How to Raise Capital from Family Offices and RIAs

Private wealth has passed the institutional market, and most sponsors have no idea how to reach it. A workshop on raising from family offices and RIAs.

Private wealth has passed the institutional market, and most sponsors have no idea how to reach it. A workshop on raising from family offices and RIAs.

EG is applying the American real estate private equity playbook to Australia, starting with medical office

Our annual list of firms actively investing in real estate technology companies

As drone deliveries expand across the Sunbelt, opportunities for real estate investors and operators emerge

Over the past decade, logistics real estate has emerged from the fringes to an institutional-quality asset class. Other related typologies like industrial outdoor storage (IOS), cold storage, and EV charging have followed, walking the line between traditional real estate and infrastructure while attracting billions in investor capital.

Today’s letter will explore drone charging hubs as the next category of logistics real estate to take off, so to speak. Drone delivery, which uses fully autonomous, battery-powered aircraft to move small packages directly to homes and businesses, is emerging as a solution to last-mile delivery, and recent deregulation could drive rapid expansion of the category.

All those delivery drones need space for charging, storage, and maintenance. For real estate developers and investors, this means the emergence of a new category of logistics real estate: small sites required for operating delivery drone fleets. That network of drone charging hubs must be leased, entitled, built, and operated, creating a new asset class at the intersection of industrial, retail, and technology real estate.

This Thesis Driven letter will explore:

