Deep Dive: Drake Real Estate Partners

Drake targets $5-20M equity in industrial outdoor storage and manufactured housing. The model, the returns, and why the overlooked niches keep delivering.

Don’t miss Thesis Driven’s Buy Box deep dive on Drake next Wednesday, September 24. Register here (for accredited & institutional investors only).

At Thesis Driven, we love niches. We’ve written before about why the best opportunities in real estate often live in corners too small, too messy, or too operationally complex for the largest pools of capital.

Asset classes like industrial outdoor storage, manufactured housing, marinas and student housing all demand hands-on execution—whether it’s rolling up fragmented owners, improving community infrastructure, or managing an operating business within the four walls of the real estate. And for those willing to do the work, the payoff is higher and more durable yields.

We typically highlight the operators and developers bringing those niche strategies to life. But behind the most successful operators are strategic investors willing to underwrite the risk and structure capital to scale. Today, we’re focusing on one of those investors: Drake Real Estate Partners.

Drake is led by co-founders David Cotterman and Nicolas Ibáñez, who were introduced in 2012 by a mutual Harvard Business School professor. In 2016 they brought in partner Jonathan Garonce, and together, they built a top-tier private equity shop with the entrepreneurial spirit of a family-backed platform, creating a franchise around market inefficiencies.

Today, they target ~$5-20 million equity checks in opportunities sourced alongside property type specific, geographic specific “sharp shooter” operators, generally in secondary and emerging markets, and property types like industrial outdoor storage and manufactured housing that institutions often overlook.

The result is a differentiated model that’s delivered net realized returns of +20% IRR and 1.9X equity multiple across more than a decade of investing.

In this letter, we’ll break down:

- Drake’s niche investment model,

- Their thematic playbooks,

- The team and platform,

- How Drake works with operators (and what operators should know about them), and

- A few illustrative deals that show the Drake playbook in action

Drake’s niche investment model

Drake has carved out a niche by focusing on the part of the market that larger managers can’t reach efficiently.

Their sweet spot is equity checks in the $5-20 million range (but can go even smaller than $5 million if the asset is part of a roll-up strategy), translating to total deal sizes of $10-90 million. That’s the territory where institutions struggle to deploy at scale but where entrepreneurial operators and family-backed sellers are still active, translating to less competition, more favorable entry pricing, and the potential for outsized risk-adjusted returns.

“We look for inefficient buy dynamics,” David Cotterman, Co-Founder and CIO of Drake Real Estate Partners, says. “Distress, mis-marketed assets, estate and family transition assets are what we like to find. We always like to buy below replacement cost, have a deep value-based philosophy, and favor assets with strong in-place cash flow.”

“That cash flow is critical; it means our returns don’t depend as much asset appreciation, and we always underwrite our exit caps conservatively relative to spot cap rates today. We’re typically generating cash-on-cash yields from day one, which gives us real downside protection in uncertain markets.”

Examples of strategies include rolling up small industrial assets into institutional-quality portfolios, buying and upgrading manufactured housing communities, and building an income-producing industrial outdoor storage portfolio. In every case, the emphasis is on adding value through hands-on execution rather than waiting for the market to bail them out.

Key features of Drake’s investment model:

- Target deal size: $5–20M equity checks in non-major markets where institutional capital is scarce

- Inefficient sourcing: Off-market and mis-marketed opportunities

- Cash flow focus: Preference for assets with strong interim cash yields, limiting reliance on exit cap rates

- Value-add execution: Operational improvements, repositioning, and tenancy fixes that grow NOI

- Operating partner leverage: “Sharp shooter” local operators provide market knowledge and execution capacity

- Alignment: Significant GP and team capital invested alongside LPs, with performance-driven compensation

“Our operating partners are an extension of our team,” says Jonathan Garonce, Partner and Head of Asset Management. “They bring deep local expertise—whether it’s a property type, a market, or even a specific sub-sector. Many are vertically integrated, which means they can handle the day-to-day execution of our business plans.”

