The Marketplaces of the Future

Predicting six new real estate marketplaces to rise over the next decade

Predicting six new real estate marketplaces to rise over the next decade

Insurance costs are rising across real estate portfolios, and one company is building a new model to manage them

Few line items on a P&L have caused more heartburn over the past ten years than insurance. Long a neglected, set-it-and-forget-it part of property operations, double-digit annual insurance increases beginning in 2019 forced real estate owners to pay attention. According to a 2024 CBRE report, rising insurance premiums since 2019 have cut 3.6% off real estate values nationally and more than 10% in some markets. Suddenly, a traditionally neglected part of the P&L was jeopardizing property performance.

Despite the pain, there has been relatively little innovation in the insurance landscape. Matching large insurers' balance sheets was daunting for any firm, and insurance brokerage remained a largely relationship-based business.

Today's letter digs into the challenges and opportunities reshaping insurance in real estate. We'll do it through the lens of WithCoverage, a new firm from Opendoor co-founder JD Ross taking a fresh approach to the market. We'll also look at non-traditional models, captives and cooperatives, that could fundamentally change the landscape.

After years of soft pricing, the insurance premium shock started in 2019. A run of catastrophic events, including California wildfires, Gulf and Florida hurricanes, and severe storms across the Midwest, burned through reinsurance balance sheets. Reinsurers responded by raising rates and pulling capacity, and carriers passed the costs through to their customers. Catastrophe-exposed markets like Florida and California got hit particularly hard with increases compounding year after year.

By 2023, multifamily owners in coastal Florida were reporting renewal increases of 50% or more on policies that had not had a single claim.

In recent years, compounding insurance rates combined with other macro factors to create a true crisis for real estate operators, landing simultaneously with rising interest rates and wage inflation. Together, these forces compressed debt service coverage and pushed some over-levered deals into distress.

But technological solutions to the insurance problem have largely been absent. Despite the rise of proptech and substantial venture capital flowing into adjacent categories like leasing, payments, and CRM, very few firms have attempted to build for the insurance segment of the P&L.

Two structural barriers make insurance innovation difficult. The first is regulation: writing policies requires state-by-state licensing, capital reserves, and a balance sheet no firm wants to compete against.

The second is the broker model itself.

Conventional insurance brokerage is relationship-based and commission-oriented. While brokers are hired by property owners and managers, they are typically compensated by carriers through commissions on the premium they place, generally between 10% and 15%. The result is a market where the agent technically working for the owner is paid more as premiums go up. That structure is hostile to innovation, as the broker's economic interest is tied to incumbent products and carriers.

The same dynamic extends to alternative risk transfer models such as captives. Self-insurance through a captive insurance company often makes financial sense once a sponsor crosses roughly $2 million in annual premiums, a threshold most multifamily owners hit between 1,500 and 3,000 units. Captives let owners retain underwriting profit they would otherwise hand to carriers, with reinsurance layered on top for catastrophic exposure. But they remain rare in middle-market real estate. Notably, insurance brokers do not earn commissions on captives.

WithCoverage co-founder JD Ross saw this firsthand while building Opendoor, the iBuying platform he co-founded with Eric Wu and Keith Rabois in 2014. The iBuyer model required insuring single-family homes that moved through the portfolio in weeks, not years, on a constantly changing roster of addresses. Standard property carriers could not write the coverage Opendoor needed; their systems could not handle the velocity, and their underwriters could not price the model.

"We had to position it as a portfolio deal, but the portfolio would be changing," says Ross.

Worse, the brokers Opendoor approached were not equipped to design something new. "No insurance broker had the IT or sophistication to do anything other than a commodity story," Ross says. Opendoor eventually went to Lloyd's of London to assemble a custom specialty product directly with the syndicate.

If large-scale iBuyers like Opendoor needed bespoke coverage from Lloyd’s, plenty of other modern real estate models would too.