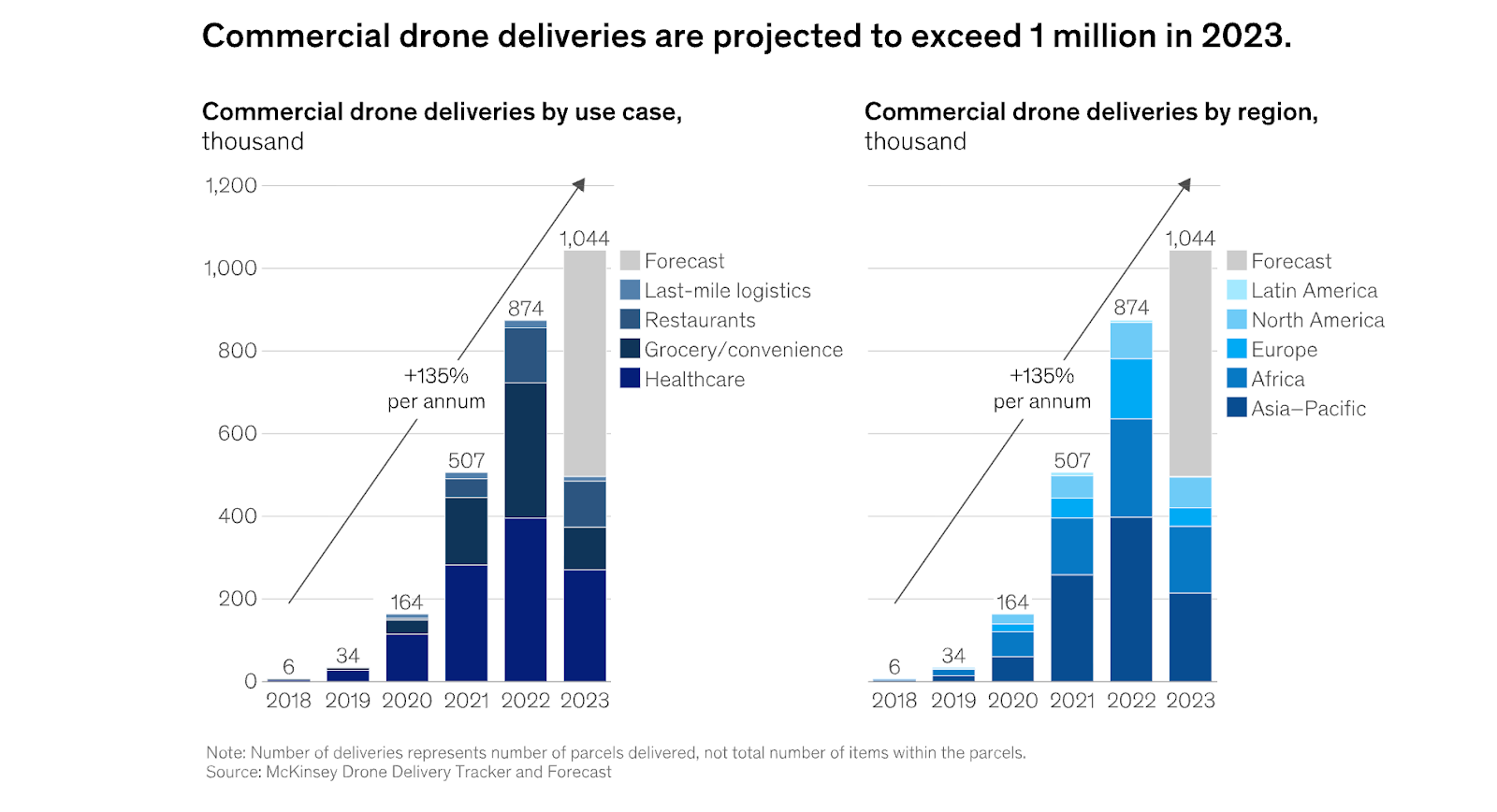

Drone delivery has quietly transitioned from demonstration to deployment. For years, headlines and prototypes dominated the conversation. But over the past 24 months, two operators, Zipline and Wing, have rapidly scaled up operations in the US. Together, they’ve now completed more than two million commercial deliveries globally with a rapidly growing share in the United States. Today, Zipline makes a commercial drone delivery every 60 seconds.

Other entrants like Flytrex, Amazon Prime Air, and Manna Aero are also growing quickly, each refining their commercial models and expanding test markets.

Retail adoption is the major accelerant. Walmart has become the first large retailer to integrate drone delivery at scale, operating across 40+ SuperCenters in Dallas–Fort Worth and completing over 300,000 deliveries in its first year. That network is now expanding to another 100+ SuperCenters in Atlanta, Orlando, Houston, Tampa, and Charlotte by the end of 2026. Walmart is turning stores into neighborhood fulfillment nodes for drone delivery. Chipotle, Sweetgreen, and DoorDash are among the brands that have already signed on with drone operators, with new announcements across retail, food, and healthcare coming almost monthly.

