Who is Investing in Real Estate Tech? 2026 Edition

Our annual list of firms actively investing in real estate technology companies

Our annual list of firms actively investing in real estate technology companies

One week out, the people building the next generation of real estate assets are gathering in one room. Thesis Driven&

A new approach replaces manual real estate workflows with AI-driven systems built around the operator’s own data

Software stocks have taken a beating this year. Across the public SaaS universe, companies that were Wall Street favorites two years ago are down anywhere from 15 to 40 percent year-to-date, even as the broader market grinds higher. The selloff stems not from underperformance but rather a commonly shared fear: that AI is about to dismantle the traditional software model from within.

That fear has not yet reached real estate technology. PropTech multiples have held, point solutions keep raising fresh rounds at familiar valuations, Entrata just filed its S-1, and the prevailing view is that AI will be incorporated into existing software rather than upending it entirely.

Today's letter examines software's future through the lens of Outcome, a new company bringing an AI-first, "outcome-led" approach to the built world. On a practical level, Outcome is helping real estate companies go AI-native, and fast. On a conceptual level, it's a useful frame for thinking about where real estate software, including the core systems of record, may end up once AI does much of real estate’s behind-the-desk work.

Software was the place to be in 2023 and 2024. The sector rode the broader technology rally, and the per-seat SaaS model looked like one of the most reliable cash machines ever built: sell a license, renew it, expand the seat count, repeat.

But once the impact of AI became clear to investors, the mood soured quickly. Companies like HubSpot, Adobe, and ServiceNow each watched chunks of their market caps evaporate as analysts raised an uncomfortable question: if an AI agent can do the job a seat used to do, who needs the seat?

The surface-level threat is to pricing, since the per-seat licensing model rests on the assumption of a human sitting at a screen. That assumption is eroding across many sectors as AI agents take over the clicking.

But the deeper shift has less to do with how software is priced and more to do with what it fundamentally does.

Software used to mean a user interface piloted by a person. A human logged in, clicked through screens, and moved data from one box to another. The new generation is agentic and autonomous; it doesn't wait for clicks. Nor does it have to be one-size-fits-all. When the cost of building custom software shaped around a specific company's data falls, the entire logic of the packaged product inverts. There's diminishing reason to fit a team and its workflows into a vendor's existing box when the box can be built around the team instead.

A vendor can survive the per-seat model giving way to consumption-based or outcome-based pricing; plenty have made that transition before. Surviving the loss of the packaged product's reason to exist is harder. For three decades, software customers operated on the assumption that buying was cheaper than building. AI is reversing that assumption, and the stock market is paying attention.

We see this directly at Thesis Driven. Hundreds of real estate operators come through our AI workshops every month. But while a workshop is effective at communicating AI’s capabilities and laying out a plan, translating that understanding into something that works on Monday morning is much harder. That’s particularly true when processes are embedded in legacy stacks and data is scattered across silos with limited integration options.

But the transition away from traditional software is already happening beyond the real estate sector. Over the next month, for instance, we at Thesis Driven are migrating off every low-code and no-code tool we use, including Squarespace, Bubble, and Webflow. The value proposition that justified those subscriptions has evaporated for an organization that can now build the equivalent itself. That math works for a small, technical shop with a handful of tools and no thorny compliance issues. It does not transfer automatically to an enterprise where the same migration has to clear security review, integrate with systems of record, and survive the departure of whoever built it.

That is, of course, the catch. Vibecoding a replacement for a critical PropTech tool is inadvisable for the average real estate firm, and reckless for anything on the critical path. The capability to build custom software cheaply is not the same as the capability to run it safely at scale.

A new generation of firms is rising to bridge exactly that gap across industries, and Outcome is doing it in real estate.

Prasan Kale saw the problem of siloed systems firsthand as a real estate technology entrepreneur. He previously built Rise, a tenant experience platform that VTS acquired in 2021 for $100 million. Rise solved for the front of house, occupant-facing layer, but building it gave Kale a clear view into the mess that is back-of-house real estate operations.

"We saw team members having to do these broken processes where the shortest line from A to B is filled with manual, repetitive, software-centric steps," Kale says. "Getting something done looks more like a zigzag than a straight line."

