Workshop: Raising Capital from Large LPs

The hard part of raising institutional capital isn't the pitch. It's that a pension allocator, an

The hard part of raising institutional capital isn't the pitch. It's that a pension allocator, an

Predicting six new real estate marketplaces to rise over the next decade

Falling birth rates, shifting migration, and an aging population are already reshaping demand across real estate, faster than most of the market has priced in

Demographics are destiny. And whatever that destiny turns out to be, we're moving toward it faster than almost anyone in real estate has priced in.

Birth rates have been falling sharply since 2008, and America’s total fertility rate (TFR) now sits at 1.55, well below the replacement rate of 2.1 children per woman. Immigration papered over declining fertility for decades, in the United States and across the developed world, but it is no longer the politically viable band-aid it once was. Last year, for the first time in modern history, more people left the US than immigrated to it.

Today's letter walks through real estate's winners and losers over the next decade of demographic change. Some categories are obvious and some are not. Along the way, we'll dig into the mechanics driving the demographic changes that underlie the trends and put a few stubborn myths to rest.

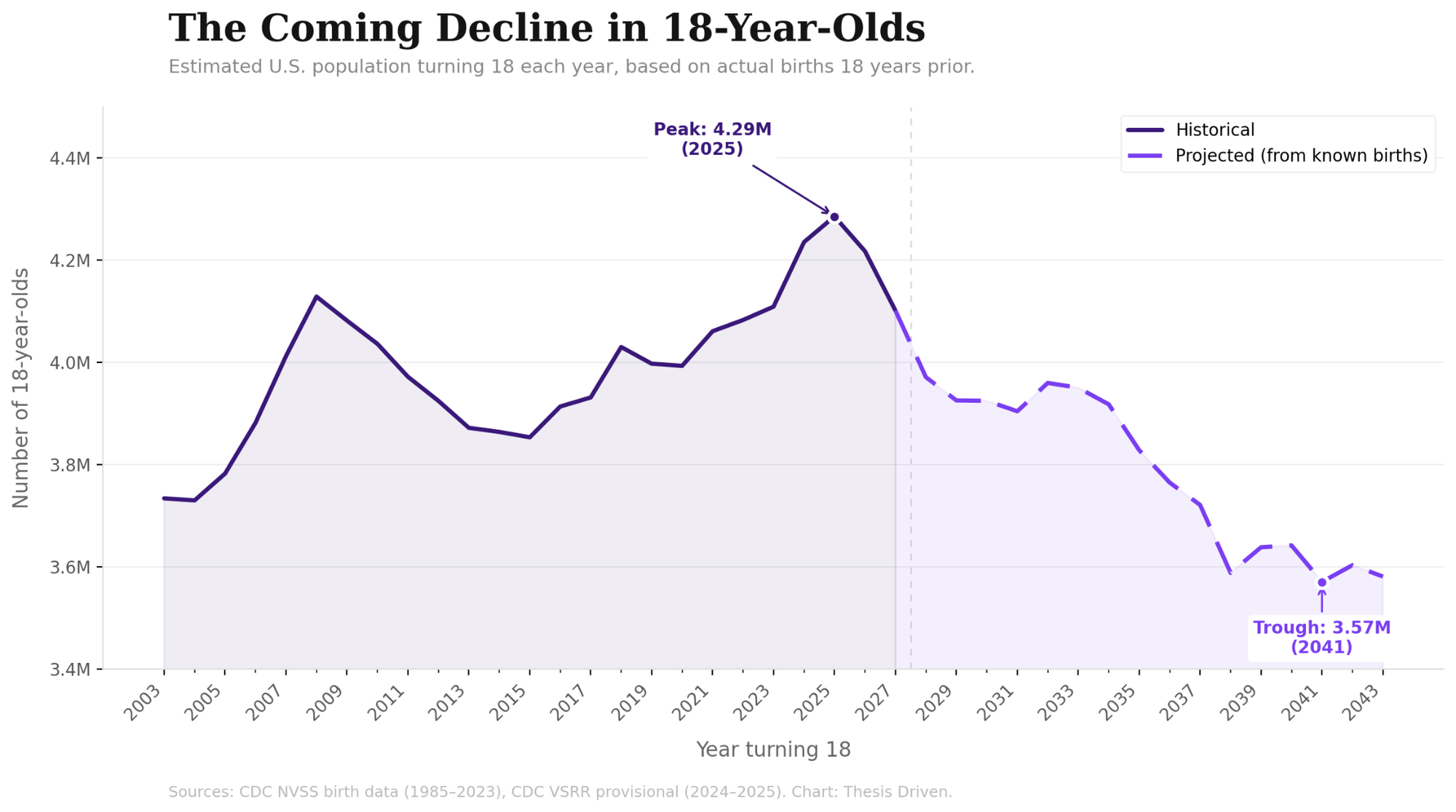

Last year, the US hit "peak 18-year-old." Every cohort of college-age Americans from here forward is smaller than the one before it. Because fertility began its steepest decline after 2009, the cohorts feeding the top of the funnel start shrinking in earnest within the next few years, and they don't stop.

