The Deals Developers Are Analyzing Today | Q2 2026 Edition

A quarterly read on early-stage feasibility activity with our friends at TestFit

A quarterly read on early-stage feasibility activity with our friends at TestFit

We're going long on print. This October, we are releasing the first edition of Thesis Driven in physical

As the spigot of institutional capital remains dry for many real estate sponsors, family offices have become an increasingly sought-after source of capital.

But for real estate operators unfamiliar with family offices, they can be frustrating and confusing partners. Without the pressures of a fund’s lifecycle pushing capital out the door — and all manner of investment opportunities at their doorstep —getting family office capital often seems like a never-ending trek.

One reason? “Family office” is a broad term encompassing a wide variety of different types of firms, from massive RIAs to small single-family offices. For a real estate sponsor, building a family office strategy requires understanding the types of family offices that are out there and how they differ.

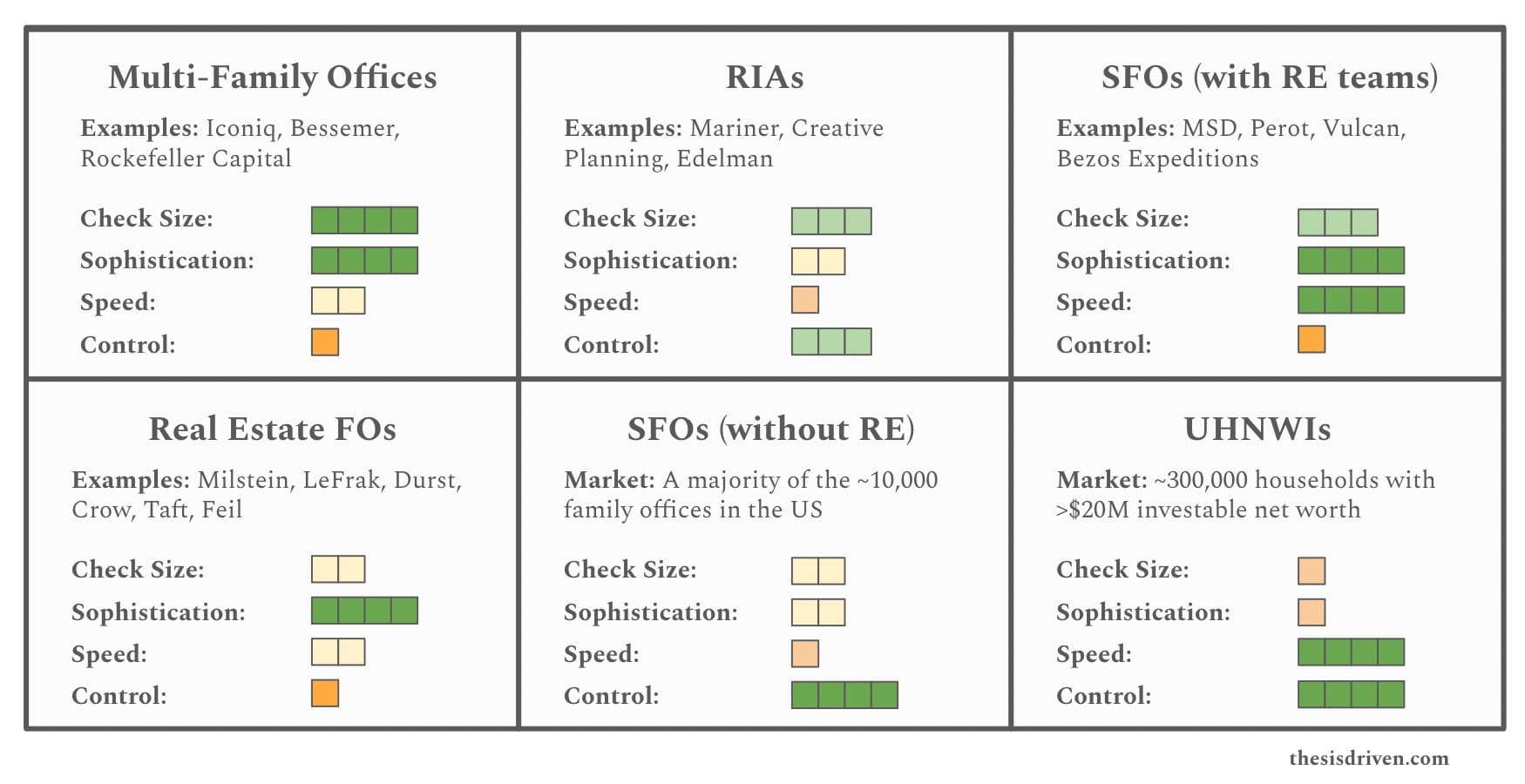

Today’s letter will attempt to shine a light on this, exploring the six types of family offices you’ll meet and how each varies in check size, sophistication, and approach. Operators can also map 4,500+ family offices to the asset classes they actually back via CapitalStack.

—

If you’d like to go deeper, check out our Raising Capital from Family Offices & RIAs workshop.

—

We evaluate and divide family office firms across four dimensions: typical check size, sophistication, speed, and control required:

Now let's dig into each type of investor:

(1) Large Multi-Family Offices (MFOs)

Examples: ICONIQ, Bessemer Trust, Rockefeller Capital Management

Typical Check Size: $10M+

Typical Sophistication: Moderate-to-High

Typical Speed: Moderate

Control Required: Moderate-to-High

While large MFOs are family offices and therefore belong on this list, their behavior is somewhere between traditional single-family offices and institutions. Like other family offices, MFOs can have a long investment time horizon, and they care a lot about tax efficiency and estate planning for their clients. MFOs can also get creative about asset classes and deal structure, and – like their single-family peers – can move quickly when needed.

But MFOs' scale allows them to have a level of sophistication closer to that of institutions or real estate private equity firms. They typically have dedicated real estate investment teams, and they aren't scared off by complexities such as joint ventures or platform investments.

