Who is Investing in Real Estate Tech? 2026 Edition

Our annual list of firms actively investing in real estate technology companies

Our annual list of firms actively investing in real estate technology companies

One week out, the people building the next generation of real estate assets are gathering in one room. Thesis Driven&

Exploring micro-multifamily investing with Groma in this week's Buy Box

There are over two million small multifamily buildings in America. Most have two to twenty units and line the streets of cities like Boston, Providence, and Chicago–the three-deckers, walk-ups, and triple-deckers that house millions of renters. Yet despite its scale, this asset class has been almost completely ignored by institutional investors, with fewer than 1% of these buildings being institutionally owned.

The reason is simple: small buildings are hard to buy, hard to renovate, and even harder to manage efficiently. They’re scattered across neighborhoods, often owned by individuals with limited capital and inconsistent upkeep. The result is a fragmented, underperforming slice of the rental market that remains stuck in a mom-and-pop operating model.

That’s the white space being tackled by Groma, a Boston-based real estate and technology company reimagining how small urban buildings are acquired, upgraded, and operated. Their proprietary AI platform, Grobot, transforms the economics of this overlooked category: sourcing properties in seconds, standardizing renovations through a consistent “Groma Grade” finish, and automating property management tasks that once required entire teams.

The company first proved its model through Groma Boston Growth Fund I: a 39-building, 136-unit portfolio that has delivered a ~20% IRR and 4% average annual distributions since 2020. In this Thesis Driven letter, we’ll break down:

According to the U.S. Census Bureau, roughly one-third of all rental units in the country are housed in 2- to 20-unit properties – more than two million buildings in total. Yet fewer than 1% are owned by institutional investors.

The reason has less to do with performance and more to do with friction. Small buildings are dispersed, idiosyncratic, and difficult to analyze in bulk (for example, each comes with its own heating system, roofline, and in-place leases). For a large fund, underwriting these assets one by one yields little economy of scale. And managing them is even harder: scattered locations, older infrastructure, and small rent rolls make it expensive to staff and maintain. The result is a market dominated by local owners–often individuals or family partnerships–who operate with limited capital and inconsistent maintenance standards.

That fragmentation has created a structural inefficiency that persists even in mature markets. Across comparable neighborhoods, small-cap multifamily assets typically trade at 150 to 200 basis-point higher cap rates than large, professionally managed apartment buildings. In plain terms, investors earn higher yields for properties sitting on the same blocks simply because they are smaller and harder to manage.

The disconnect looks like this:

“There are millions of small buildings in the U.S. that look and perform like institutional housing once you operate them that way,” said Seth Priebatsch, Groma’s co-founder and President. “The opportunity isn’t to reinvent real estate–it’s to apply modern systems to a market segment that larger investors ignore.”

At the same time, demand fundamentals remain strong. Housing supply in most urban markets continues to lag population growth, and the cost of homeownership has risen sharply with higher mortgage rates. Renters who might once have bought condominiums are staying longer, pushing occupancy levels near historic highs. In many metros, the rent-to-income ratio for Class B apartments remains well below that of large new developments, providing a cushion in downturns. These dynamics make the small-building segment one of the most resilient corners of the rental market–cash-flow-rich, locally diversified, and tied to essential housing rather than discretionary luxury.

“When you zoom out, micro-multifamily is a systems problem,” added Chris Lehman, Groma’s co-founder & Head of Research & Policy. “Fragmented ownership, inconsistent data, and manual workflows have prevented scale. Our job is to design infrastructure that lets efficiency compound across thousands of small assets.”

The pattern resembles what occurred in the single-family-rental (SFR) sector a decade ago. Before 2010, scattered houses were considered too operationally messy for institutions. Technology, standardized renovations, and scale changed that, transforming an informal asset type into a multi-hundred-billion-dollar industry. The same ingredients are now converging around micro-multifamily. Data accessibility, portfolio-level analytics, and new management platforms are beginning to remove the operational penalty that once kept institutions out.

For investors, micro-multifamily represents the newest opportunity to capitalize on an asset class and market that is hard to operate and fragmented–ahead of large institutional investment.

Turning micro-multifamily into an investable, repeatable business starts with solving three problems: how to buy, how to upgrade, and how to operate at scale. Groma’s answer is Grobot–an internal technology platform that automates the full property lifecycle and applies data feedback loops that compound across every building in the portfolio.

