Why AI Has Struggled to Break Into Mortgage Lending

Stacks of documents, repetitive workflows, and massive economics make mortgage lending an obvious target for AI, but adoption has been slow.

Today’s Thesis Driven newsletter is guest written by Jenny Song, Partner at Navitas Capital, an early-stage venture firm investing in technology for foundational industries such as construction, real estate, energy and infrastructure.

"If we have to switch loan origination systems, I will not be the CEO anymore."

A mortgage lender chief executive said this to us during a recent investment diligence. We were evaluating whether his firm was positioned to deploy agentic AI to automate the loan process, and he understood the opportunity clearly. What he wouldn't accept was the disruption required to get there.

He is far from alone. As venture investors specializing in built world industries, we navigate this reality constantly. The resistance is rarely technophobia, it is structural. And mortgage lending is where those structural forces run deepest.

Residential mortgage lending is, by almost any measure, one of the greatest untapped AI opportunities. The market originated over $2 trillion in loans in 2025, a down year. It has high transaction volume, labor-heavy and document-based workflows, and technology infrastructure that has been largely unchanged for decades. For lenders that modernize, the upside is clear: faster closings, lower origination costs, and the ability to process significantly higher loan volume without adding headcount. These are decisive advantages in a business where margins are thin and volume is everything.

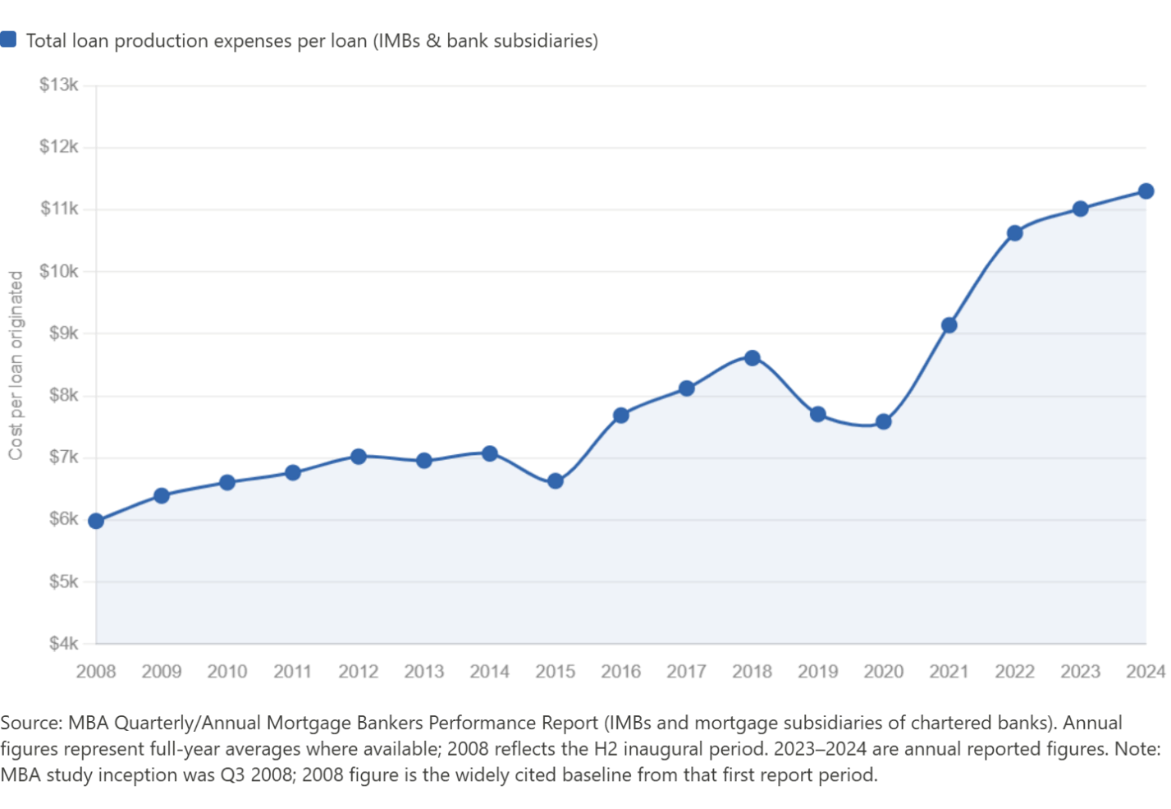

Built world industries have a well-earned reputation for slow technology adoption, but the AI wave has arrived across much of the sector. Apartment owners have adopted AI property management tools, trade contractors have adopted AI call answering and dispatch, and renovation firms have adopted AI for takeoffs and visualization. Mortgage lenders are the conspicuous exception, and the consequences show up in the numbers. Industry productivity continues to decline and lender profitability remains near its lowest point since the Global Financial Crisis.

