreases to160, but NOI (and thus UYOC) would be higher … even before you account for the lower operating costs associated with lower turnover.

“Extra Bedrooms” in Office to Residential Conversions

As Brad has noted before, the extra bedroom, including the “windowless bedrooms,” is one of the most family friendly designs when it is permitted, especially since babies sleep so much anyway! One of the most inconvenient factors of conversions is the large office floorplates. Due to the larger elevator core and central bathrooms located on ever floor, the modern (condition) office buildings have floorplates that mean that units will be deeper than typical. One of the best way to make lemonade out of this situation is to design both the units and buildings in a more “family friendly” manner. With the additional upside, as Matt Yglesias has noted, that by saving industrial and office buildings for another use, we can “save” our downtowns.”

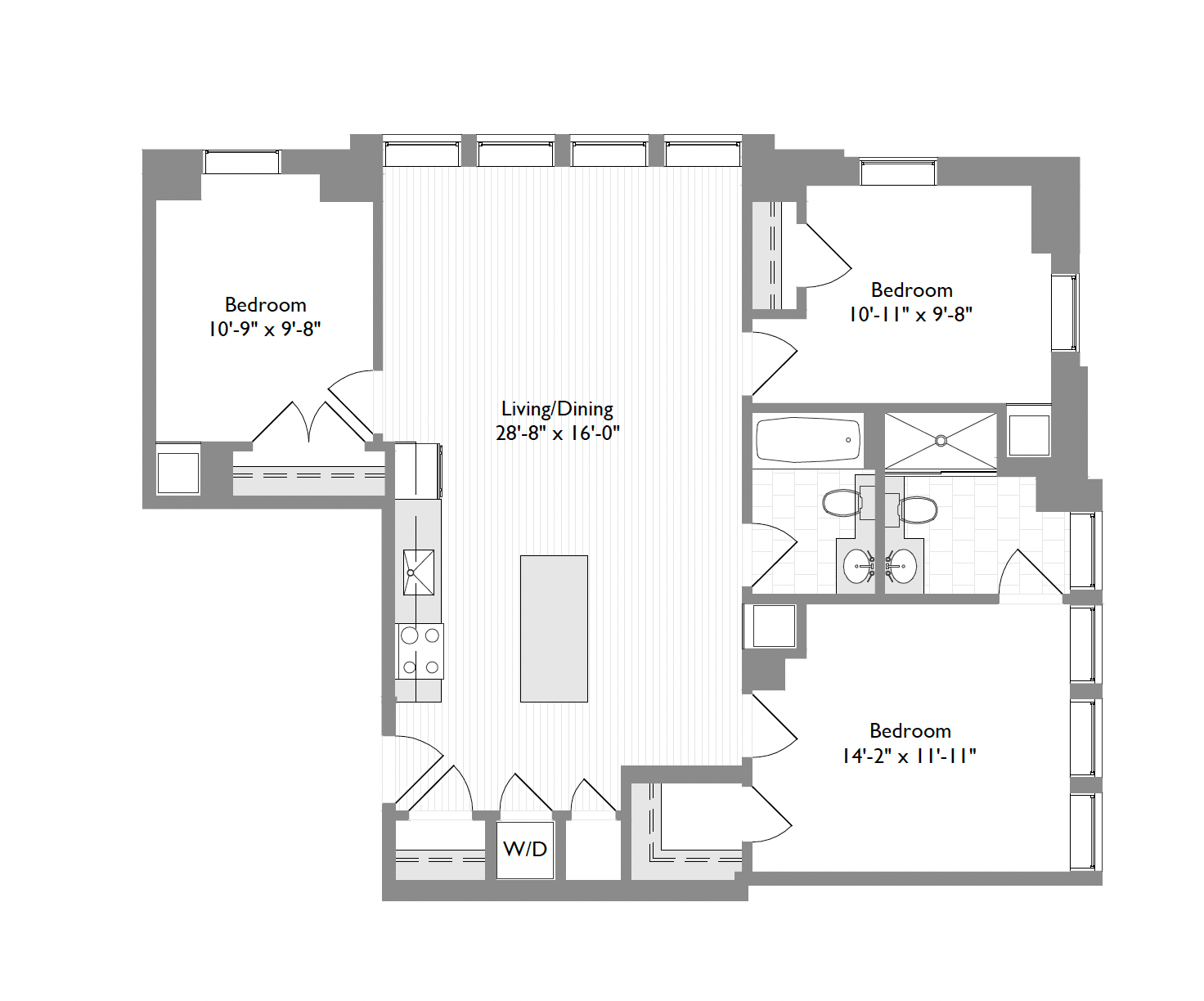

From a project that was featured in the New York Times, we have an 1140sf 3BR/2BA, which exemplifies adding the extra bedroom to the corner of the building.

And from an office to residential conversion in downtown Philadelphia on Broad Street (in a building that includes a kids playroom and art room) here’s an example of a 900sf 2BR/1BA, which demonstrates adding the “windowless bedrooms.”

A purpose built, institutional apartment building designed for families

Earlier this year, I had the privilege of visiting one of the most forward thinking and intentionally designed apartment buildings for families: AMLI Redmond Way, The East Building. Both the project and the strategy had been in development for several years. Even before Covid or before any hard data was available, the developer had a strategy on finding projects for larger units designed for families, and building them with Dens. A project finally presented where there were 2 buildings and it made sense to build one of them with larger units, and the other with a more traditional mix. So at the end of this year AMLI is a 126-unit building with an average size of over 1100 square feet.

Over 92% of the units are at least 1BR+Dens. And nearly 75% have 2 or 3 Bedrooms. The amenities are as robustly targeted at families as exists in an institutional building in the United States:

• Stroller parking in bike room and unit corridors

• Flip-down toilet seats designed for children.

• Climbing structure, sandbox, playhouse, trikes and riding loop.

• Large indoor playroom with activity areas and playhouse features.

• Parent seating areas to supervise children while working from home … and many more

While it is absolutely a challenge to make “family friendly” buildings as an investment case, what I hope has been demonstrated, both by the study and by examples is that it is possible. The future of our cities depends on investors and planners figuring out how to design and build product such that our young, ambitious, couples and have kids and stay in the City.

-Bobby Fijan

Covering the future of real estate and the people creating it