The Deals Developers Are Analyzing Today | Q2 2026 Edition

A quarterly read on early-stage feasibility activity with our friends at TestFit

A quarterly read on early-stage feasibility activity with our friends at TestFit

We're going long on print. This October, we are releasing the first edition of Thesis Driven in physical

The below-the-surface assessments of a handful of powerful firms influence borrowing costs, capital flows, which deals get financed—and which don't

In the post-Global Financial Crisis (GFC) blame game, there were no shortages of villains. While markets may have expected a high degree of risk-taking and aggression from bankers and hedge funds, it came to light that rating agencies, the third parties tasked with assigning objective risk scores to debt securities, had themselves gotten caught up in speculative fervor.

Firms like S&P Global, Moody’s, and Fitch—once regarded as the market’s sober arbiters—were suddenly cast alongside the financial engineers who pushed finance to its breaking point. The crisis revealed principal-agent problems and misaligned incentives that undermined the credibility of credit ratings.

Confidence in the agencies themselves was shaken—yet their role in the system proved far harder to replace than many expected. Nearly two decades later, these firms remain essential infrastructure for commercial real estate finance.

A paradox has emerged: sophisticated investors know ratings are imperfect and conduct their own analysis, yet the market as a whole still depends on them to function. They provide a common language that allows capital to flow efficiently across a fragmented marketplace. Without them, transaction costs would be prohibitive, since every buyer would need to independently underwrite every loan, making large-scale capital formation in CRE far more difficult.

CMBS (Commercial Mortgage-Backed Securities) are once again playing an outsized role in commercial real estate markets. According to S&P Global, CMBS issuance increased 24% in 2025. S&P notes that the increase would have been even more substantial were it not for the uncertainty and volatility wrought by “Liberation Day,” Trump’s tariff rollout in April of last year. That means rating agencies have a direct impact on the availability and cost of capital, and therefore on how commercial real estate is priced and financed.

But what role do they really play in the market?

Not every real estate project uses the CMBS market, but CMBS ratings, and the resulting interest rates ripple through the ecosystem. In practice, they steer capital toward certain property types, geographies, and deal structures—shaping which projects are financed, refinanced, or ultimately brought to market.

In this letter we’ll explore:

Fundamentally, CMBS can be thought of as a form of bond, but one backed by many different underlying borrowers. Property loans are bundled into a trust that issues bonds to investors. Cash from loan payments flows through a “waterfall,” in which senior bonds (AAA-rated) are paid ahead of other tranches and protected by subordination—meaning junior bonds below them absorb losses first. If loans default and properties are foreclosed, losses eat through the structure from the bottom up, shaping how investors price risk in commercial mortgage debt.

A AAA bond might have 30–40% subordination, meaning that percentage of the pool would need to be lost before the senior bond loses a dollar. A BBB bond might have only 10% subordination, sitting closer to potential losses.

This waterfall structure creates a risk-return spectrum: senior bonds offer stability and lower yields, while junior bonds provide higher returns in exchange for absorbing losses first, reflecting the different levels of risk investors are willing to price.

The CMBS ratings market is dominated by a handful of major agencies, with Morningstar DBRS, S&P Global Ratings, Moody's, Fitch Ratings, and Kroll Bond Rating Agency (KBRA) serving as the primary evaluators of commercial mortgage-backed securities. Their ratings determine how bonds are priced, who can buy them (many institutional investors face regulatory restrictions on below-investment-grade securities), and ultimately whether a CMBS deal can come to market at all. Most transactions receive ratings from at least two agencies so investors can compare different views of risk.

The rating process begins with detailed, loan-level analysis rather than broad statistical modeling.

Agencies like Morningstar DBRS emphasize property-specific fundamentals, essentially re-underwriting each loan from an investor's perspective. They construct cash flow projections for every property in the pool, stress-testing the numbers under various adverse scenarios such as occupancy declines, rent reductions, and rising operating expenses—all of which directly affect debt service coverage and refinancing risk.

This is an important caveat to ratings; they are intended to reflect the likely losses at differing levels of stress, not the overall health of the underlying property or market. In both the GFC and the post-pandemic period, the source of stress was not properly modeled. In the GFC, the magnitude of home price declines was simply not a scenario any of the models had considered. Similarly, the impact on offices from the COVID shutdown and the work-from-home trend could not be foreseen, and bonds that had been reasonably given AAA ratings were suddenly at risk from an entirely exogenous real-world development.

Nonetheless, rating agencies calculate two critical metrics for each loan: the probability of default over the loan's life and the loss severity if default occurs.

Loss severity depends heavily on loan-to-value ratios, but agencies don't simply accept the original appraisal. They derive current market values based on their sustainable cash flow estimates and market-appropriate capitalization rates, which can differ substantially from origination values, especially as market conditions shift.

Once individual loans are analyzed, agencies model how losses would cascade through the CMBS structure using Monte Carlo simulations that run thousands of scenarios. Since bonds are tranched, agencies determine how much loss each tranche would experience at different rating levels. An AAA-rated bond should withstand severe stress with minimal loss, while lower ratings accept progressively higher loss potential, which investors reflect in pricing.

The process doesn't end at issuance. Rating agencies continuously monitor loan performance, property fundamentals, and market conditions throughout the bond's life. When loans show distress signals—such as declining occupancy, falling revenues, or missed payments—the agencies update their default probability and loss severity estimates, potentially triggering rating downgrades.