“Every property we add makes the next one easier to buy and operate,” says Priebatsch. “The software learns from each renovation and tenant interaction, so efficiency compounds with scale. The cumulative result is that small buildings–once considered too operationally inefficient for institutions–now perform like mid-scale multifamily assets.”

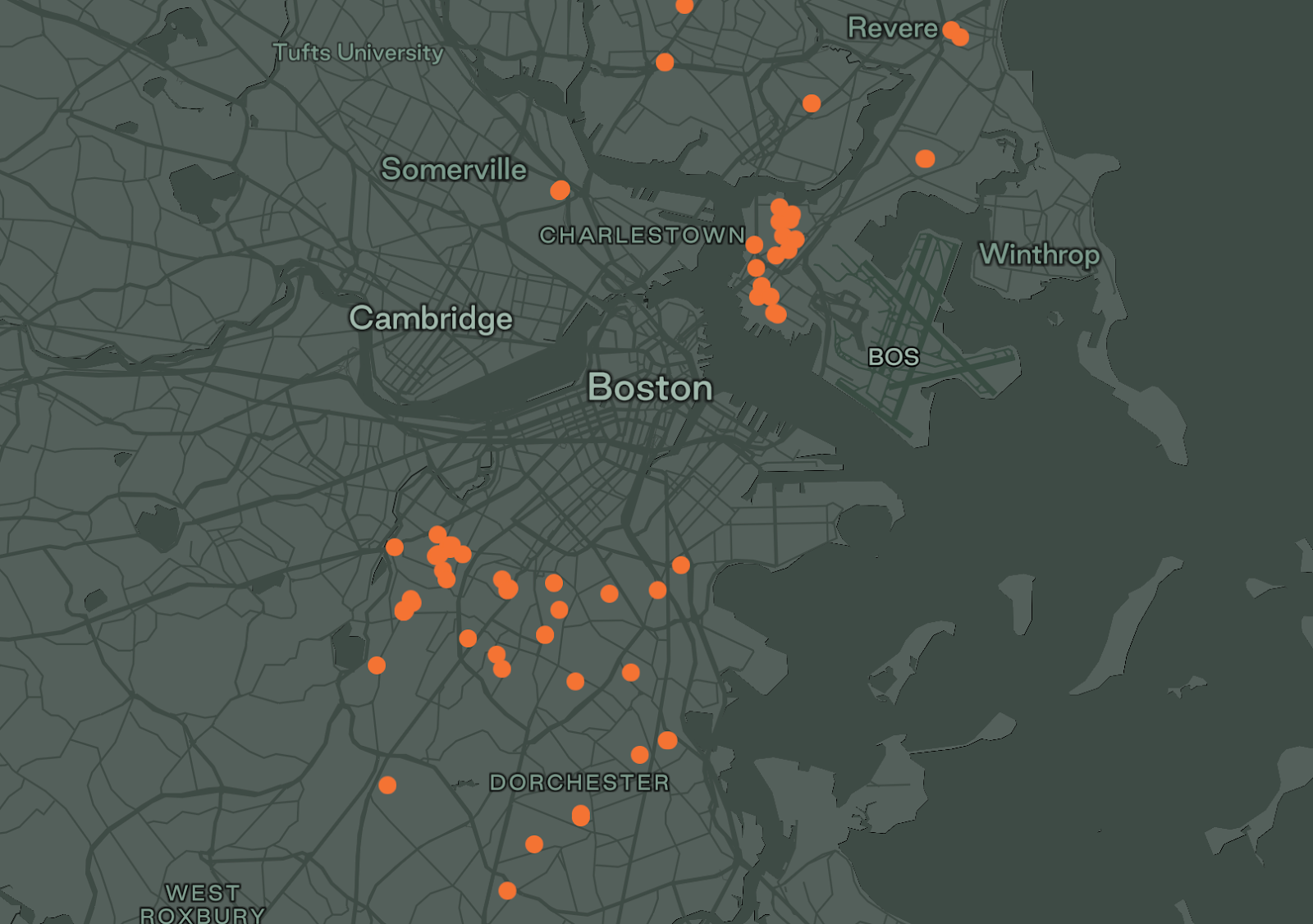

Before launching the Groma Real Estate Trust, the team tested its model in Boston through a closed-end vehicle called Groma Boston Growth Fund I.