This combination of sophistication and flexibility means that MFOs do some of the most interesting deals in real estate – such as ICONIQ's backing of flex rental operator Sentral+.

(2) Registered Investment Advisors (RIAs)

Examples: Mariner, Creative Planning

Typical Check Size: $1M - $50M

Typical Sophistication: Moderate

Typical Speed: Low

Control Required: Moderate-to-Low

Registered Investment Advisors (RIAs) are wealth management firms that oversee client assets. While some RIAs act like family offices, the biggest ones behave much more like institutional allocators. Firms such as Creative Planning (over $370B in assets under management/advisement as of mid-2025) manage thousands of ultra-high net worth households, with many clients having $10M+ in assets. These RIAs are increasingly offering private markets, alternatives, and real estate exposure to their clients — often via feeder funds or co-invest vehicles.

RIAs with these resources typically have internal due diligence, compliance, and reporting teams (or use third-party platforms) which allows them to back more complex real estate deals — joint ventures, value-add, and opportunistic strategies — assuming the sponsor can meet their standards.

That said, working with RIAs has downsides for real estate operators. First, check sizes are often smaller than those of institutional LPs, with stricter limits on illiquidity and lock-ups due to client suitability requirements. Second, the process tends to be slower: multiple layers of approval, compliance, alignment with client risk profiles, and often significant documentation (legal, financial, tax, etc.). Third, RIAs are sensitive to fees and transparency; if your structure has high carried interest or opaque cost layers, you may be filtered out. Finally, while RIAs can provide repeat capital, they may also pull back after market shocks more quickly than long-horizon institutions, increasing deal risk in downturns.

(3) Single-Family Offices with Dedicated Real Estate Teams

Examples: MSD, Perot

Typical Check Size: $5-50M

Typical Sophistication: High

Typical Speed: High

Control Required: High

For real estate operators, the 10,000 or so single-family offices in the US can be split into two broad categories: those with dedicated real estate investment teams, and those without. To begin, we'll talk about the first group.

Single-family offices with dedicated real estate teams are similar to multi-family offices with two major exceptions:

This also means they can move remarkably fast for family offices, quickly making decisions to back – or avoid – a category and operator.

