Capital Markets Summit: Who's in the Room

One week out, the people building the next generation of real estate assets are gathering in one room. Thesis Driven&

One week out, the people building the next generation of real estate assets are gathering in one room. Thesis Driven&

The hard part of raising institutional capital isn't the pitch. It's that a pension allocator, an

A data-driven analysis of how real estate GP scale correlates with technology adoption, specialization, asset class, and more

Last month, Thesis Driven brought on former ReZone AI CEO Daniel Heller to run our Operator Database. He’ll be sharing regular insights from the database with Thesis Driven going forward, and today’s letter explores how real estate developers evolve as they scale.

The Thesis Driven Real Estate Developer and Owner Database is the largest compendium of active real estate GPs in the US and Canada, giving us a unique lens into the trends and needs of our 8,400+ active Real Estate GPs, and their 70,000+ principals.

In this article, we’ll focus on GPs sizes, their willingness to adopt new technologies, and investment themes and categories correlate with developer scale.

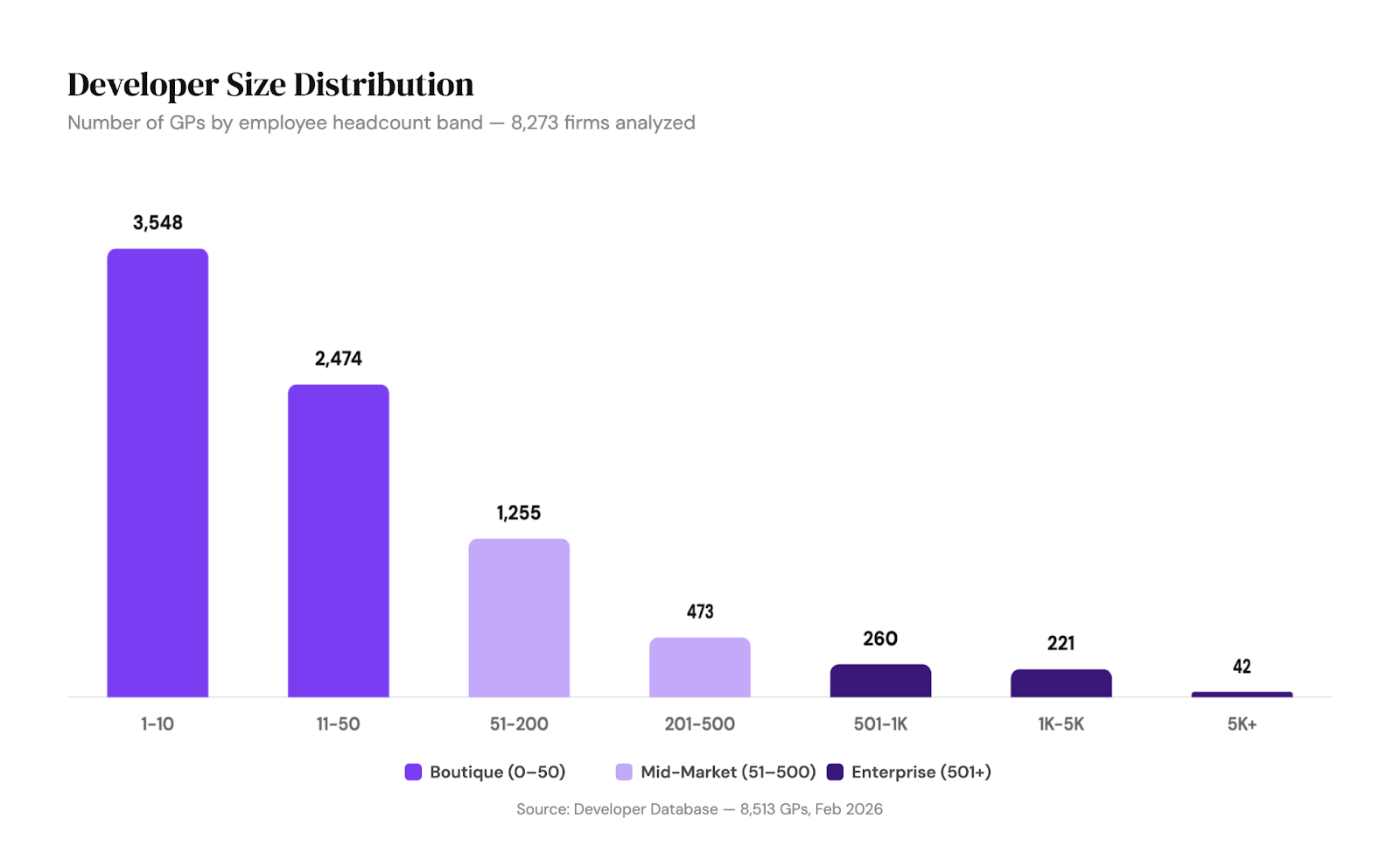

70% of firms have less than 50 employees representing the long-tail of local, relationship-driven developers, while the top 6.3% have 500+ employees; these behemoths are mostly vertically-integrated national or large regional real estate operators.

More than 70% of firms have fewer than 50 employees. The long-tail is real, and it's a significant market segment for anybody selling into real estate operators. These aren’t the names you see on NMHC Top 50 lists or CRE conference panels – They’re the two-partner shops building 20 townhomes in a Raleigh suburb, family businesses buying standalone retail properties, and local operators doing one or two ground-up multifamily deals per year.

At the other end, we have 523 firms with 500+ employees, and only 263 that clear the 1,000 employees threshold. These are the Greystars, the Lennars, and the Hines – firms where a single deal might employ more people than an entire boutique shop.

Caveat: Employee count in itself is an imperfect measure as it inflates the size of vertically integrated operators versus those using third-party management and leasing. However, it is still a useful measure in aggregate.

Boutique firms don't make big press releases. They don't have departments focused on "tech." For vendors, they offer a huge market but low ACV.