Years later, Ross teamed up with Max Brenner, co-founder of the investment platform Compound, to start WithCoverage. The pitch runs along two parallel tracks: a technology layer and a compensation model. "We wanted to do for insurance what Brex and Ramp did for finance," Ross says.

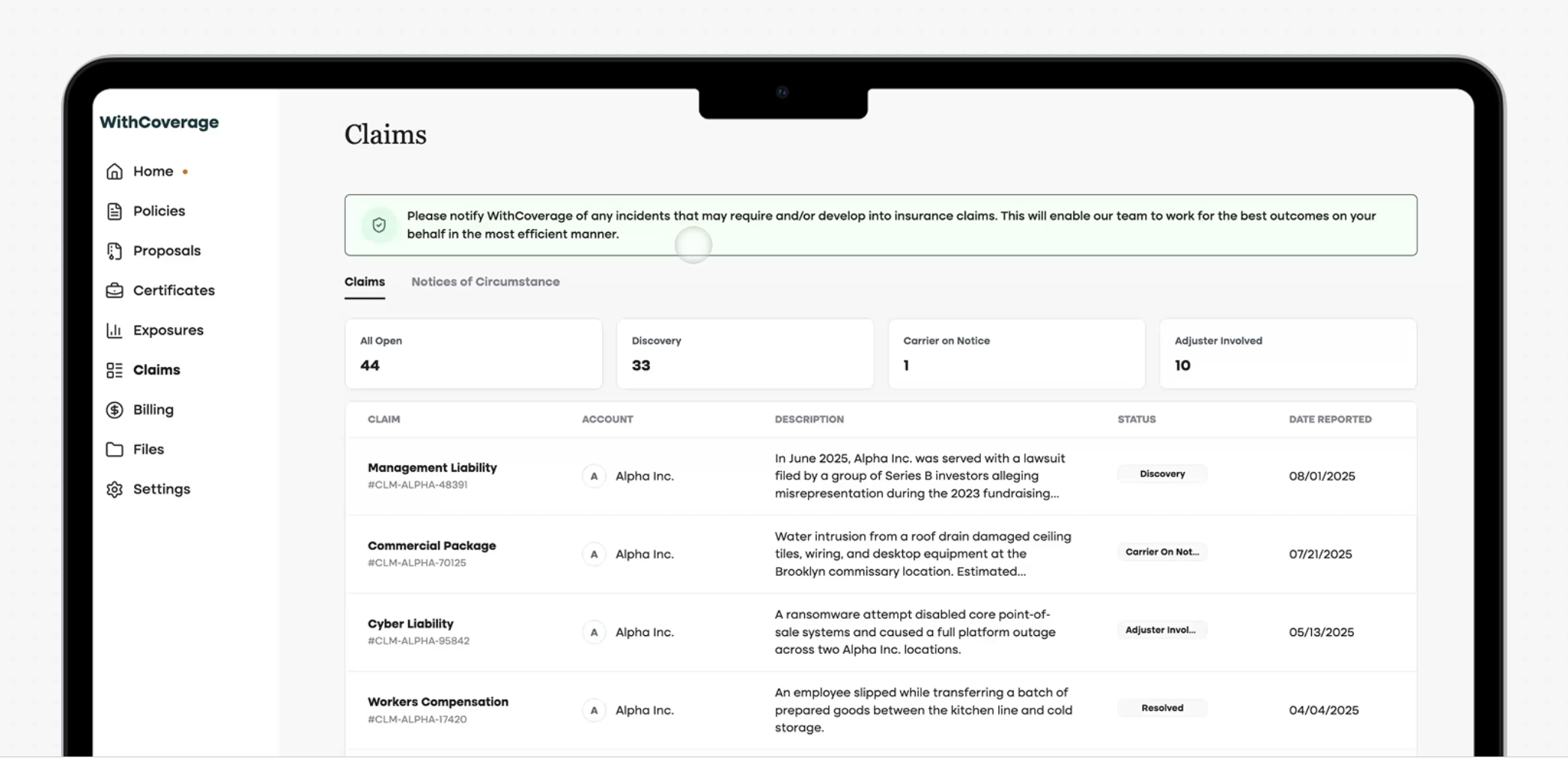

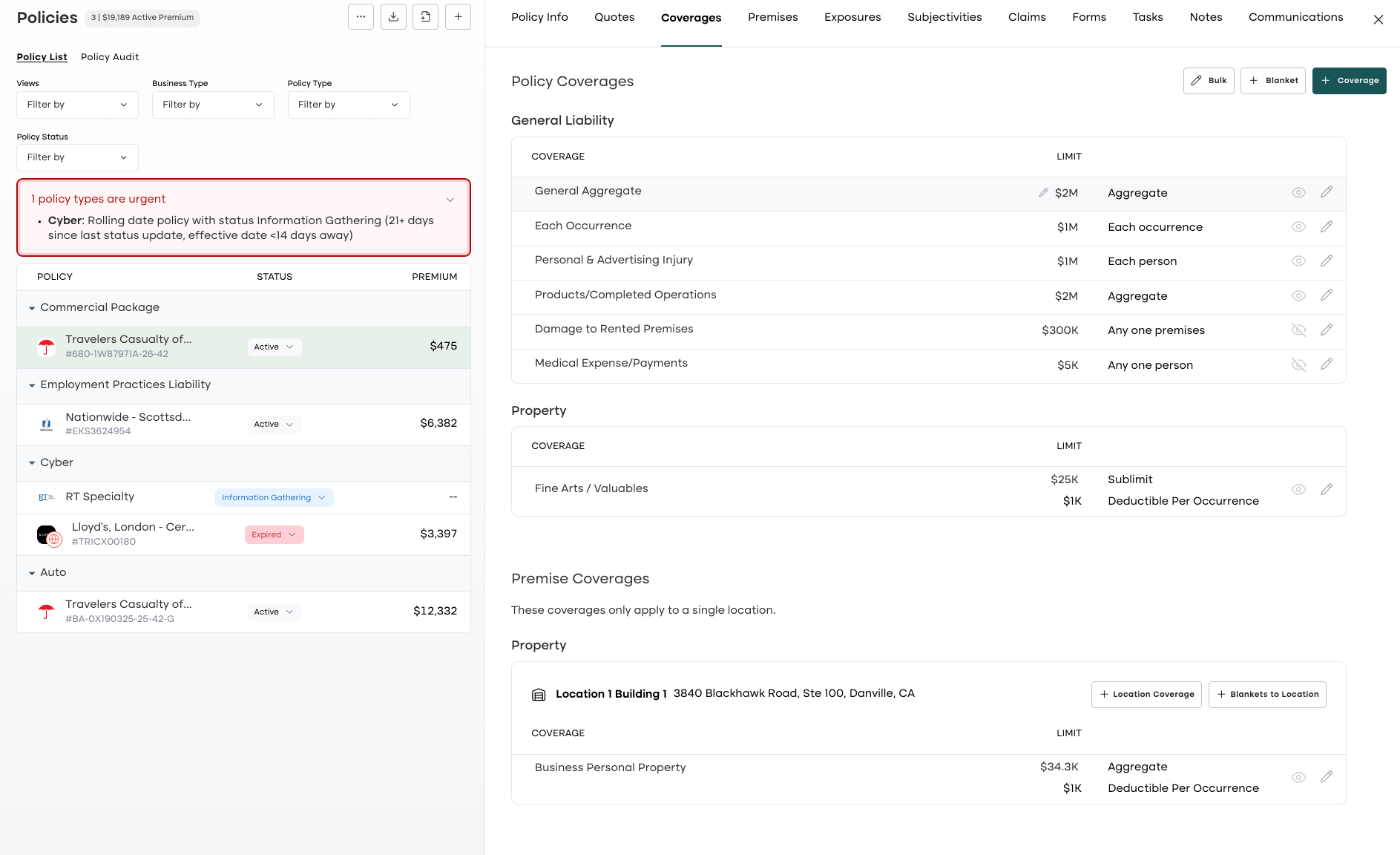

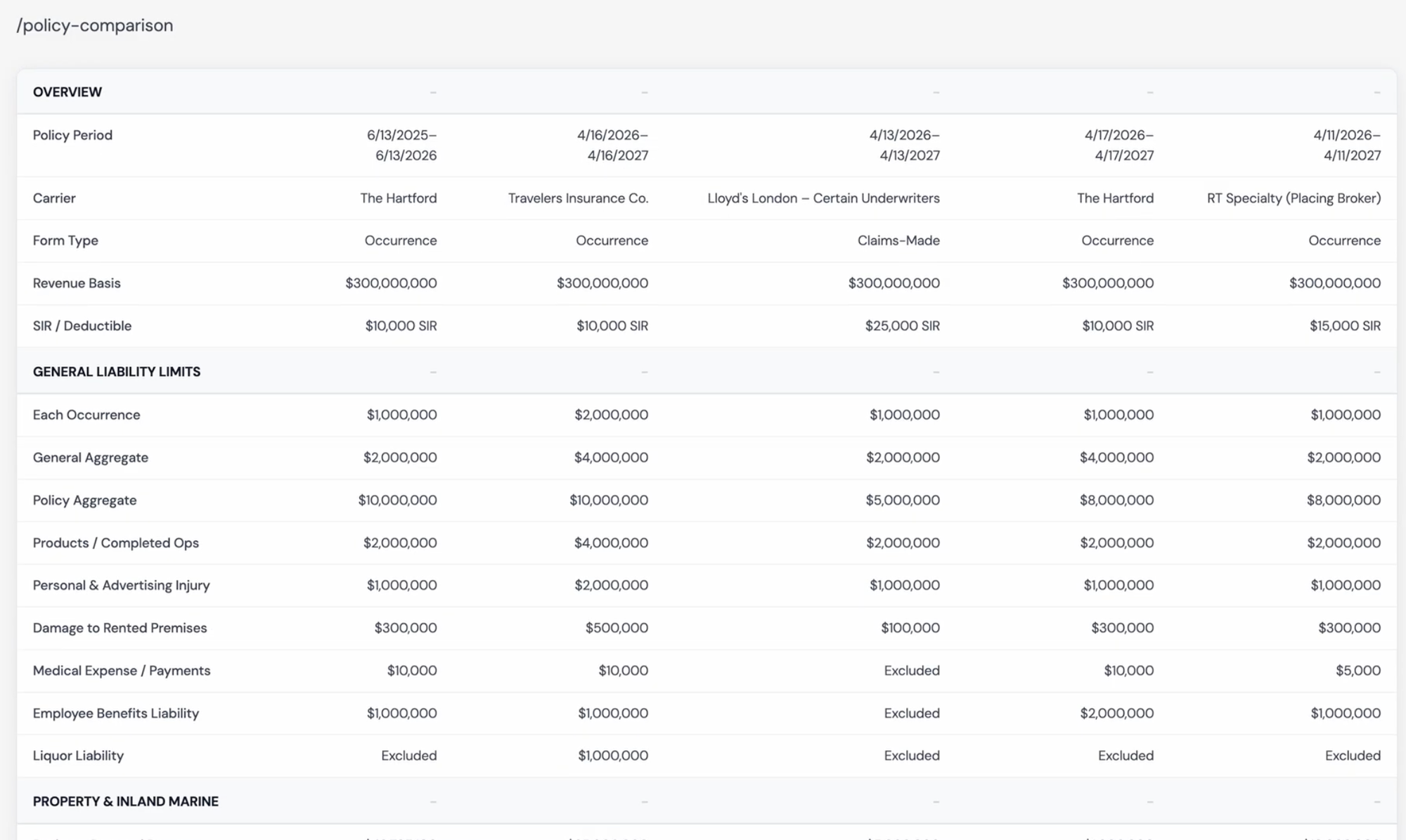

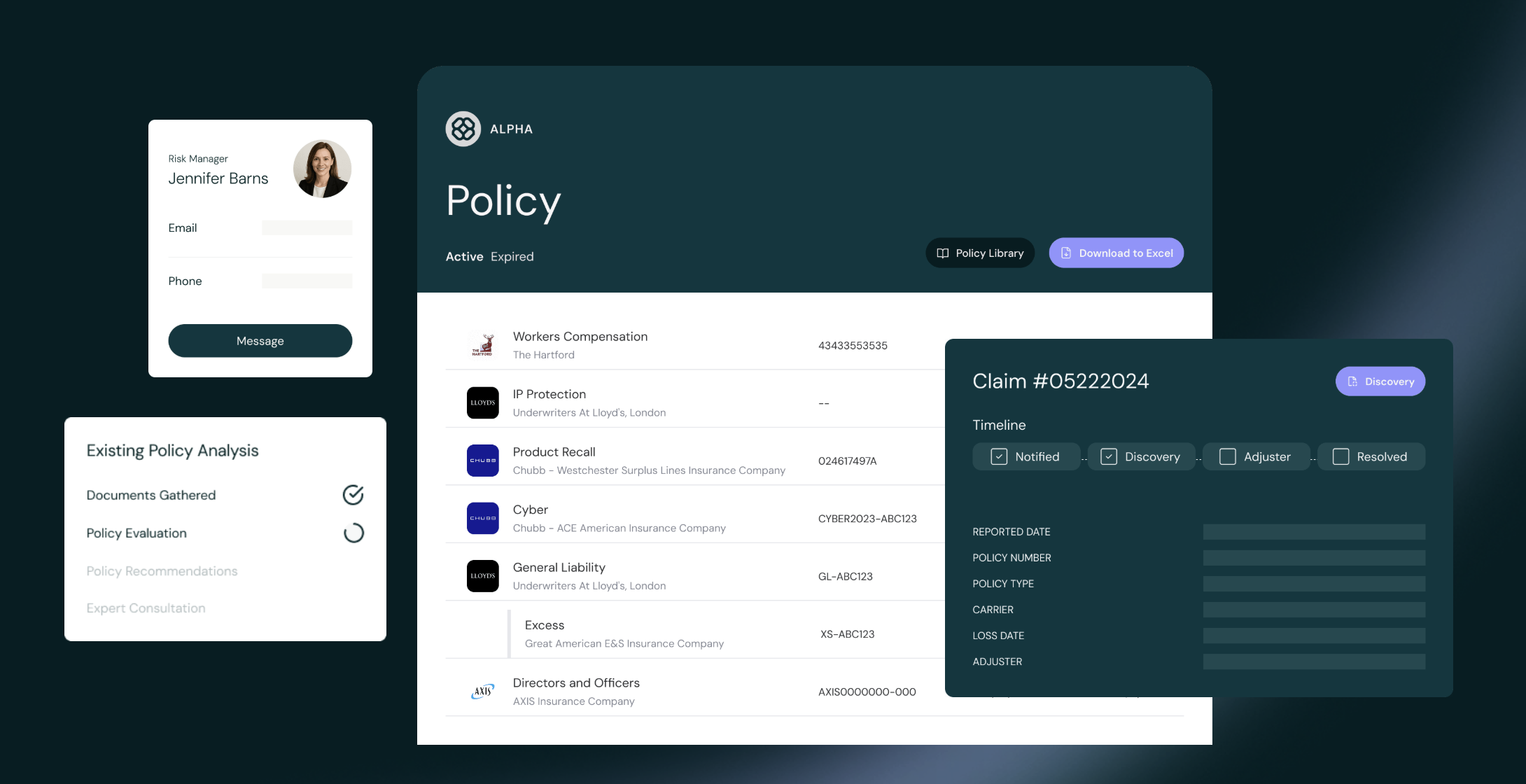

On the technology side, the story is a familiar one in today’s real estate tech landscape: a bet that AI can compress work that has historically been slow and manual. WithCoverage's software ingests policies and parses them for exclusions, endorsements, and gaps. Certificates of insurance, which can take days to procure through a traditional broker, can be generated in minutes. The system cross-checks coverage against lender requirements in real time, flagging where a policy falls short of debt covenant compliance before it becomes a problem at closing.