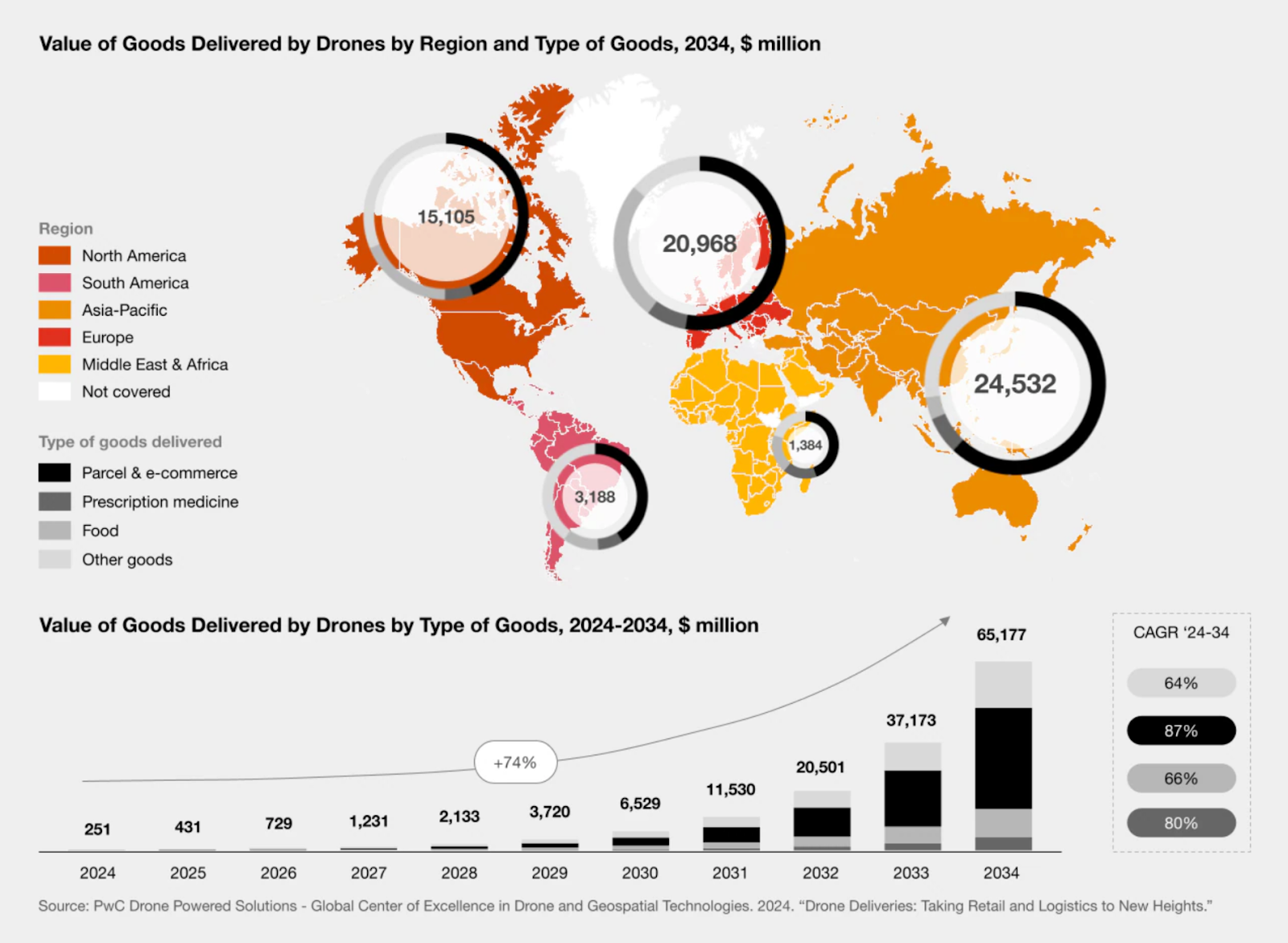

Retail and technology analysts are closely watching the drone delivery trend. A 2023 McKinsey study noted the dramatic increase in drone deliveries and anticipated accelerating growth in the coming years. Amazon alone anticipates 500 million drone deliveries by 2030, and a recent PwC study projected a 74% CAGR in the value of drone deliveries through 2034.

Until this year, regulatory questions remained a major blocker to widespread adoption of drone delivery. Historically, drone operators needed special FAA permission to fly drones beyond visual line of sight (VLOS), a requirement for any feasible drone delivery operation. But the June 2025 White House executive order “Unleashing American Drone Dominance” directed the FAA to finalize Part 108 by February 2026, providing a new operational framework to enable drones to operate safely at scale.

(Related to the above, drones are increasingly seen as the future of warfare, driving technology costs down as state actors including the US and China invest in scaling the manufacturing and development of commercial drones that could also have military applications.)

Like self-driving cars, drone delivery is still in the realm of “see it to believe it.” For readers living in Europe or big northeastern US cities, drone delivery may seem on par with fusion power or quantum computing – cool, but far out on the horizon. But for residents of a number of Sunbelt cities, it’s increasingly the retail reality.

If any readers live in or are traveling to Dallas, for instance, we recommend visiting one of the live Walmart drone delivery sites; there are more than 40 active in the Metroplex. But if you’re on the other side of the country, this video may provide some color:

In short, technology, policy, and retail adoption have aligned, setting the stage for large-scale deployment.