The zigzag has a specific cause. "Owners and operators have bought so many point solutions over time that the strategic decisions and work actually get done on spreadsheets and dashboards where all of these silos are recombined," Kale notes. Every vendor sold a tidy answer to one question; the operator was left stitching those answers back together by hand, in Excel, at the exact moment a real decision needed to be made.

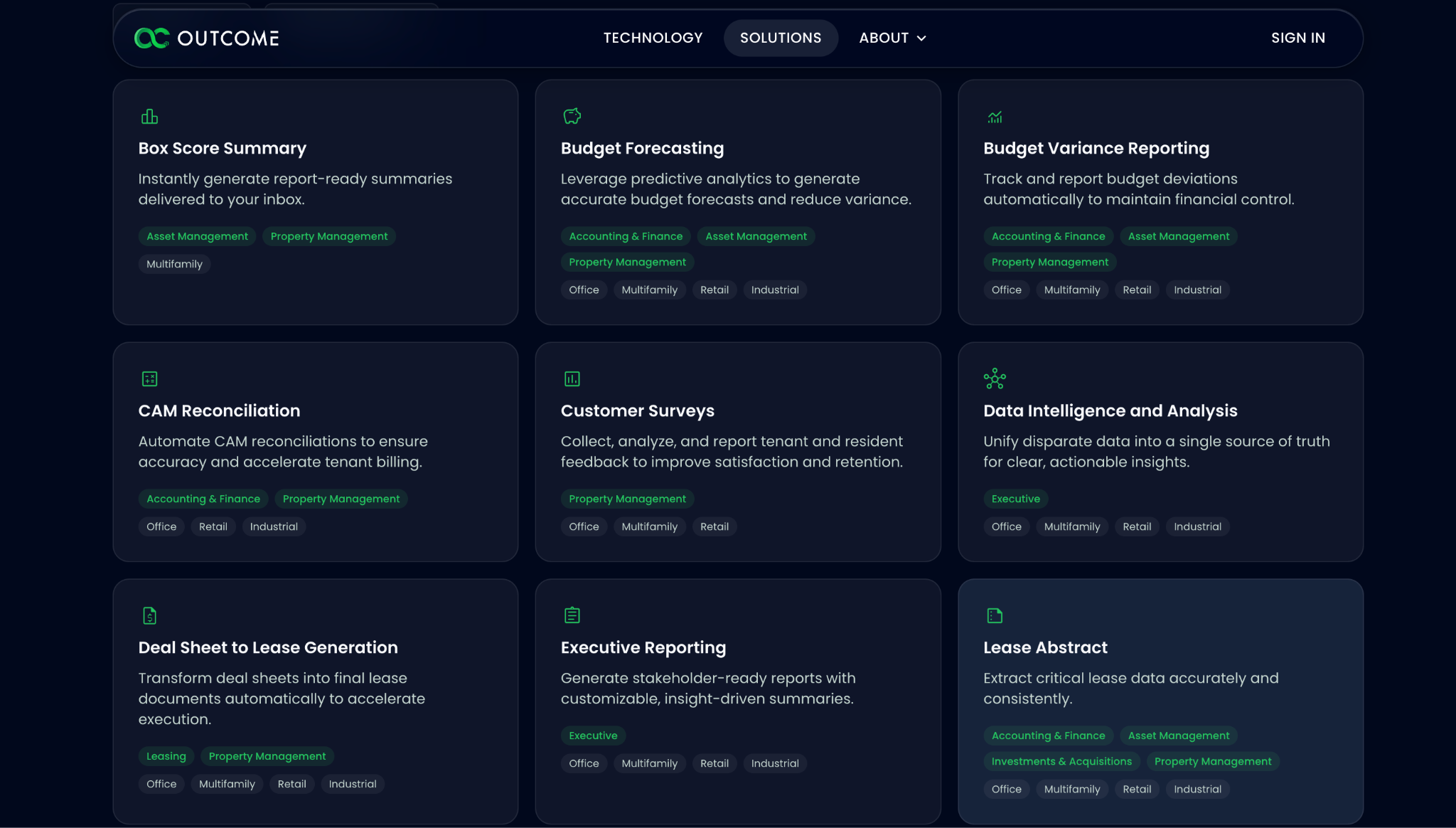

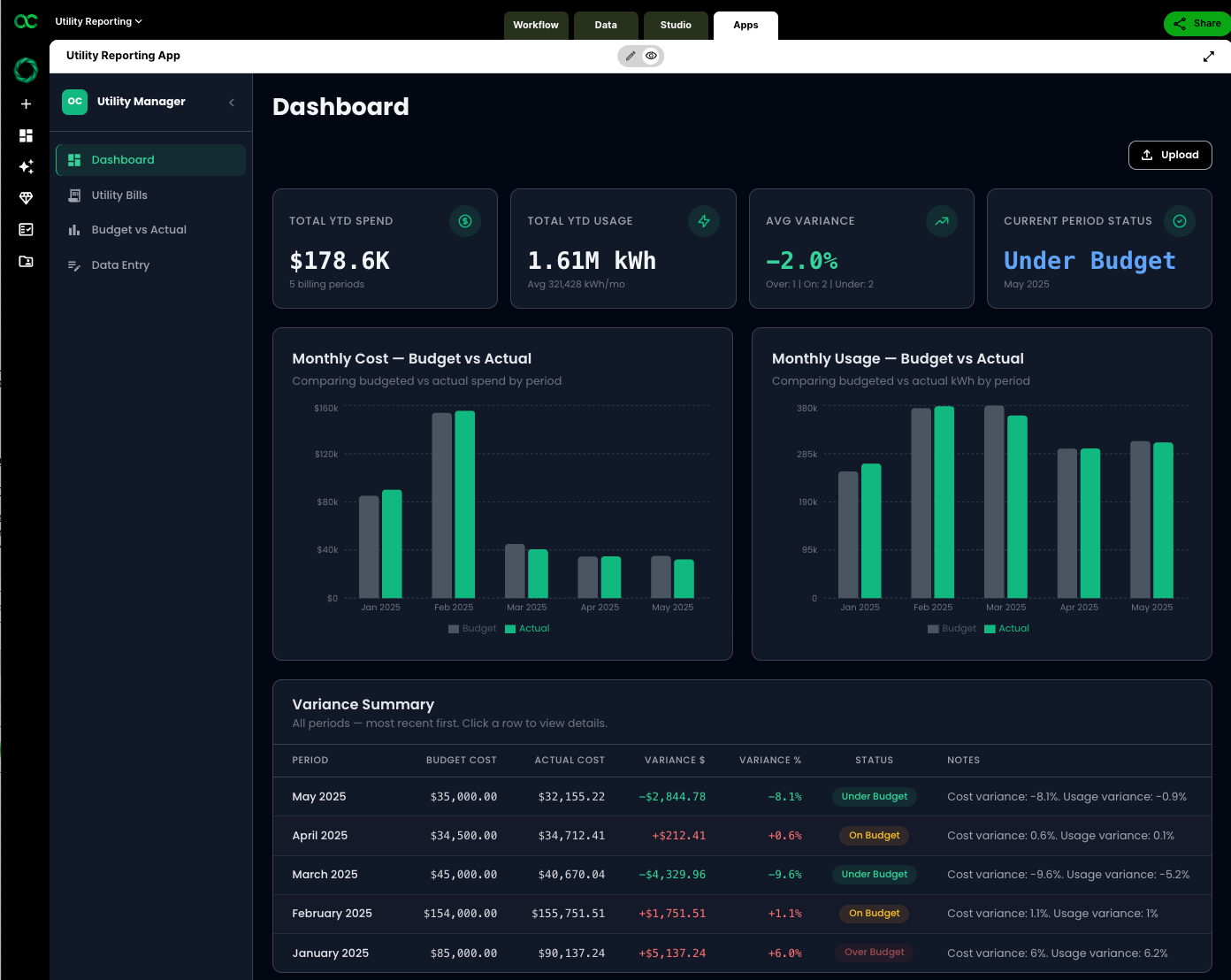

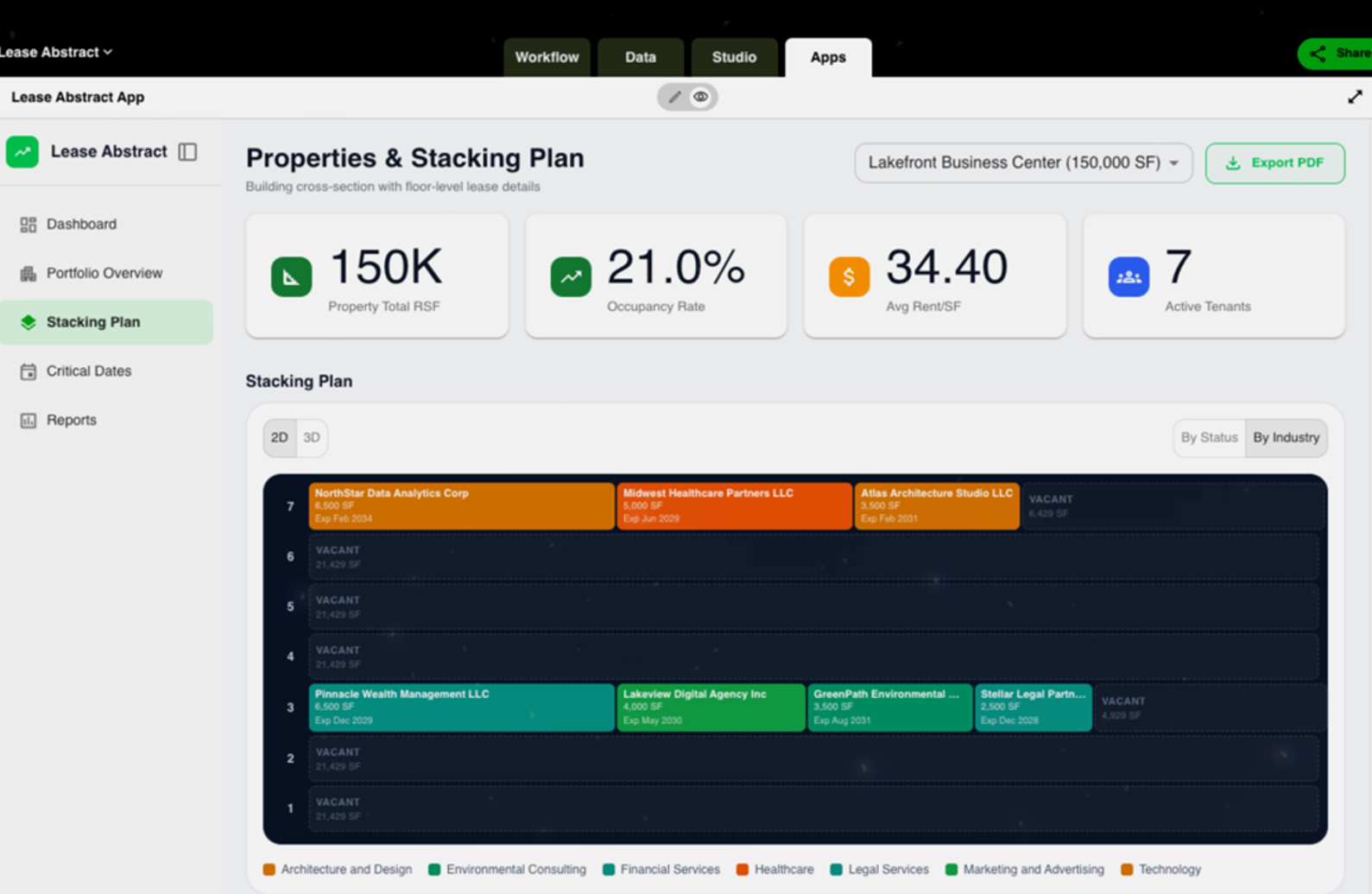

The obvious move would have been to build one platform to unite them all. Kale went the other way. Rather than building yet another system of record, Outcome tackles individual workflows one at a time, assembling a family of custom point solutions it calls "outcomes." In accounting and finance, that means lease abstraction, budget forecasting, variance reporting, and CAM reconciliation. In acquisitions, it means lease and rent roll audits, comp analysis, and offering memorandom (OM) abstraction.