"We're using software to bring transparency and automation to insurance program management. We verify compliance with lender requirements in real time and take the operating work off the client's plate — our software handles it," Ross adds.

The larger technical advantage is not speed on any single task. It is that the system treats lender review, policy analysis, and certificate issuance as one connected workflow rather than three separate ones. In a traditional brokerage, a change in lender requirements sits in one silo, the underlying policy lives in another, and the certificates issued from it are managed in a third. Gaps between those silos are where compliance failures originate; a lender covenant tightens, the policy never gets updated, and the certificates going out the door no longer reflect actual coverage. WithCoverage's platform closes that loop: a change to any one element automatically reconciles against the other two. The value is not just automation but integrity across the full chain.

The platform also builds bespoke tools in response to specific client needs. One active real estate client had no reliable way to estimate insurance costs on acquisition targets before going under contract. WithCoverage built a tool that delivers replacement cost and rate estimates in real time, giving the client a clearer picture of expected insurance spend before bidding. This is a small example of the broader WithCoverage ethos: the firm treats its client base as a feedback loop for product development, not just a book of business.

He also aims to deploy software to tackle the unglamorous parts of insurance administration that require someone, human or AI, to be knee-deep in policy terms. Properties are routinely overinsured on replacement cost, underinsured on business interruption, and stuck with exclusions that nobody remembers approving. AI-driven policy analysis can surface those issues across an entire portfolio in hours rather than the weeks it would take a human broker to do manually, if that broker did it at all.