Why is this the case, and will a new wave of AI start-ups turn the tide?

In this letter, we'll cover:

- The structure of the mortgage market after the financial crisis and Dodd-Frank, and how that shaped innovation and adoption

- The last wave of mortgagetech and what it got wrong

- How AI is being applied to the mortgage industry, and what lenders are doing today

- The most recent wave of startups, the approaches they are taking, and where things are headed

Manufacturing a Loan

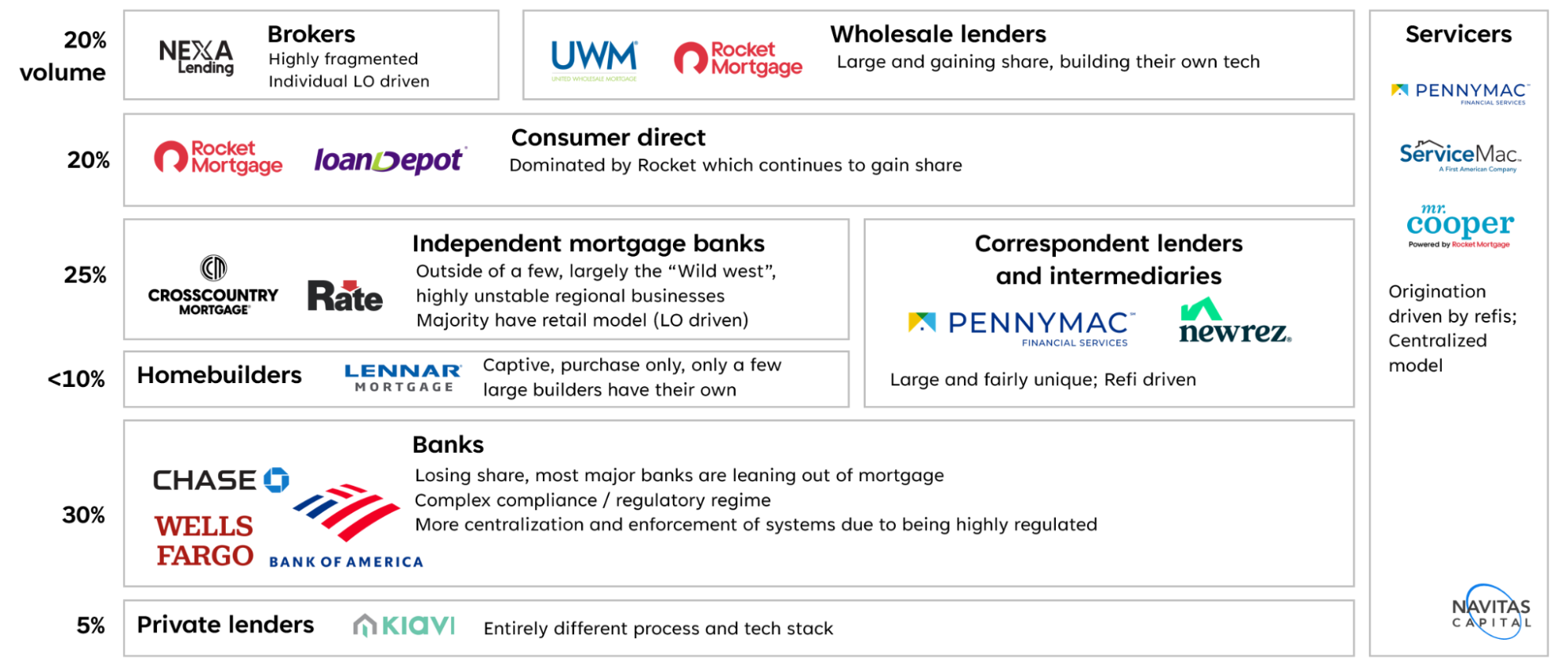

Mortgage lenders are not, in truth, really lenders. Modern mortgage banks, most of which don’t take deposits, are better understood as contract manufacturers, assembling loan documents that meet the standards of Fannie Mae, Freddie Mac, and Ginnie Mae and collecting transaction fees. They’re in the business of moving as many files as possible. They don't assess risk or hold loans on their balance sheet. Their business is throughput and their product is documentation.