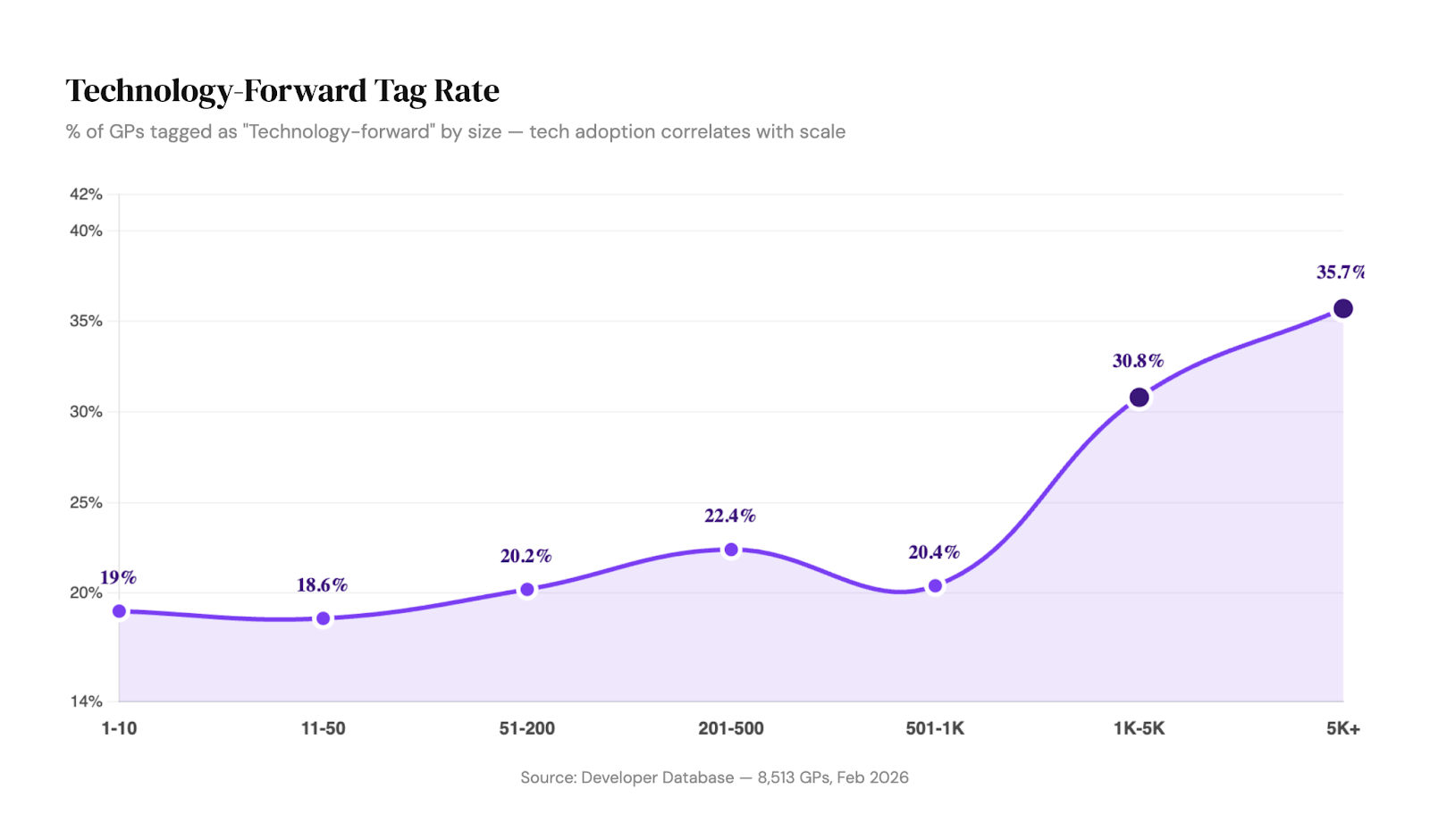

We scanned thousands of company websites, press releases, proptech conference attendance, interview calls, and articles to understand which developers are "technology forward," a subjective measure of their interest in new technology. As a general rule, as real estate operators grow in size, they become more interested in adopting new tools.

However, there’s a significant jump between 500-1k employees and 1k-5k employees.

This structural change might be due to large developers being vertically integrated with operations and therefore have a greater need for operational technology. Another reason might be due to large, publicly traded companies having a market incentive to make noise about their tech-forwardness. (See our breakdown for Q2 25 on “What Real Estate Giants Are Saying About Tech.")