The fund acquired 39 buildings totaling 136 units across neighborhoods such as Mission Hill, Dorchester, Roxbury, and Jamaica Plain between 2020 and 2021. The assets were small–typically three- to six-unit walk-ups–but collectively represented a proof of concept for how Grobot’s technology could perform in a live operating environment.

Fund I performance, at a glance:

Under prior ownership, properties of similar size in Boston typically operated with expense ratios between 45-50%. Groma’s standardized materials, centralized maintenance scheduling, and automated tracking have reduced that figure to roughly 30-32%. The resulting increase in NOI has allowed the portfolio to outperform regional averages even during a period of cost inflation and rising insurance expenses.

Representative outcomes include:

“Fund I proved that the constraint in operating micro-multifamily at scale wasn’t the asset class–it was the operating system,” says Lehman. “Now that the system works, the next step is to make it continuous, moving from a closed fund to a perpetual platform that compounds efficiency and data over time.”

The efficiencies achieved across 39 small buildings demonstrated that Grobot’s operating model could scale well beyond a single city. So rather than raise a series of discrete funds, Groma has used that data and infrastructure to form a perpetual investment vehicle–the Groma Real Estate Trust, which is designed to acquire, renovate, and manage small multifamily buildings across multiple markets.

The transition from fund to trust was largely structural:

Today, the Groma Real Estate Trust holds over 100 properties and roughly 550 units in Greater Boston, with plans to expand to new markets, like Providence, in the coming months.

Unlike most private funds, the trust’s structure is designed to provide flexibility and transparency. Shares are priced quarterly based on a net-asset-value (NAV) process undertaken in partnership with a third-party valuation firm, and redemptions are permitted on a limited, quarterly basis. Today, investors must be accredited, but the minimum commitment–$1,000–is far lower than typical institutional thresholds. And Groma is testing the waters to allow non-accredited investors as well in the near future. That combination of professional oversight and accessible entry point has attracted a mix of family offices, high-net-worth investors, and emerging wealth-management platforms seeking steady income with technological leverage behind it.

Future iterations will include tokenized share representations (“GromaCoins”) recorded on blockchain infrastructure and a “Rentvesting” program that enables residents turn some of their monthly rent into ownership in the Groma Real Estate Investment Trust. Both initiatives are designed to align incentives between the people who live in Groma properties and those who invest in them.

The first expansion market is Providence, Rhode Island, where smaller buildings account for nearly three-quarters of the multifamily inventory. With limited new supply, consistent rent growth, and cap rates in the “mid-6s”, Providence offers conditions similar to early-stage Boston, making it a natural next step in Groma’s effort to institutionalize the small-building segment.

For decades, efficiency in the real estate industry has been tied to scale–larger projects, larger checks, and larger teams. Because size was the only way to make operations economical.

Groma challenges that assumption by proving that efficiency can come from standardization and software rather than square footage. In most cities, small buildings make up the majority of the housing supply but remain disconnected from professional capital for operational, not economic, reasons. By applying data-driven underwriting, repeatable renovation systems, and consistent management, Groma blurs the line between “micro-multifamily” and traditional multifamily–potentially compressing the 150-200 basis-point cap-rate spread that separates small assets from institutional ones and unlocking both yield and appreciation in the process.

In other words, technology is the catalyst:

Together, these shifts turn fragmentation into scale. The same principles that institutionalized single-family rentals in the 2010s–data transparency, process discipline, and capital alignment–are now being applied to neighborhood-scale housing.

“Institutional real estate has always favored the big box,” says Lehman. “But the next wave of efficiency will come from connecting the small ones. Once data unifies the system, small buildings stop behaving like isolated assets and start functioning like a network.”

That network effect extends from operational efficiency to ownership itself. Groma’s roadmap includes tokenized shares (GromaCoins) and a Rentvesting program that allows residents to build fractional ownership over time. Both are designed to close the gap between the people who live in these buildings and those who fund them. If successful, the model could represent one of the first large-scale examples of participatory housing investment–a structure where renters, investors, and technology infrastructure share in the same long-term value creation.

For more deep dives on emerging real estate operators like Groma, explore Thesis Driven's Operator Spotlights and our workshops on capital markets strategy.

-Paul Stanton

Our annual list of firms actively investing in real estate technology companies

Predicting six new real estate marketplaces to rise over the next decade

As AI eliminates administrative burden and capital consolidates around scaled platforms, operational performance is becoming a primary driver of returns

How a new model for rural communities built on shared identity is driving both demand and backlash

Covering the future of real estate and the people creating it