“Our role is to underwrite independently, collaborate on the business plan, and then stay shoulder-to-shoulder from acquisition through exit.”

The approach gives Drake the flexibility to move into niches that demand local knowledge, from marinas to student housing to infill industrial. Drake can pivot nimbly between these, and others, thanks to this partnership model.

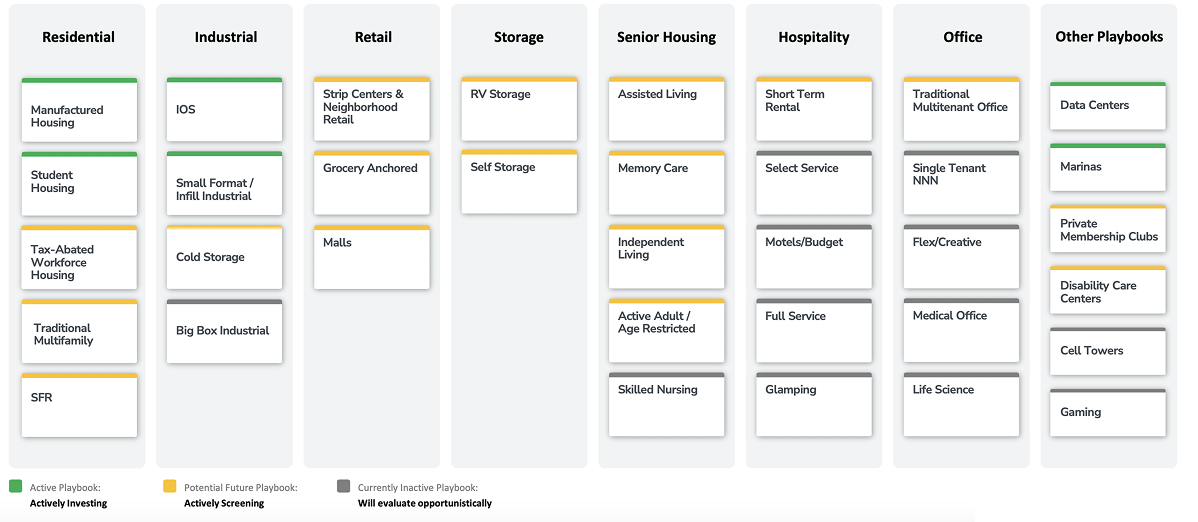

Drake’s Thematic Playbooks

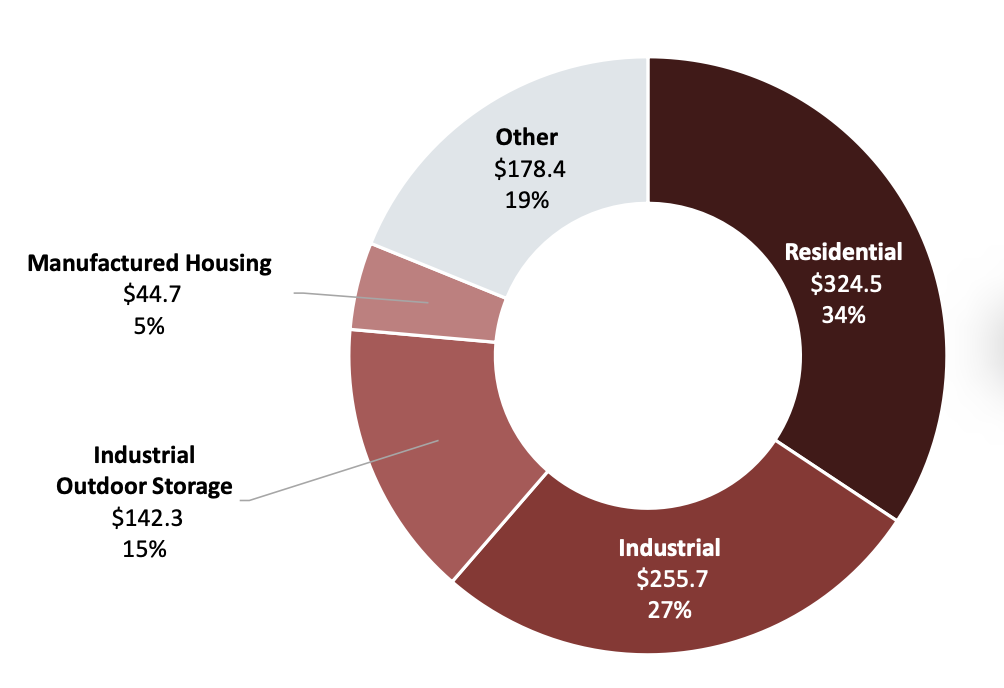

While Drake has flexibility across property types, most of its capital has been concentrated in a handful of themes that reflect long-term supply-demand imbalances. About 80% of Drake’s equity invested since inception has been deployed in residential, industrial, industrial outdoor storage, and manufactured housing.

The common thread is operational complexity paired with secular demand tailwinds—settings where entrepreneurial operators can add real value.