After 2008, traditional banks retreated from mortgage lending. Dodd-Frank's regulatory burdens accelerated that exit, and less-regulated independent mortgage banks (IMBs) filled the void. Where traditional banks had owned the entire value chain from originations to servicing, IMBs carved it into pieces: a broker might own the sale, a specialty lender might underwrite and fund, an intermediary might securitize the pool, and the servicing rights might land with yet another party entirely.

What emerged looks almost nothing like other forms of consumer lending.

This complex web of providers, with highly transactional business models and motivations, creates a difficult backdrop for any technology company trying to sell across it. And it produced the opposite of efficiency. With every handoff, paperwork multiplied, data was lost, and the underlying costs of lending kept climbing.

Mortgagetech 1.0

A generation of startups set its sights on the mortgage market with mobile-first experiences and cloud-based software, promising to standardize data, streamline review processes, improve the customer experience, and maybe even make borrowing less painful.

More than a decade later, mortgagetech investors are jaded and billions of venture dollars are gone. The most prominent survivors, Better and Blend, both languish in the public markets, their market capitalizations (each under $500m) trading well below the capital they raised. Better's promise that its technology platform enables more profitable lending stands in sharp contrast to its persistent losses, a stark contrast to Rocket Mortgage, which has built a consistently profitable business at scale. Blend’s numbers are also telling: its revenue declines each year as it cedes mortgage market share and its bank customers shift focus elsewhere.

And these were the ones that made it.

Dozens of other well-funded companies never achieved escape velocity, or were gobbled up by incumbents before fulfilling their visions. The pattern is not unique to mortgage, but the gap between promise and outcome is unusually wide. Industry productivity has only fallen and headcount has remained stubbornly high.

So why has technology adoption in this sector been such a challenge? We see four structural issues:

1. Market heterogeneity. The firms that originate mortgages are extraordinarily diverse in structure, function and need—and that diversity is a trap for software startups, who would prefer to build one uniform product for customers who all look alike. A broker, a national bank, a credit union, a homebuilder with a captive mortgage business: each operates under a different business model, regulatory regime, and software stack. A product that works for one rarely ports to another. Blend won in the bank segment and never meaningfully broke out of it. Startups that chase the whole market tend to end up confined to small TAMs.

2. Boom and bust. Mortgage lending is intrinsically tied to interest rates, and because revenue is driven entirely by origination volume rather than assets under management, the business is inherently cyclical. There is almost never a good time for technology adoption. In boom times, lenders are too busy processing loans to learn new systems. In slow times, they are cutting costs and hoarding labor for the next upswing. The window for meaningful technology investment is vanishingly small.

Even when startups do gain traction, the boom-bust dynamic forces them into transaction-based pricing. That aligns the product to value, but makes recurring software revenue nearly impossible to build.

3. Slow pace of decision and implementation. Mortgage lenders are in the business of minimizing risk. The whole manufacturing process is effectively CYA: documenting to the nth degree so that a mortgage file never comes back to the lender. This culture pervades decision-making.

Many lenders are also highly decentralized. Transaction volume is king, and loan officers (LOs) control it through local relationships with realtors, wealth managers, and real estate investors. Most lenders grow through recruitment of the best loan officers, much like real estate agencies. LOs carry significant organizational cachet, and lenders are careful not to upset them. A change in tech risks alienating the people who generate the revenue, so it is often better avoided.

Even when startups win a hard-fought customer, implementation and expansion cycles in mortgage are some of the longest in any industry. It can take years to win an entire account, and years more to roll out from one office to another.

4. Sticky incumbents. Encompass, owned by ICE Mortgage Technology, is the 800-pound gorilla of loan origination software. Clunky and archaic, it is the backbone of the market, with 60-70% share. It also dominates servicing software and other components of the tech stack. Most organizations using Encompass have customized it extensively and invested millions in implementation. Because the LOS is the system of record for all compliance processes, it is nearly impossible to displace.

Every startup in the mortgage ecosystem faces the same strategic question: do they play nice with Encompass? The vast majority comply, paying hefty fees including a 20% revenue share to integrate. Compliance, though, only entrenches the incumbent further. Startups end up as widgets within the Encompass platform, unable to own larger workstreams. It is a trap dressed up as a distribution strategy.