This lands directly on a higher education industry that is already structurally fragile below the top tier. Selective, name-brand universities will be fine; they turn away qualified applicants every year and have a deep bench of demand to draw on. The pressure falls on the schools outside the top 50, the regional publics and tuition-dependent privates that were already running a wave of closures and consolidations before the demographic cliff arrived. A smaller pool of 18-year-olds means those schools compete harder for a shrinking prize.

The enrollment squeeze is also hitting at the exact moment colleges can no longer lean on international students to fill the gap. International enrollment fell 17% year over year in fall 2025, removing the marginal demand that propped up enrollment at hundreds of mid-tier institutions through the 2010s.

There’s a direct translation to real estate. Demand for purpose-built student housing will soften, and it will soften the most at the bottom of the quality spectrum. Class B and C product in secondary college towns, the older garden-style and converted stock that only ever penciled because student demand kept growing, is the most exposed. When the beds stop filling, there is no clever repositioning that conjures students who were never born.

Let’s get one myth out of the way: declining fertility, even below-replacement fertility, does not mean a declining population.

Demographic inertia is a powerful thing. The US population will keep growing for decades even as Americans have fewer kids, because older people are staying alive longer and the large cohorts are still decades away from their actuarial cliffs. While the eventual decline is locked in, it isn’t going to show up immediately in high-level population numbers.