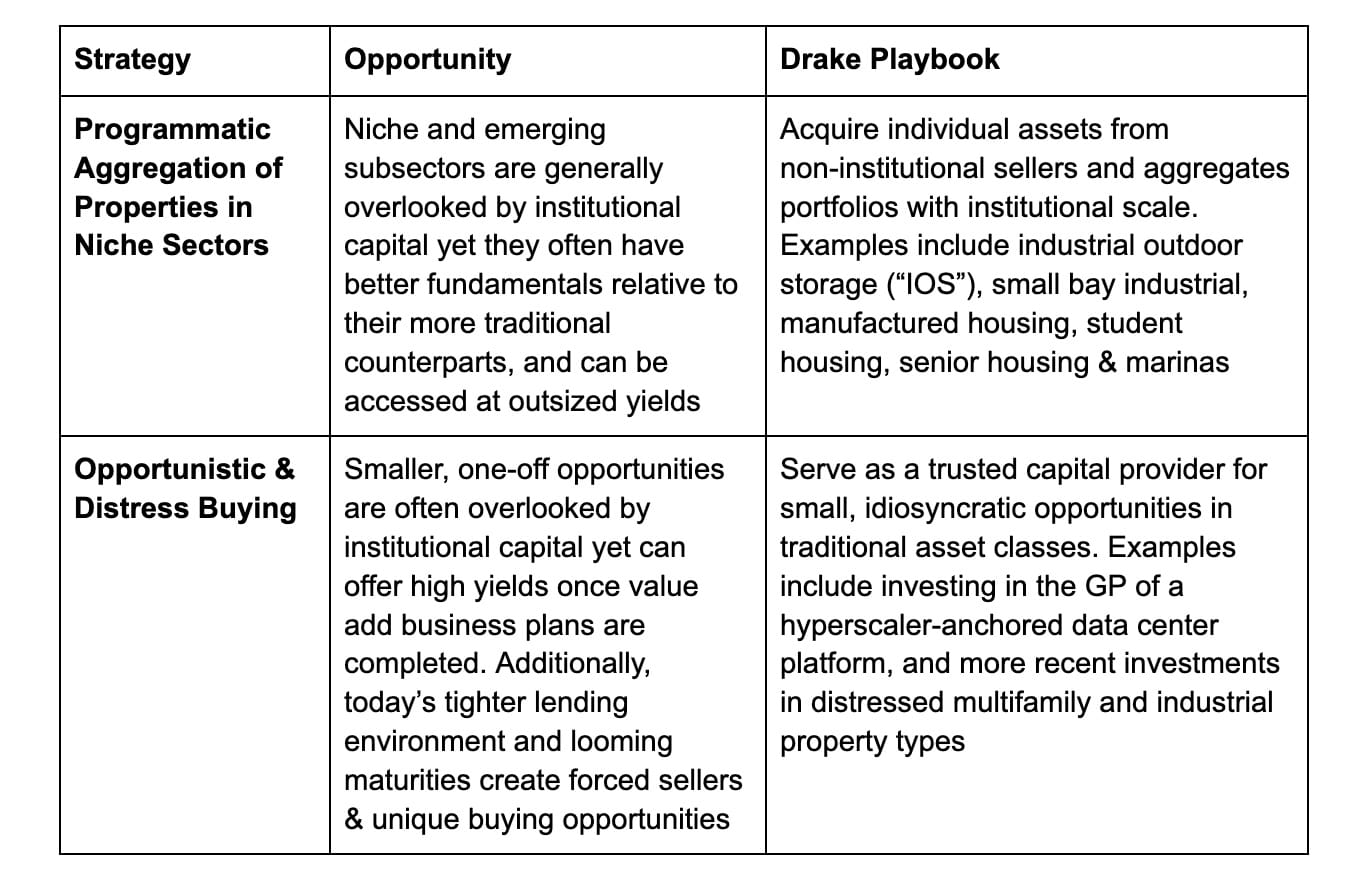

Drake currently employs two primary strategies:

The Team Behind Drake

Drake is built around three partners who approach real estate from different but complementary angles—one from the institutional world (David), one from a family office (Nicolas), and one from the ground-up execution side (Jonathan).

The firm was started when David Cotterman and Nicolas Ibáñez were introduced by Arthur Segal, founder of TA Realty and a real estate professor they both studied under at Harvard Business School. David had previously been a principal in the real estate group at MSD Capital, Michael Dell’s family office, where he put more than a billion dollars to work across property types after beginning his career in development at Urban Partners. Nicolas had been building the real assets arm of his family’s firm, Drake Enterprises, which today manages more than $1.4 billion, giving him a long-term, family office perspective on capital and culture.

In 2016, they brought in Jonathan Garonce, who had been running principal real estate investments at a family office after his time in Merrill Lynch’s private equity real estate group. Jon became the execution partner—working closely with and overseeing the firm’s operator partner relationships.

The team is 20 strong across acquisitions, asset management, finance, and IR, with 58% female or minority representation.

“We’ve always believed alignment has to be real,” says Nicolas Ibáñez, Co-Founder and President of Drake. “Our team and families invest meaningful capital in every fund, and our compensation only works if the investments perform.”

“We take the same approach with operators—most of our partnerships are programmatic, with co-investment and shared hurdles so everyone is pulling in the same direction. That creates a culture that’s flat and collaborative, where decisions get made quickly and the same people stay involved from acquisition through exit.”

This level of continuity is unusual in private equity real estate, where responsibilities are often handed down to junior staff (many operators describe the frustration of negotiating a joint venture with senior partners, only to find themselves reporting day-to-day to a 26-year-old analyst).