"An analyst can forward an email to an agent with a T-12, rent roll, and OM," Kale says. "It will do a full underwriting and respond to them with a spreadsheet."

None of this is groundbreaking on its own. Plenty of companies do lease abstraction. Others do variance reporting and reporting package drafting. The novel part is how Outcome does it: using AI to customize each implementation to the operator's specific data, integrations, and workflow rather than shipping a fixed feature and asking the customer to adapt.

"This is our single biggest challenge and advantage," Kale says. "It can serve hundreds of use cases across many departments." The company has built close to 90 prebuilt outcomes to date, and the catalog keeps growing.

That breadth is deliberate, and so is the refusal to specialize. Outcome is asset-class agnostic, working across property types rather than taking the easy path of, say, multifamily underwriting. "We like to make things harder on ourselves," Kale says. The result is a single engine that bends to the operator. “Software is shaped around your raw data," Kale says.

The custom, AI-powered approach is not so much a threat to the software industry as a rethinking of what software is in the first place.

"Software is three things," Kale says. "Data, business logic, UI. We have the data, we have the business logic because of the ontology layer, we know how one field or cell affects the other, then we need to figure out the user layer, and tap the power of AI to quickly deliver what their software wants to be." Strip a SaaS product to its parts, and the UI, the thing customers actually pay a per-seat fee to touch, turns out to be the least durable layer. The data and the logic are the assets, and the interface is merely the container.

A frame shift of this scale is not something an operator should approach casually. Two concerns warrant serious consideration before anyone rebuilds their stack around an AI engine.

The first is security, which becomes more pressing with every new AI tool an operator adopts. Most foundation models and application-layer products use customer data to train models or generate aggregate insights, which means an operator's leasing data can become someone else's benchmark report. Outcome has kept every customer’s data entirely separate.

"Your data stays yours forever," Kale says. "It’s not aggregated or shared. We are not publishing benchmark reports on how leasing is going in some zip code. So your data stays yours to the point that it actually sits in a server that is dedicated to you. It’s not a multi-tenant database. It’s a specific dedicated server that we have managed rights on."

The second concern is maintenance, the historical Achilles' heel of custom software. A SaaS vendor pushes one update to every customer at once; a bespoke build tends to degrade the moment its author moves on. Outcome's answer is to keep every implementation living inside its own platform rather than shipping loose code into a customer's environment. "When we maintain our platform, we maintain all the applications within it," Kale says. The custom outcomes inherit the upkeep of the engine that runs them.

All of which rests on a single bet: that AI-powered maintenance actually holds up, that the engine Outcome has built can keep dozens of bespoke workflows current without a human overseeing each one. That is the central assumption of the entire model.

Outcome's initial target is the middle-market operator still running on spreadsheets or a tangle of point solutions. There's a useful parallel to mobile payments in Africa, where entire markets skipped the landline and the bank branch and went straight to the phone. Many operators will skip the SaaS and point-solution era entirely, jumping from spreadsheets directly to agentic applications without ever assembling the multi-vendor stack in between.

The question is whether all of this disrupts the PMS platforms at the center of the industry, and Kale is direct about where the wall sits. "It's increasingly possible to replicate the core platforms without years of work," he says. "But those platforms are the industry standard, and lenders aren't going to accept a proprietary underwriting file in place of the industry standard." The blocker isn't capability. "It's not a technical blocker, it's an industry-standard blocker." Replicating the incumbent tools is now feasible; convincing a lender to underwrite off the replica is not.

That gap won't hold forever. "I think there is a singularity out there on the horizon," Kale says, conceding that it is still far off. "Why does there need to be any software? If you can get all of that data captured one day, then yes, you could replace legacy property management systems."

In recent years, real estate operators have focused on owning their data, specifically the ability to extract key information from walled gardens and control how it moves. The next question is not about owning data, but owning the operating software layer itself.

-Brad Hargreaves

Predicting six new real estate marketplaces to rise over the next decade

The gap between finding an energy inefficiency and fixing it has cost building owners for over a decade. Agentic AI is the first technology that can close it.

Covering the future of real estate and the people creating it