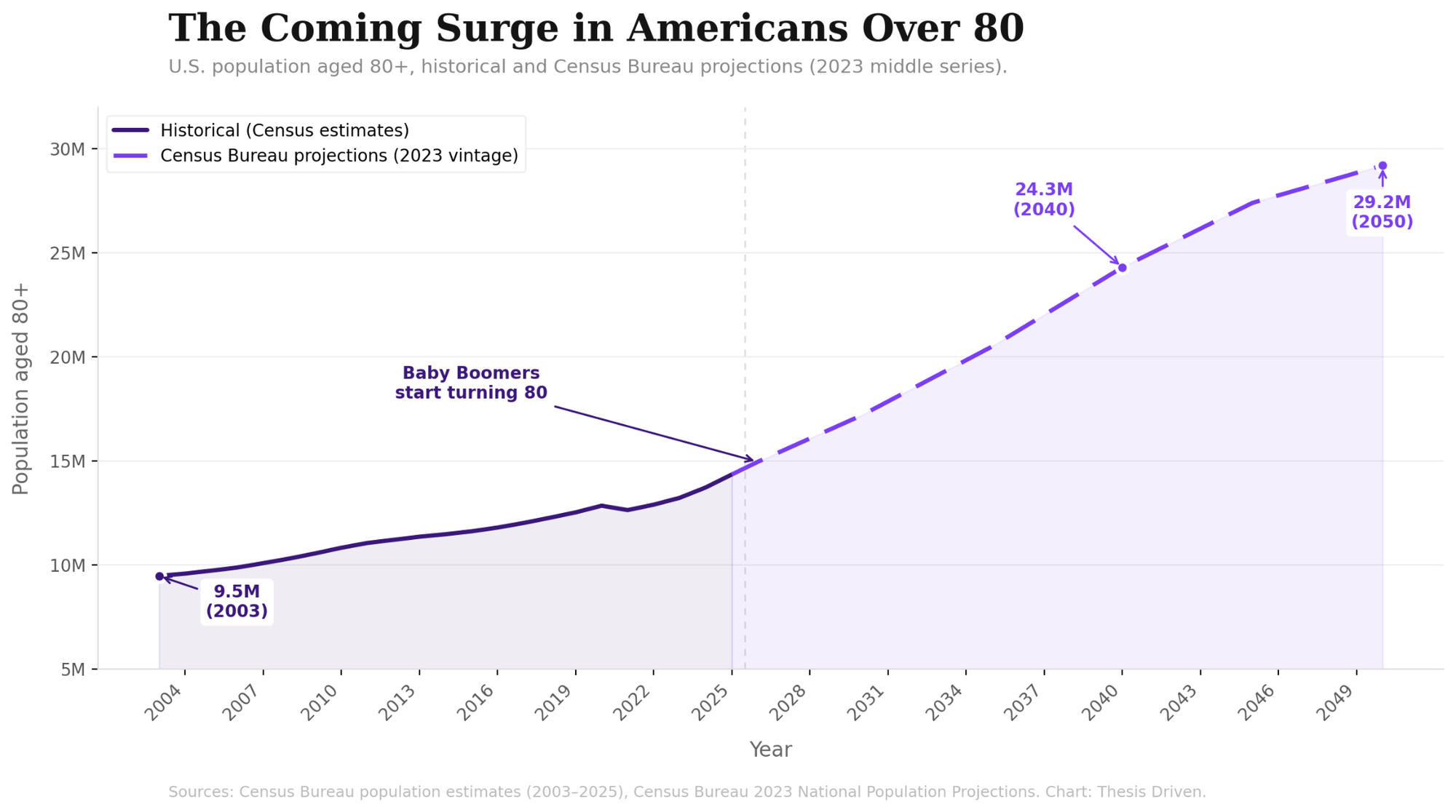

So while the young population shrinks, the senior population grows, and it grows for a long time. The first wave of that demand falls on 55+ and active adult communities, the lifestyle-oriented product for healthy, independent, self-funded boomers, and increasing numbers of Gen Xers, who want amenities and community without a care component. That cohort is enormous, it controls an outsized share of national household wealth, and it is only beginning to move.

Memory care, however, will be the standout performer. In percentage terms, the single fastest-growing age band over the coming decades is the 90-plus population, as medicine keeps finding ways to extend life. The catch is that extending life and managing aging are not the same problem; our ability to cure or suppress specific diseases has run well ahead of our ability to manage cognitive decline. People are living longer, and a growing share of those extra years will require supportive, supervised care. Demand for memory care is not a cyclical bet; it is baked into the actuarial tables.

There may even be an elegant bit of symmetry here. Some of the struggling colleges and emptying student-housing assets sit in pleasant, walkable, amenity-rich college towns. A subset of active adults want exactly that: a campus environment, cultural programming, lifelong learning, a town built around 18-year-olds that suddenly has room. The operator who figures out how to convert a half-empty college town into a destination for engaged retirees may be solving two demographic problems at once.

Immigration was quietly holding a lot of small towns together. Many of these places have dismal fertility and even worse raw birth numbers, not because of cultural choices but because they were already short on people of prime childbearing age. The young adults left for metros years ago, and inbound international migration kept the lights on.

The stories of small towns revitalized by immigrants are real. But the causation runs the other way from how it's usually told. Those towns didn't attract immigrants because they were thriving. They attracted immigrants because they had been depopulated and were cheap, and the immigrants were the thing keeping them alive working jobs with wages that native-born Americans didn’t want — think meatpacking plants in Nebraska. Without the immigration filling those vacancies, many small towns will enter terminal decline.