How Drake Works with Operators

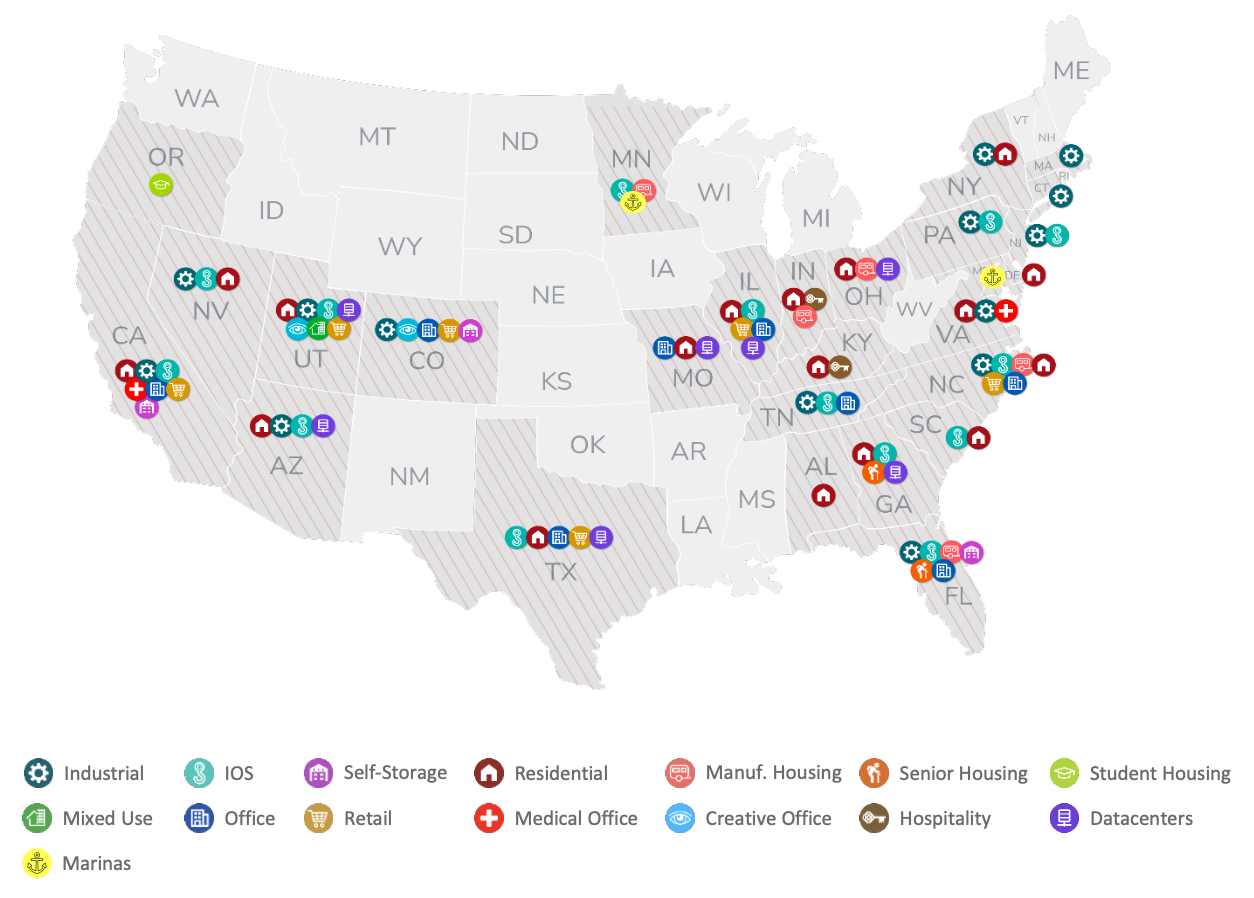

For Drake, the operating partner isn’t just a vehicle for execution—it’s the core of the model. Nearly all of the firm’s 180-plus acquisitions have come through its network of local operators, and more than 90% of those have been repeat partnerships.

The profile of these partners is consistent. They are usually smaller, entrepreneurial groups with deep local knowledge, a niche focus, and proven track records (oftentimes generating consistent unlevered yields north of 8%). Most are vertically integrated, i.e., they handle their own property management, leasing, and capital projects. That integration gives them speed and control, while Drake provides an institutional lens around asset management, capital, financing, and reporting.

What operators should know about working with Drake:

- Repeat relationships: 90%+ of deals are with repeat partners—Drake looks for long-term programmatic ventures, not one-offs

- Niche focus: Strong preference for operators with deep expertise in a specific property type or geography

- Vertical integration: Many of Drake’s best partners control their own management and operations, which allows for efficiency and execution speed

- Shared discipline: Drake independently underwrites every deal and stays involved from acquisition through exit, bringing institutional process to budgets, financing, and reporting

- Skin in the game: Co-investment and shared performance hurdles ensure alignment between fund and operator.

This approach plays to each side’s strengths. Operators identify opportunities and run the day-to-day. Drake brings capital, structure, and continuity as the same people who greenlight a deal are still in the room when it’s time to lease, refinance, or sell.