But a shift in compensation model is perhaps even more important to delivering value. Where conventional brokers earn commission from carriers, WithCoverage charges a flat fee directly to the client and waives carrier commissions. "We charge a flat fee, put all the carriers on notice, say 'quote this on net zero commission,'" Ross says. The pitch to carriers is that they can sharpen pencils because they are not paying broker comp; the pitch to clients is that the broker's economic interest is no longer tied to the size of their premium.

WithCoverage launched outside real estate, working initially with consumer products, hospitality, and tech companies. Real estate was an obvious adjacency given the size of the pain and the absence of alternatives. The firm expanded into the sector earlier this year.

But the company’s model runs into a specific friction in real estate that does not exist in other industries: the principal-agent gap between owners and fee managers. For a third-party property manager, hiring a traditional broker is effectively free. The broker's commission is buried in the carrier's premium, which gets passed through to the owner. Switching to WithCoverage's flat-fee model means writing a check out of a budget that previously had no line item for it. Even if the owner ultimately saves money on the premium, the fee manager has to advocate for a structure that adds friction to its own operations and creates a new P&L line item that has to be explained and negotiated with the owner during annual budgeting.

Unsurprisingly, WithCoverage isn’t rigid on its commission-free model, reverting to a more conventional structure if requested by its customers. "Half of our clients are on a traditional commission structure, half are not," Ross says. When a client insists on commission, the firm will accept it, preserving the principal-agent dynamic that the model was designed to eliminate. The compromise reflects how hard it is to dislodge an entrenched compensation structure even when the math favors a change.

The larger opportunity in flipping broker incentives is that it opens the door to innovative structures conventional brokerages have little reason to recommend, captives being the most obvious example.