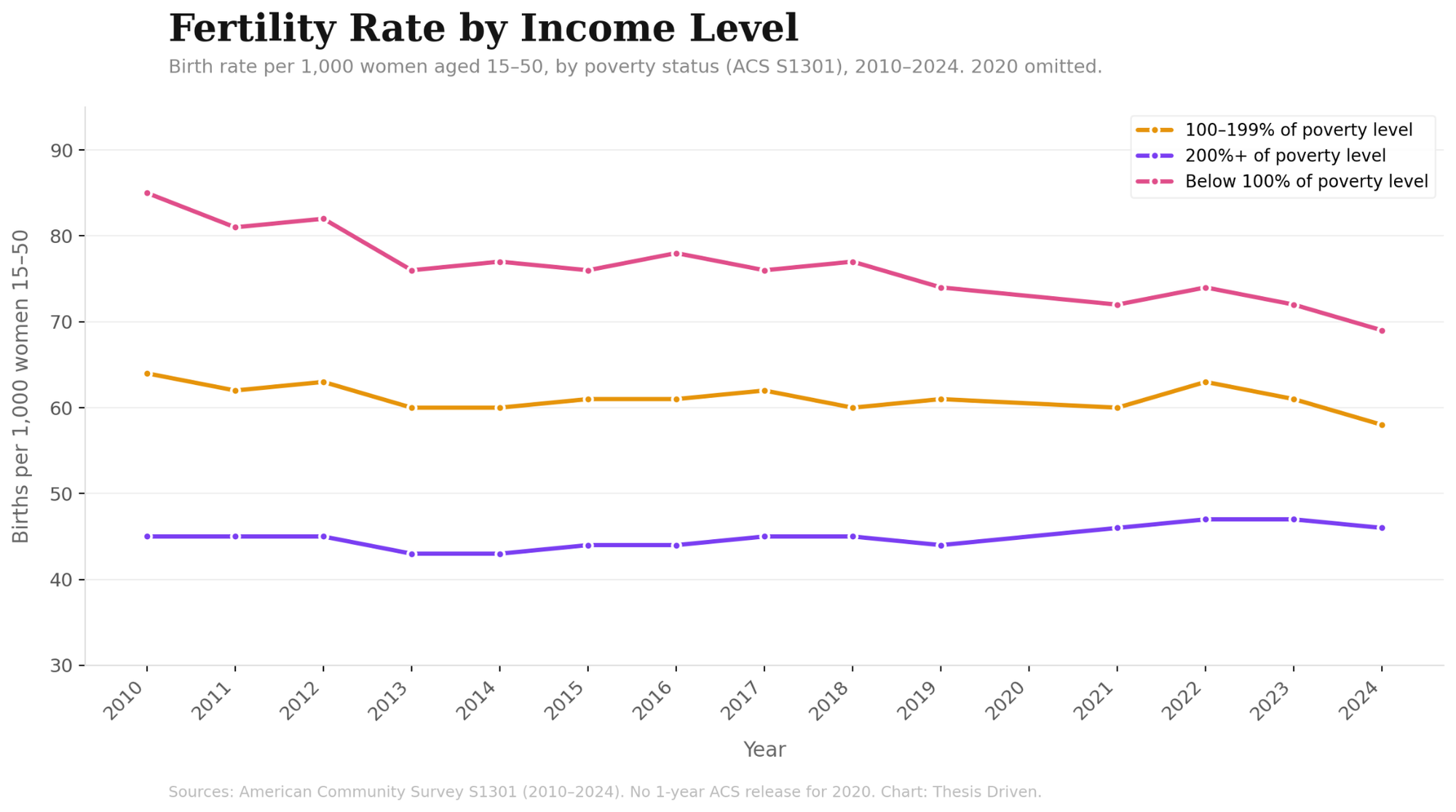

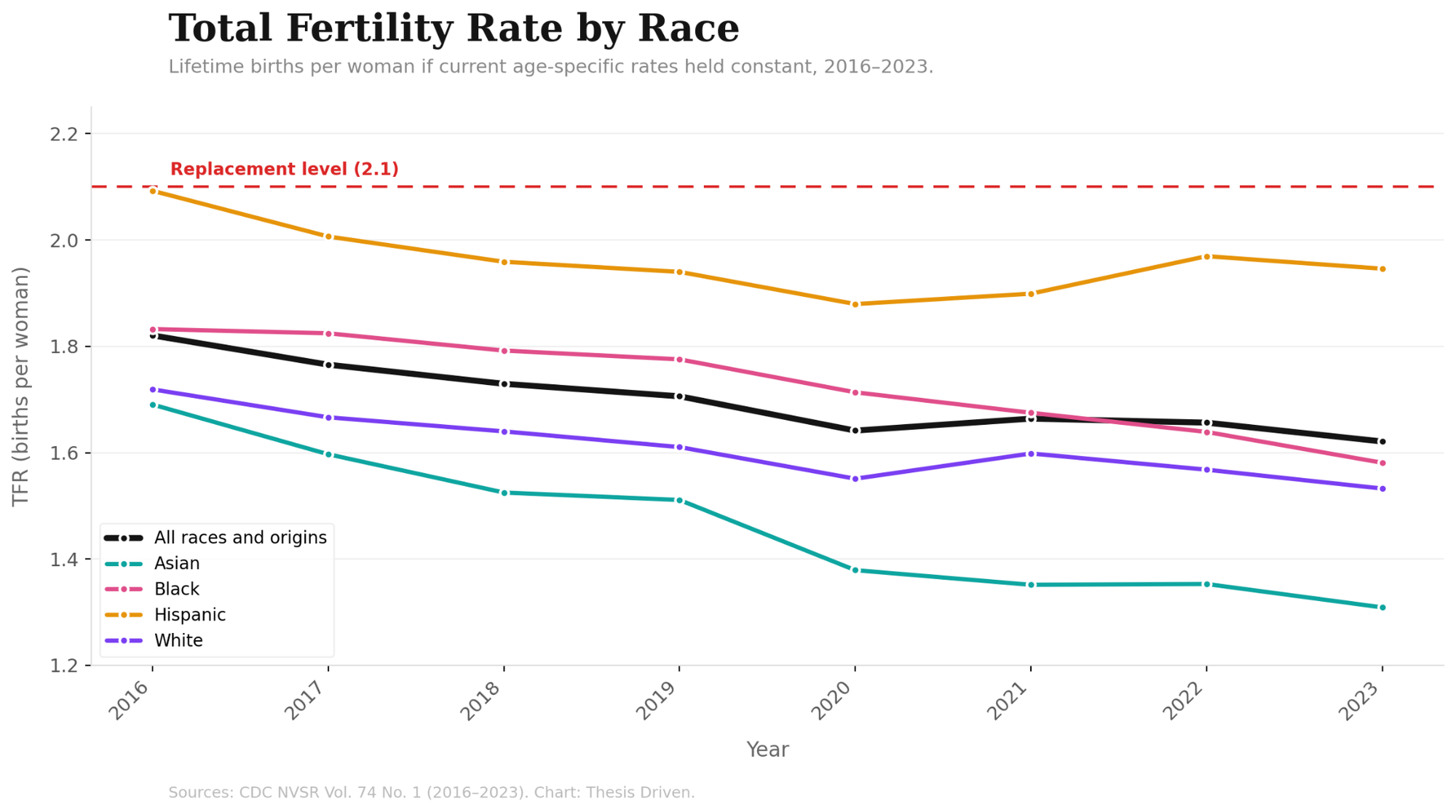

It’s also worth noting that recent fertility declines have been steepest among lower-income Americans, driven in large part by a collapse in teen pregnancy that, whatever else one thinks about it, removed a meaningful chunk of total births. Fertility among wealthier Americans has actually risen slightly over the past fifteen years. The decline is differentiated along racial lines too. Black fertility has now fallen below white fertility for the first time in US history.

Each passing year delivers a smaller cohort of young adults reaching first-time-homebuyer age. That alone would pressure entry-level homebuilding. What makes it acute is the timing: the demand-side shrinkage arrives just as the largest cohorts in American history begin downsizing and passing homes along to their children.

The result is a squeeze from both ends. Demand for the tiny, yardless, far-flung exurban starter home thins out at the same moment the resale market fills with Luxury Boomer Boxes: larger, nicer, better-located homes hitting the market through downsizing and inheritance. The entry-level builder's customer is disappearing while the inventory competing with that builder is expanding.