For operators, the value is clear: Drake can help turn local expertise into scale, bundling smaller assets into institutional portfolios and providing the capital and governance needed to grow. But the expectation is clear too—alignment must be real, and execution has to be repeatable.

Illustrative deals

The best way to understand Drake’s model is through the types of projects it’s executed across sectors, identifying inefficient entry points and bringing institutional expertise to sub-institutional projects.

Miami Truck Parking (Industrial Outdoor Storage) ~ Miami, FL

This project illustrates Drake’s original thesis in IOS: upgrading underutilized land into income-generating infrastructure tied to logistics demand.

- Acquired an off-market 12-acre site in Feb 2019

- Upgraded with resurfacing, fencing, lighting, security, and new on-site showers/bathrooms

- Master leased to Lanier Parking Systems for $2.3mm/year

- Sold in April 2022 generated a 44% gross IRR and a 2.8x gross equity multiple

Greensboro Industrial ~ Greensboro, NC

This is an example of buying “smart” into a complex situation, below replacement cost, and creating value through lease restructuring.

- Acquired in March 2019 from a liquidating trustee acting on behalf of a fractured ownership syndicate. Further complicating the transaction, the asset’s tenant was a subsidiary of Sears, who was in bankruptcy at the time.

- The asset is a 1.5 million SF industrial warehouse leased to Kmart and subleased to NFI Industries, for $45mm ($29/SF)

- Restructured lease into a direct deal with NFI, requiring the tenant to invest in the space

- Sold in March 2021 generated a 70% gross IRR and a 2.6x gross equity multiple

Colton Multifamily ~ Inland Empire, CA

A large-scale multifamily repositioning that shows Drake’s ability to enhance value through targeted renovations and improved tenant experience.

- Acquired in October 2019, a 366-unit multifamily property

- Completed exterior and common area upgrades: pool and barbecue area, clubhouse, fitness center, dog park, new paint and signage

- Renovated 52% of units, achieving rents 12% above underwriting

- Refinanced in August 2021, returning 60% of original capital

- Sold in December 2022 generated a 43% gross IRR and a 2.4x gross equity multiple

Industrial Outdoor Storage Portfolio ~ Nationwide

Active programmatic aggregation strategy of resilient IOS properties targeting high unlevered yields.

- Acquired 67 assets totaling $172 million of equity in generally off-market sourcing since 2023

- Average occupancy of 94% across portfolio

- Simple low capex business plans in high barrier to entry asset class

- $89 million dry powder available to continue growing portfolio amidst market portfolio sales of ~5-6%

Together, these projects highlight the through-line in Drake’s strategy: buying into inefficient situations, improving operations with the right local partners, and exiting into institutional demand.

We’re excited to dig deeper with the founding team on Wednesday, September 24th at 3pm EDT to discuss the evolution of Drake’s strategy, how they partner with operators, and where they see opportunities today.

Register here (for accredited & institutional investors only).

All Fund-level performance metrics are unaudited and calculated net of fees, carried interest and expenses, but gross of federal and state income taxes. Asset-level returns are presented herein gross of management fees, carried interest, income taxes (if applicable) and other fund expenses, the application of which would reduce such rates of return. These metrics represent the unaudited performance based on actual cash flows of each investment.

-Paul Stanton

Read next

Reinventing the Tribe: RidgeRunner and the New American Village

How a new model for rural communities built on shared identity is driving both demand and backlash

The Micro-Resort Capital Gap

Small, founder-led experiential resorts are achieving high occupancy and premium pricing, but they don’t fit traditional capital models.

The Moneyball Playbook for Multifamily Development

A data-driven approach to unit mix, layouts, amenities, and marketing helped one Gowanus Wharf project lease faster and at higher rents in a crowded market

Deep Dive: CERES & Culinary-Centric Residential Communities

How CERES is bringing the European “gourmet cluster” model to U.S. residential development, with food and culinary culture at the center of daily life