(4) Real Estate Family Offices

Examples: Milstein, LeFrak, Durst

Typical Check Size: Varies

Typical Sophistication: Moderate-to-High

Typical Speed: Moderate

Control Required: High

Real estate family offices are similar to the previous category of single-family offices with one big exception: these families made their money in real estate rather than building their fortune in some other industry and choosing to differentiate into real estate.

While this may seem like a distinction without a difference for an operator looking to raise capital, it means two things for these real estate-native family offices. One, they have far more confidence in their specific approach and capabilities than any other investment group. They don't just invest in real estate, they operate real estate assets and bring in-house development and management expertise to the table.

This experience and direct control means that real estate family offices have an easier time bringing portfolios and operating assets into the conversation. If LeFrak or Durst decides to embrace a new technology or operating model, they can simply implement it in their own assets without the hassle of getting their JV partner or operator on board.

Operators should be aware that these groups often like to "do it themselves" rather than partner with third-party operators. Although this isn't a universal rule – these families absolutely partner with outside operators when going outside their market or core expertise – it does mean that they can be competitive threats as easily as they are investors.

(5) Single-Family Offices Without Dedicated Real Estate Teams

Market: A majority of the ~10,000 family offices in the US today

Typical Check Size: $2-10M

Typical Sophistication: Low-to-Moderate

Typical Speed: Low-to-Moderate

Control Required: Low

While some single-family offices have dedicated real estate investors – as we covered in the two prior sections – most of them do not. Many family offices are too small to justify a dedicated real estate investment team; others don't prioritize real estate investing over, say, the public markets, venture capital, or fixed income.

These family offices, of course, still make real estate investments. But they're far less likely to take a leading role in the transaction, more comfortable joining a syndicate or JV alongside another family office or investor they know and trust. And they're more than happy to take a "wait and see" approach to a new model or sponsor, passing on the first, second, and third deals before jumping in once they have a high degree of confidence.

It's important for operators to recognize that these family office investors are looking across a wide variety of deals and categories. On a given day they may evaluate a private equity transaction, a distressed debt opportunity, or an early-stage venture deal being championed by one of the family's kids in addition to whatever real estate opportunities get put in front of them. Rising above the noise is essential.

(6) Ultra High Net Worth Individuals

Market: The 300,000 households in the US with >$20M investable net worth

Typical Check Size: Varies

Typical Sophistication: Low-to-Moderate

Typical Speed: High, mostly

Control Required: Low

There is, of course, a fuzzy line where family offices stop and high-net worth individuals / retail capital begins. Having a “family office” means that dedicated investment staff is helping an individual or family make investment decisions. But nobody intervenes when you hit a certain net worth and insists you stop working with JP Morgan Private Wealth and start hiring your own staff. So in practice there are a lot of really wealthy people who could have a family office but just don’t.

Obviously it's hard to generalize about these individuals. Some can write very large checks on a whim; others will take up lots of your time and ask a ton of questions only to make a $25,000 commitment.

But when they move, they can move quickly and with conviction. Playing to themes of interest – an investment in a given city, a shared work or college experience, a market need – can get them focused on the opportunity. Sophistication, obviously, will vary based on the individual's background, experience, and willingness to commit time to the deal.

—

Real estate operators want to reach family offices. And that makes sense given the state of the institutional capital markets and the advantages of taking family office capital. But "family offices" are not a monolithic category, and understanding the specifics of the group you're talking to is essential in getting a deal done – and not wasting your time barking up the wrong trees. For the full playbook on identifying and approaching each investor type, see our 2026 GP's playbook for finding real estate investors.

—

If you'd like to go deeper, check out our Raising Capital from Family Offices & RIAs workshop.

—

-Brad Hargreaves

World Tree Technologies is using a quick-growing hardwood to compress decades-long timber cycles into an investable real estate timeframe

Meet the 100 people shaping the future of the built world, Part III

Meet the 100 people shaping the future of the built world, Part II

Why the next generation of real estate fund managers will be built on video reels and newsletters

Covering the future of real estate and the people creating it