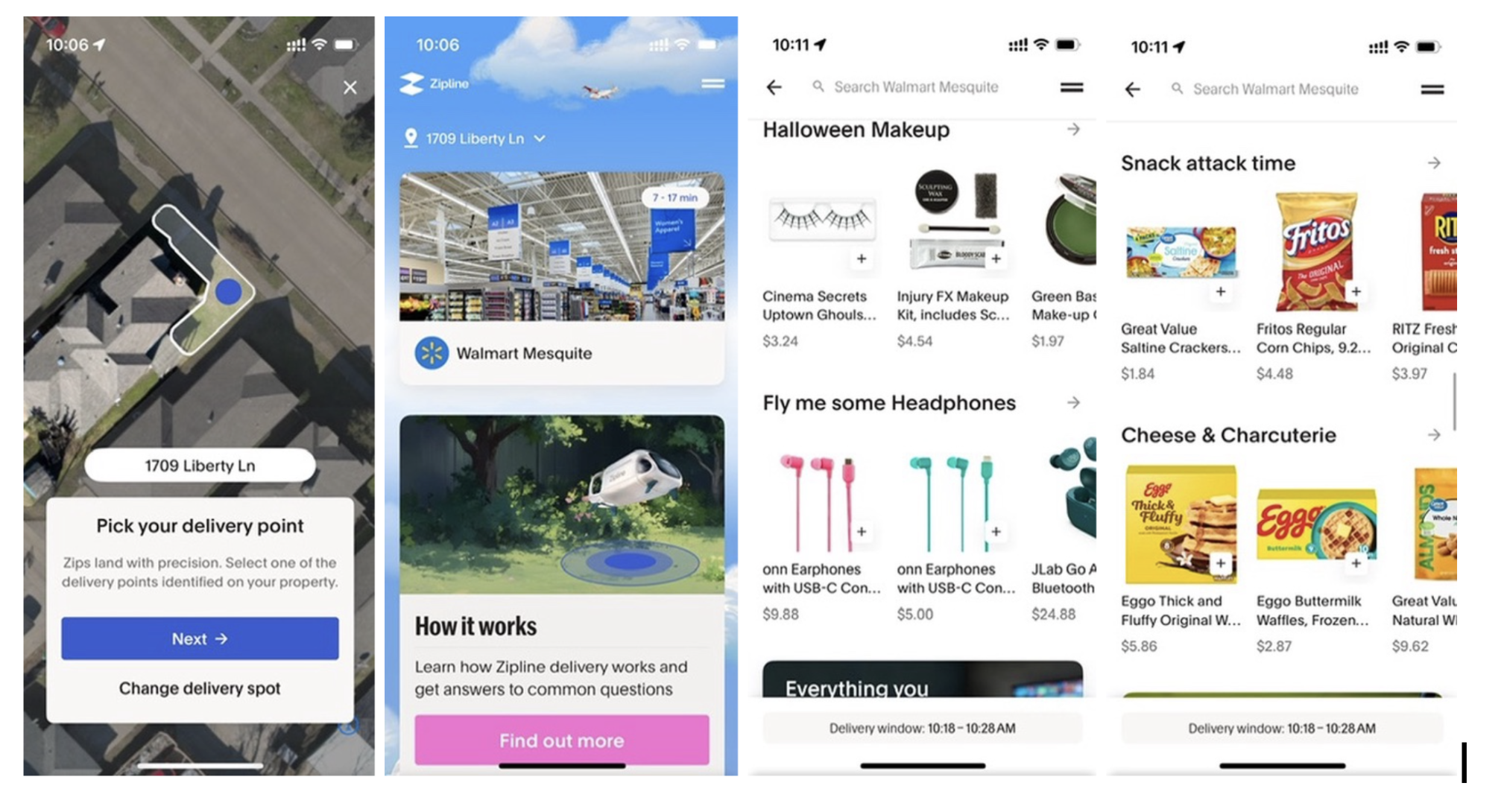

Modern delivery drones are lightweight, electric, and fully autonomous, designed to carry payloads of 5–8 pounds within a 5–10 mile radius. Using redundant navigation systems and onboard sensors, they fly autonomously to deliver packages. The packages are lowered on a tether, keeping propellers safely above people and property.

For consumers, the experience mirrors on-demand delivery: order through an app, pick a delivery spot, and track the vehicle en route in real time. (Except it’s a drone, not a DoorDash driver.) Multifamily sites and mixed-use areas designate coordinated drop zones—similar to rideshare pickup points.