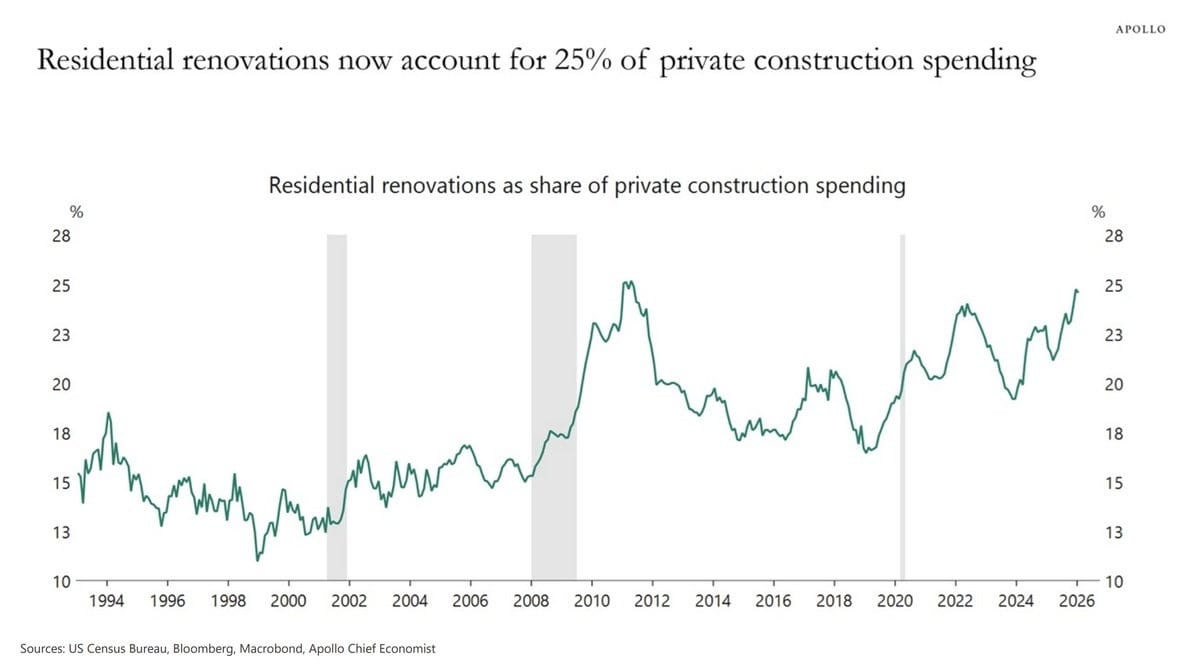

Renovation is already a large and growing share of total US construction spending, and the demographic and rate environment only accelerates it. The drivers are unglamorous and durable: The housing stock is aging and needs work, and higher rates have locked millions of owners into homes they have no intention of selling. This turns deferred maintenance and "we'll fix it when we move" into "we live here now, let's renovate."

Add the aging-in-place wave to that. A growing population of older homeowners would rather modify the home they own than move into managed care, which means accessibility retrofits, single-floor reconfigurations, and quality-of-life upgrades on top of ordinary repair demand. Renovation captures the spending that new construction loses when household formation slows.

And when all those boomer homes do pass down to their inheritors — or hit the market — some renovation is inevitable to bring them in line with Millennials’ very different design aesthetics and layout expectations. Goodbye formal dining room, hello flex office and mudroom.

The most misread statistic in American urbanism is net domestic migration, and the misreading has convinced a lot of smart people that big cities are dying. They aren't. As we laid out previously, big cities that pull in large numbers of young people will almost always post negative net domestic migration. That is a feature of how they work, not evidence of decline.

The mechanism is simple once it's spelled out: Two people move to New York in their twenties, meet, marry, have a kid, and decamp for the suburbs. That's a household of three leaving where two individuals arrived: -1 net domestic migration generated by a city doing exactly what cities do: attract young people who meet, get married, and have kids.

Cities should absolutely build more housing to keep more of those people longer, but retaining all of them would require population growth unprecedented in modern urbanism. Historically, big cities grew despite negative domestic migration, carried by high birth rates (raw births, not the fertility rate) and international migration.

The variable here is housing costs. High rents push families out sooner, which drives net domestic migration more negative and caps growth. Zoning is an artificial constraint, but it sets off a feedback loop with real consequences: constrain supply, push rents up, accelerate the family exodus. Let rents fall and the loop runs in reverse. Families stay longer, households persist, and the city stabilizes.