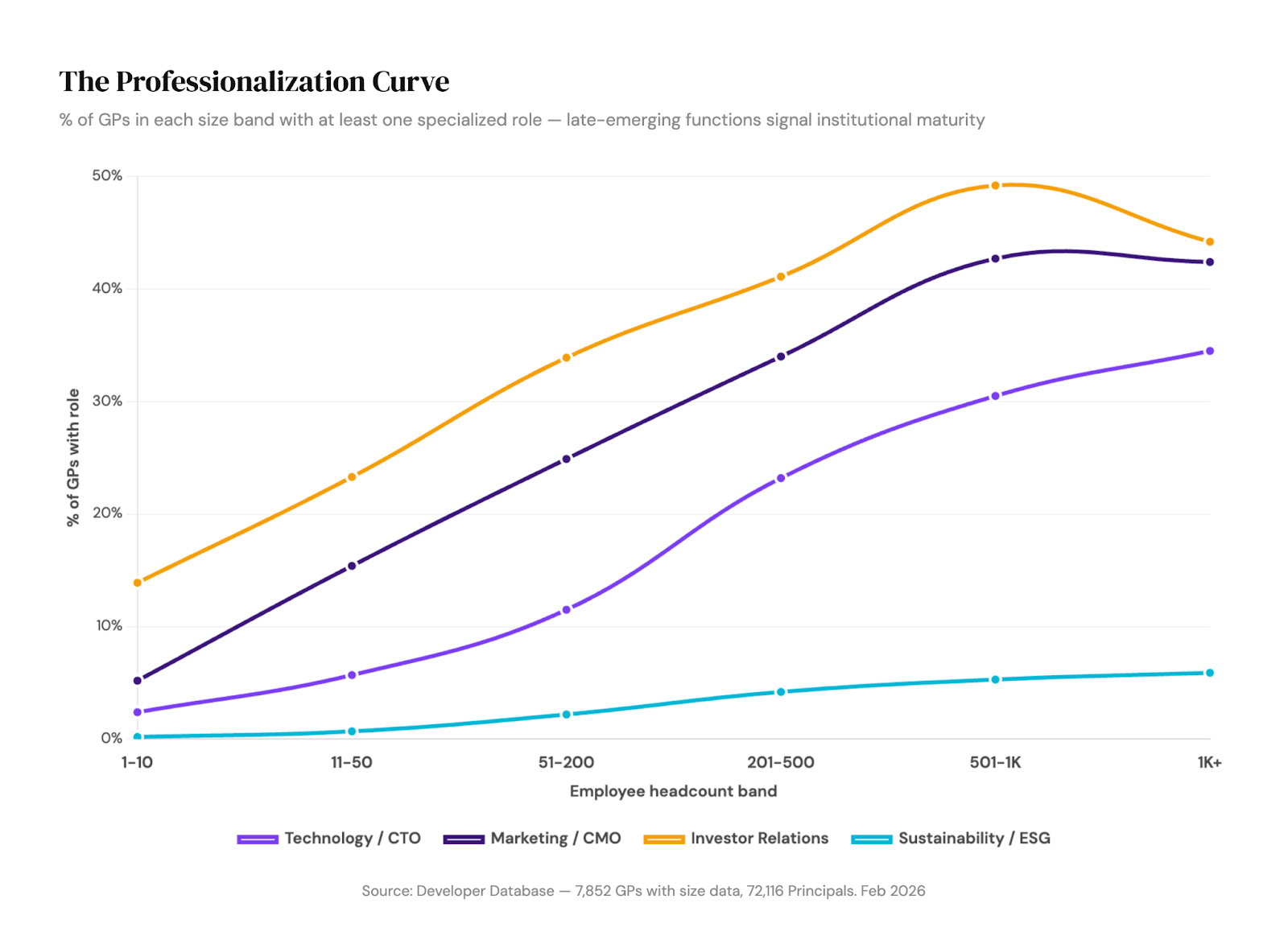

However, getting excited about new tech isn't enough: implementation can be a far more significant challenge and often requires specialized expertise. Our next chart evaluates the presence of these specialized roles – CTO, VP Marketing, IR, ESG – as operators scale.

For vendors and tech companies selling into developers, "Who is my champion?" is a key question.

Marketing and Investor Relations are the most common specialized roles to emerge early, with more than 5% of even the smallest companies (1-10 employees) having these roles.

Technology follows a steeper curve, but starts later. Only 2.4% of small firms have a Tech/CTO role, but by 201-500 employees we see a big jump to 23.2% and by 1,000+ employees it’s 34.5%. The 51-200 band is the inflection point, as the rate doubles from 5.7% to 11.5%. For proptech vendors, this is the rich "middle market" to prospect.

Sustainability/ESG remains a niche function for most firms independent of size. It’s still a role that either doesn’t exist or lives inside another function. For proptech companies building ESG tools, this means you’re selling into firms where your champion probably doesn’t have “sustainability” in their title.