From a real estate perspective, the importance lies in standardization and repeatability. Each flight originates from a small, modular pad site, meaning the infrastructure model can scale quickly across metros. These repeatable footprints, called “drone charging hubs,” represent the next monetizable layer of last-mile logistics.

Drone delivery networks currently rely on two primary site types: Store-Integrated Charging Hubs adapted for large throughput sites (e.g., Walmart) and Neighborhood Charging Hubs that serve multiple partners (ex: Coffee shops, pharmacies, restaurants).

A. Store-Integrated Charging Hubs

B. Neighborhood Charging Hubs

Both types of drone charging hub share a few features in common:

Fortunately for real estate developers, drone charging hubs are generally operator agnostic. As of today, all the major drone operators have fairly similar requirements: a permitted and fenced-off site with power and data fed to the enclosure ready to lease.

As we’ll discuss in the next section, charging hubs are typically leased to drone operators, which manage all aspects of drone operations and install their proprietary charging stations. Landscaping (when applicable), fencing, maintenance, and security are the main responsibilities of the real estate owner.

The success of these networks depends on density: the more nodes per metro, the lower the per-delivery cost and the more sustainable the model. For property owners, that translates into durable leasing demand for strategically located charging hubs.

For industrial owners, underused asphalt or back-of-house areas are prime candidates for neighborhood charging hubs. Industrial infill sites are especially attractive as they are closer to population centers. Terms typically include:

For retail landlords, drone hubs become tenant amenities, expanding store trade areas from 3–5 miles (typical for car delivery) to 6–10 miles, increasing tenant sales and center relevance. Most hubs occupy under 8,000 SF of edge parking – non-disruptive to shoppers, yet highly valuable to tenants.

The result is new, recurring NOI from compact footprints that strengthen both tenant performance and asset positioning.

The key to delivering this new network of drone charging hubs quickly is bringing real estate capital and domain expertise under one roof. Too often, drone operators approach traditional property owners with proposals that feel unfamiliar: complex terms, high improvement costs, and little precedent. At the same time, many owners interested in participating don’t know whether their sites are well positioned or even permitted for this emerging use.

As a developer, we help bridge that gap by identifying, entitling, and developing (with LP capital) strategically located charging sites that meet both regulatory and operational criteria. We then rent those to drone operators. We’re currently advancing 25+ neighborhood-scale sites across Dallas-Fort Worth to be delivered to operators by the end of 2026, and we’re beginning site selection in high-demand metros including Charlotte, Atlanta, Houston, Orlando, and Tampa.

Underwriting drone infrastructure combines land use and airspace feasibility.

Every metro will be different, but sharing some insights from our land use experience permitting 20+ drone charging hub sites in the Dallas Fort Worth Metroplex, Utah, and Arkansas:

Airspace constraints are now a primary site selection variable including proximity to airports, helipads, schools, and controlled airspace classes. A parcel’s value for drone use is determined as much by its flight corridor access as its zoning designation.

In practical terms, underwriting drone sites now means running a dual analysis: ground feasibility and airspace feasibility. The best sites score high on both.

Drone delivery is evolving from concept to commercial infrastructure. Scaling it will require dozens of small, standardized pads per metro - each leased, powered, and permitted. As a developer, we underwrite airspace and land use, match active operators, and structure charging hub leases that add durable NOI with minimal disruption.

-Benoit Miquel

About the Author

Benoit Miquel is the founder and CEO of LM4 Partners. LM4 works with owners and drone operators to:

Previously, Miquel led Zipline’s real estate team for six years overseeing site development across seven countries and multiple U.S. States, including Utah, Arkansas, and Texas. With a background in commercial construction and development, he now develops last mile delivery sites across the US. He earned degrees in Civil Engineering from McGill University (B.S.) and Stanford University (M.S.).

He can be reached at benoit@lm4partners.com

Predicting six new real estate marketplaces to rise over the next decade

The gap between finding an energy inefficiency and fixing it has cost building owners for over a decade. Agentic AI is the first technology that can close it.

Covering the future of real estate and the people creating it