The Promise of AI

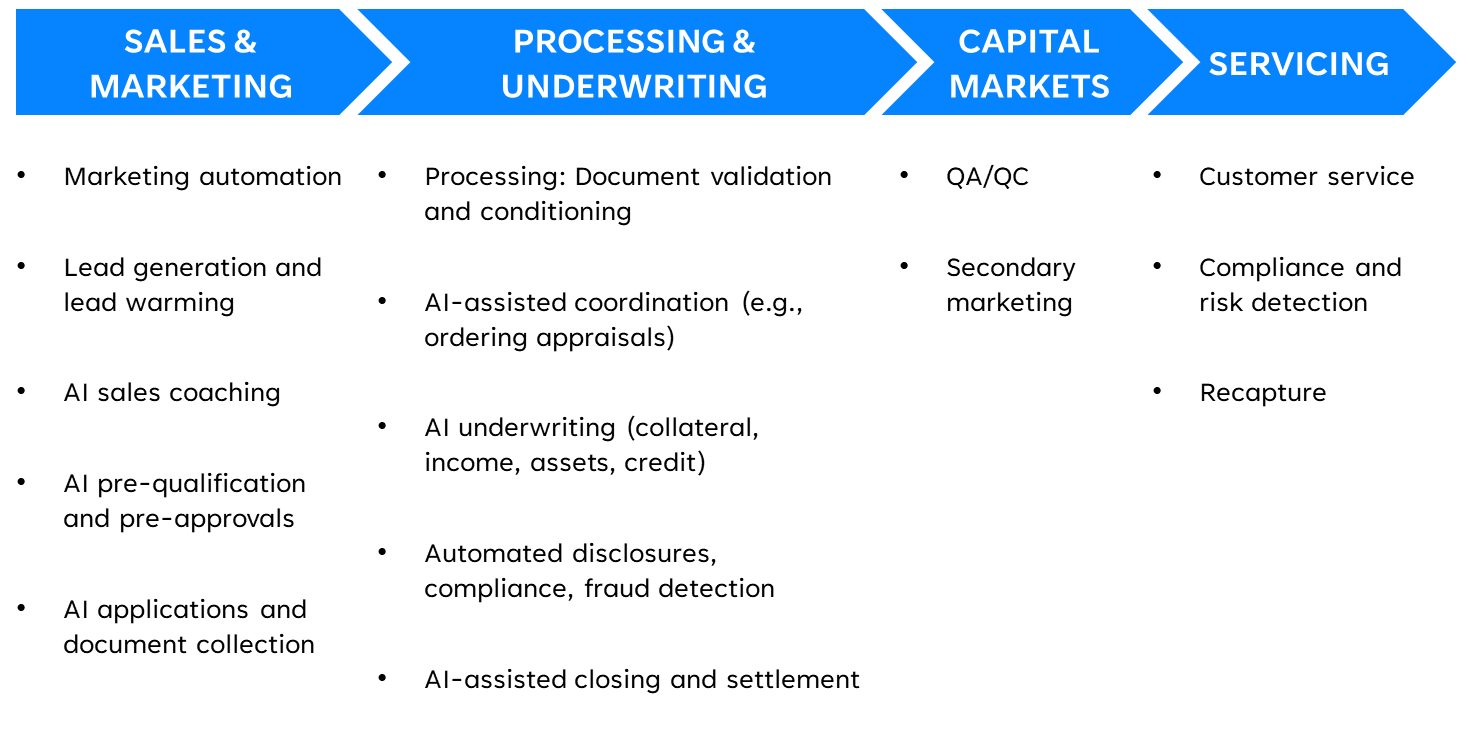

None of this makes mortgage an unattractive AI opportunity. Across the value chain, the openings are everywhere.

In processing and underwriting in particular, the opportunity is massive: these are workflows largely based on reviewing documents and checking them against written guidelines and checklists. Mortgage lender executives are quick to paint the picture of a future with fully automated applications and approvals, quick closings, and no messy paperwork.

Lenders are taking several distinct approaches. Large ones like Rocket Mortgage and UWM have largely built their own tech stacks over time and are layering AI into those systems. They are, in some respects, path dependent: with all the investment they’ve made in existing systems, they’re less able to incorporate new off-the-shelf solutions. What they have instead is data: as market leaders, both sit on proprietary loan datasets that no startup can match. Both have made AI a prominent part of their marketing: Rocket to investors, UWM to brokers, pitching a tech-forward origination platform.