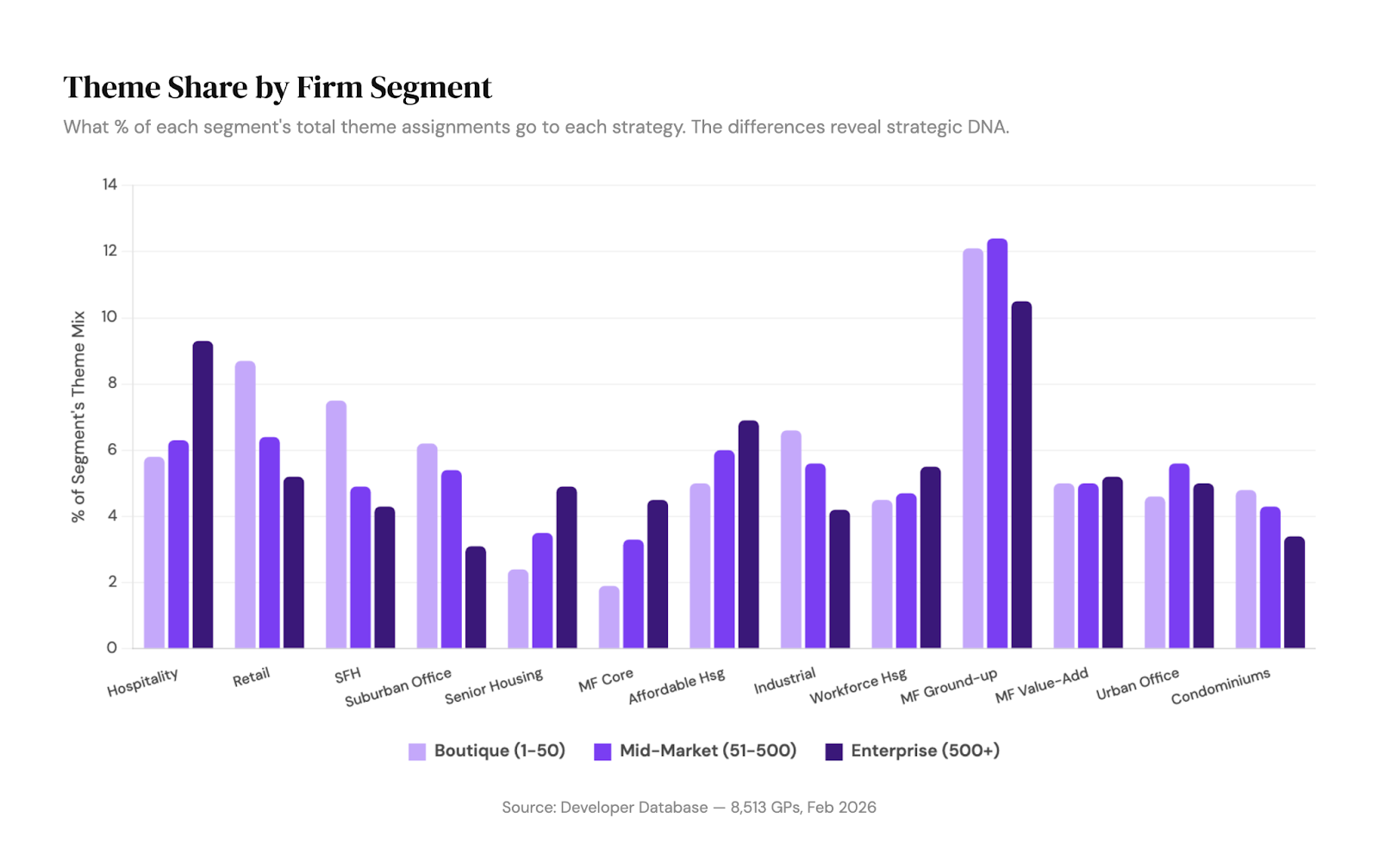

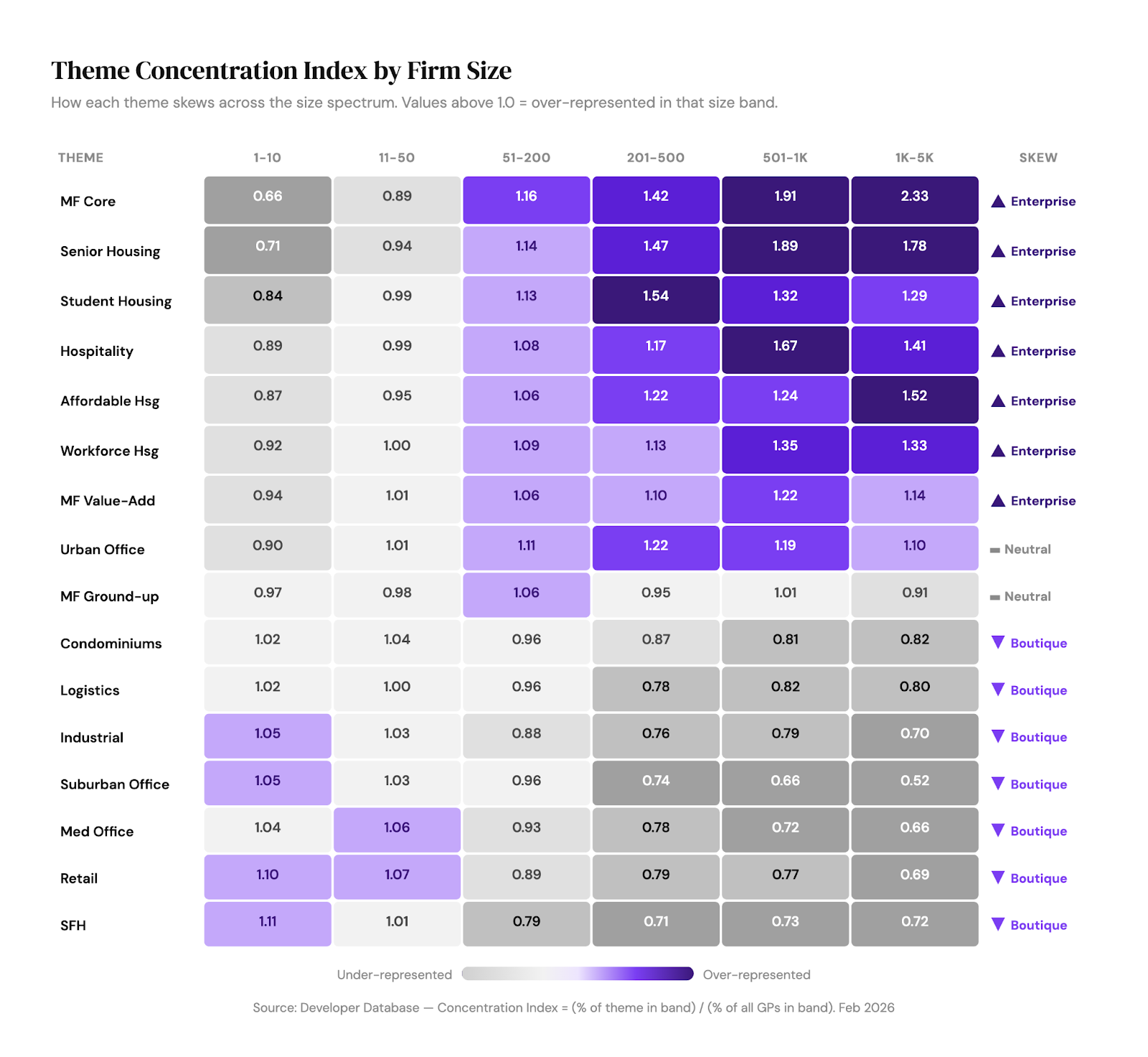

We normalized firm count and looked at what percentages of each segment’s theme mix against each strategy.

Boutique firms over-index on strategies where local relationships are the moat: Retail (8.7% vs. 5.2% enterprise), SFR (7.5% vs. 4.3%), and Suburban Office (6.2% vs. 3.1%).

Larger platforms are more likely to specialize in operationally complex asset classes: Hospitality (9.3% vs. 5.8% boutique), Senior Housing (4.9% vs. 2.4%), and Core MF (4.5% vs. 1.9%). There are strategies that reward larger, vertically integrated teams with more specialized roles.

Ground-up multifamily is the great equalizer: 12.1% of boutique firms, 12.4% of mid-market, and 10.5% of enterprise. Building apartments is universal.

The takeaway for proptech: your product’s value proposition should look completely different for a 15 person boutique shop doing SFR infill than for a 2,000 person platform running senior living communities.

Today, the Developer Database tracks 8,552 Developers and 72,337 principals in 234 markets sorted into 52 themes.

If you'd like a demo, just get in touch with us through the developer database site or reach out to me at daniel@thesisdriven.com

-Daniel Heller

Covering the future of real estate and the people creating it