Expensive metros hold an advantage that cheaper places don't. In a low-rent market, there is no floor. Depopulation means vacancy, and in some submarkets there is simply no rent at which anyone will take the unit. Expensive cities have room to fall before they hit that wall, and falling makes them more attractive, not less. A pricey, supply-constrained metro that gets 15% cheaper becomes a magnet again. Cheap, hollowed-out markets lack that corrective feedback loop.

A shrinking labor force is a tailwind for anything that replaces labor. Fewer workers, particularly fewer working-age people, means more opportunity and more pressure to automate. What reads as a pilot project or a nice-to-have experiment today becomes a hard operational necessity tomorrow as a contracting workforce compounds the existing skilled-trades shortages.

As labor costs get bid up by scarcity, automation and robotics that don't pencil today, blocked by high upfront costs and low utilization, suddenly clear the hurdle. A brick-laying or pile-driving robot that’s a bad investment at $25-an-hour labor becomes a great one at $45.

Immigration remains the wildcard. A future administration that meaningfully reopens skilled immigration would ease labor scarcity and slow the automation imperative at the margin. Absent that, the pressure to automate the physical economy only intensifies.

With fewer people, and fewer working-age people in particular, housing quality filters upward. Renters who couldn't previously afford a given tier of apartment suddenly can, because the competition for those units has thinned. The impact lands squarely on Class B and C product, especially in tertiary markets that lack the demand depth to backfill.

The narrative rhymes with what happens in low-cost cities. Is there a market-clearing price at all, or do some units simply sit empty? In the weakest submarkets, it is possible that no rent clears the unit, and the asset goes dark.

But there’s a complicating statistical question buried in here: As rents fall, do new households form? Specifically, I’m watching "hidden households," people doubled up with parents or packed in with roommates who would split off into their own (mostly single-person) units as prices come down. That latent demand could absorb a meaningful share of softening supply.

The definitions themselves are slippery, which is part of why this is so hard to forecast. The number of households and the number of housing units are mechanically linked, since a household is defined in terms of occupying a housing unit. Some housing experts argue there is no housing shortage by pointing to the tight correlation between units and households. But that correlation is partly an artifact of the definition: a household exists because a unit exists to contain it, which makes the argument circular. How much pent-up household formation is waiting in the wings is one of the most important unanswered questions in housing, and it determines how far Class B and C rents have to fall.

The math of population decline is straightforward and unforgiving. Fewer young, working people will be supporting more retirees drawing pensions and Social Security. The dependency ratio deteriorates everywhere, but it hits harder in some places than others.

States and cities that already carry heavy unfunded pension liabilities, that lean on a narrow base of working-age taxpayers, and that have been losing those taxpayers to migration are staring at a vise. The obligations are fixed and rising, while the tax base funding them is shrinking and aging. The standard responses (raising taxes, cutting services) both make the jurisdiction less attractive, which accelerates the outflow that created the problem. Today’s fiscally questionable states like California and Pennsylvania will struggle, while states already in fiscal trouble (New Jersey, Illinois) will face severe fiscal stress.

It is the municipal version of the no-floor dynamic playing out in depopulating housing markets: once the spiral starts, there is no obvious price at which it self-corrects.

For real estate, fiscal fragility is not an abstraction. It shows up as deteriorating services, rising property and transfer taxes, and eventually distressed infrastructure in exactly the markets that can least afford to deter residents and capital.

–

The thread running through all of this is the same one running through the fertility data: the future is already determined for a long way out, and most of the market is still underwriting the past. The winners over the next decade won't be the players who guessed where demographics are heading. They'll be the ones who noticed we're already there.

-Brad Hargreaves

How a generation of superstar chefs and obsessed diners remade urban neighborhoods, inflated rents, and priced themselves out of the streets they made desirable.

How autonomous vehicles will break the economics of convenience retail

Stacks of documents, repetitive workflows, and massive economics make mortgage lending an obvious target for AI, but adoption has been slow.

When ultra-exclusive resort towns like Jackson Hole and Aspen run out of space and affordability, demand moves down the road

Covering the future of real estate and the people creating it