Many other lenders are choosing instead to partner with AI startups, often with multiple providers simultaneously even when those startups have overlapping roadmaps. Given that few mortgage tech apps have historically managed to expand their scope, the patchwork approach feels logical: most lenders would prefer to work with one AI vendor, but no single startup is likely to cover all ground quickly.

The third approach goes the deepest: uprooting existing systems to replace them entirely with AI-native systems of record. Few lenders attempt it because the organizational disruption can be enormous: it affects the most employees and requires large-scale rewiring of processes. Lenders tend to describe it as open heart surgery.

Most AI app layer startups pitch system of record replacement as their long-term goal: embed deeply enough into workflows, accumulate enough data and interactions, and the legacy system becomes irrelevant. No current app layer company in mortgage is close to that, which is why some lenders are concluding that the painful switch is unavoidable if they want to fully adopt agentic workflows.

AI Progress

Widespread AI adoption in mortgage is still early, especially in core loan manufacturing where the efficiency impact might be greatest. The theoretical applications of the technology are obvious; the complexity of the industry is where it breaks down.

Many loans are clean and AI can handle their paperwork efficiently, but so can an experienced processor or underwriter. That is not where the value is. The 80-20 rule applies: 20% of loans take 80% of the effort, and the same ratio holds for AI. The cases AI cannot yet handle are precisely the ones most worth automating. Most startups don't have enough data to automate at the accuracy levels the industry requires. As one Rocket Mortgage executive put it, there are simply too many permutations in mortgage for anyone to achieve that level of performance. The data that does exist is messy and requires significant cleaning before it can be used.

Most startups recognize this and know they must achieve high accuracy within one wedge use case and gain trust before expanding into more of the process. The shared vision is full automation of loan manufacturing. The disagreement is over where to start and what gives any one company the right to expand from there.

The current wave of startups is notably more experienced than its predecessor. Many are repeat founders who came up through earlier mortgagetech or fintech companies and learned the hard lessons firsthand. That credibility has been enough for major lenders like Pennymac and Newrez to commit early. The key questions remain: how quickly can any startup translate early partnerships into broader acceptance, and how can they earn the right to own more of the process while navigating the incumbent relationships that constrain them. Vesta is the one exception, in outright competition with Encompass rather than uneasy accommodation.

Our view is that technical capabilities will follow commercial and competitive success, not the other way around. Access to data and bespoke processes are the bottlenecks, not the underlying technology. The value is there to be had.

The choice facing mortgage lenders is not whether AI will reshape their industry. It is whether they will be the ones doing the reshaping, or the ones being reshaped.

Our Predictions

- When interest rates eventually fall and refinancing volume returns, the lenders that went through the pain of upgrading their tech stacks during the slow period will be positioned to capture massive share, processing loans faster and more cheaply than those that didn't. AI-native loan origination systems will see their highest adoption in refi-heavy segments, particularly servicers and direct-to-consumer lenders, and those segments may be large enough to produce a meaningful standalone business.

- AI-native brokerages will emerge as a competitive force in purchase transactions. The broker channel has been gaining traction and brokers still own the human relationships with realtors and buyers. AI-native brokerages that provide a full agentic tech stack in addition to back-office functions like licensing and compliance can win the best teams by eliminating tedious paperwork, improving margins, and allowing LOs to focus on relationships.

- Another wave of AI-native IMBs is coming, though winning against Rocket Mortgage will be no easier than it was for Better. The smart ones will acquire existing IMBs rather than build from scratch, because scale loan volume is required to generate the AI efficiencies that justify the model. Rocket's data advantage, accumulated over decades, remains the hardest thing in the industry to replicate.

This isn't a winner-take-all market. AI adoption will be shaped by the same fragmented forces that came before it, but it will leave its own imprint on market dynamics too. At some point, mortgage lenders will have to break free from their earlier patterns and invest the time and resources to adopt new technology, or the productivity gap will become so great that they'll be disrupted by those who did.

—Jenny Song

Read next

The Least Glamorous Job in Real Estate Is Getting Sexier

As AI eliminates administrative burden and capital consolidates around scaled platforms, operational performance is becoming a primary driver of returns

Reinventing the Tribe: RidgeRunner and the New American Village

How a new model for rural communities built on shared identity is driving both demand and backlash

The Winners and Losers of America’s Demographic Future

Falling birth rates, shifting migration, and an aging population are already reshaping demand across real estate, faster than most of the market has priced in

Food Culture Is Real Estate

How a generation of superstar chefs and obsessed diners remade urban neighborhoods, inflated rents, and priced themselves out of the streets they made desirable.