A captive insurance company is a wholly-owned subsidiary set up to insure the risks of its parent. Instead of paying premium to a third-party carrier, the parent capitalizes a captive, retains the underwriting risk on the layers it can afford to bear, and buys reinsurance on top for catastrophic exposure. If losses come in below premium, the parent keeps the underwriting profit. If losses spike, the captive draws on its reserves and the reinsurance layer absorbs the tail.

Captives come in two flavors. Single-parent captives are owned by one sponsor and underwrite only that sponsor's risk. Pooled captives, sometimes called group or cell captives, bring multiple unrelated sponsors together to share risk and spread fixed costs. Single-parent captives historically require enough scale to justify the legal, actuarial, and capital structure overhead. Pooled captives lower the bar.

"At $2 million a year in aggregate premiums you should be looking at a captive," Ross says. "That's where we need to do the actual analysis. You are selling the most profitable layer of risk to someone else. If you can bear some of that risk yourself, you capture that risk back."

The math has held for years. What changes with a model like WithCoverage's is that the broker is paid to design the structure rather than to place premium with a third-party carrier. A traditional broker recommending a captive is recommending a structure that cuts its own commission base substantially, so few do. Setting up a captive is also much more complex than placing a policy, requiring effort that, in more stable, low-cost insurance environments, owners may find unappealing.

But a captive can also become a profit center in its own right. "What's cool about a captive is you can monetize. Bring others in, sell them insurance. Warranties, renters insurance, all sorts of ways you can monetize your captive, turn it into a profit center," Ross says. Renters insurance is the most direct adjacency for multifamily owners; resident warranty programs, parking insurance, and other ancillaries can run through the same vehicle.

Smaller and middle-market owners aren’t completely locked out of the captive model; pooled structures can aggregate portfolios across separate owners. In a pooled captive, multiple unrelated sponsors share the underwriting risk on the layers they can collectively absorb and split the legal, actuarial, and capital overhead that would otherwise make a single-parent captive uneconomic at smaller scale.

The largest operators in any asset class have always had access to balance-sheet advantages the middle market does not; pooled captives can help smaller operators run on more equal footing. "Greystar has a whole risk management team, they have their own insurance products," Ross says. "We will pool up the middle market to allow them to be competitive with the big players."

Whether pooled captives gain real traction in middle-market real estate will depend on how willing operators are to commit to multi-year structures and shared loss exposure with competitors. The Multiple Employer Welfare Arrangements some industries use for health insurance offer a useful, if imperfect, comparison: efficient when the pool is well-curated but fragile when adverse selection creeps in. Trade-association MEWAs (Multiple Employer Welfare Arrangements) in trucking and construction have generally held up when membership is limited to similar-profile employers, while broader open-enrollment versions have a long history of insolvency.

The broader point is that the conditions that kept insurance a quiet, set-it-and-forget-it line item are eroding. Rates have risen far enough to justify the operational effort of finding alternatives. Technology has compressed the cost of running policy comparisons, COI workflows, and compliance checks. Brokers willing to charge flat fees create an opening for structures the commission model never had a reason to push.

Whether WithCoverage specifically becomes the platform that bends the insurance line item, or one of several firms that finally cracks the broker model, the structural change is worth watching. Insurance has been one of the largest sources of NOI compression in multifamily for half a decade. Any improvement — whether through technology or business model shifts — in how the line item gets priced, brokered, or self-insured shows up directly in cap rate math and in deal valuations.

For an industry that has spent seven years absorbing the pain, any innovation is a welcome sight.

–Brad Hargreaves

Predicting six new real estate marketplaces to rise over the next decade

The gap between finding an energy inefficiency and fixing it has cost building owners for over a decade. Agentic AI is the first technology that can close it.

One founder's account of the structural reasons autonomous AI property management SaaS gets crushed, and what the right model actually looks like

Covering the future of real estate and the people creating it