The underlying structure of CMBS tells only part of the story about its relative attractiveness compared with other forms of debt financing. Bank loans typically offer a lower rate and have more sponsor-friendly prepayment terms, but underwriting standards and loan-to-value ratios have both gotten considerably tighter. Insurance lenders may be the holy grail, providing lower-cost long-duration financing, but those lenders require huge deal sizes to make the economics work, limiting access for many CRE sponsors.

CMBS, by contrast, attracts borrowers who value execution certainty and competitive pricing over relationship flexibility. The market has traditionally served middle-market real estate investors and sponsors who own stabilized, income-producing properties but lack the balance sheet strength or banking relationships to access portfolio loans from life insurance companies or commercial banks.

These borrowers often prioritize non-recourse financing that releases them from personal liability if the property underperforms. CMBS lenders readily provide non-recourse loans since the debt is typically sold into securitization, unlike banks that require personal guarantees or full recourse—a structural difference that can materially affect sponsor risk and project underwriting decisions.

Crucially, CMBS financing often has punitive prepayment terms or requires defeasance—a method of effectively replacing the income from the property with income from Treasuries when a borrower refinances or prepays. That means sponsors do not necessarily benefit from a fall in interest rates, which can influence hold periods and exit timing for CRE assets.

The 2008 financial crisis and subsequent Dodd-Frank regulations fundamentally reshaped the CMBS market. Risk-retention rules now require loan originators to hold 5% of every securitization, aligning their interests with investors but increasing capital requirements and reducing lending capacity—which in turn constrains the volume and pricing of debt available to certain CRE projects.

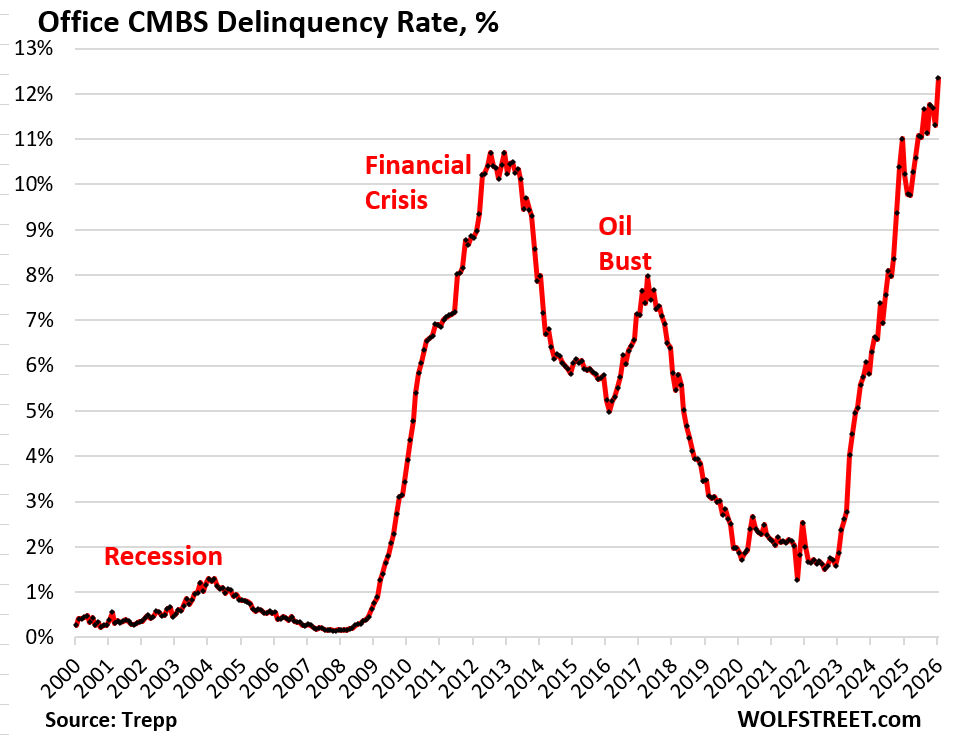

The transparency of CMBS means it is often used as a more real-time barometer of commercial real estate market health. But CMBS data reflects only a subset of the market and can present a skewed picture if viewed in isolation.

Recently, CMBS delinquency rates reached an all-time high of 12.3%, yet real estate prices have not suffered anywhere near the dramatic collapse of 2008 or the dislocation of COVID. This demonstrates that CMBS is a snapshot of a subset of a larger market, not the “canary in the coal mine” that drives bearish sentiment and catastrophic headlines. It’s one signal among several that investors use to interpret CRE pricing trends.

Credit investors and sponsors view CMBS ratings through fundamentally different lenses, reflecting their opposing positions in the capital structure and divergent economic incentives—differences that ultimately influence how capital is priced across the CRE market.

For credit investors in senior tranches, ratings serve as essential due-diligence shortcuts and regulatory gatekeepers. Institutional buyers such as pension funds, insurance companies, and money market funds often have mandates limiting them to investment-grade securities, so the difference between BBB- and BB+ can determine whether a bond is eligible for purchase at all.

These investors rely on ratings to quickly assess relative value across deals without conducting full loan-level underwriting themselves—though sophisticated buyers often supplement agency ratings with their own analysis. Senior bondholders generally trust that AAA and AA ratings provide sufficient subordination cushion to protect against all but catastrophic scenarios, focusing more on yield spread and liquidity than granular property fundamentals. They're buying ratings as much as they're buying bonds, a dynamic that can influence borrowing costs for the underlying properties.

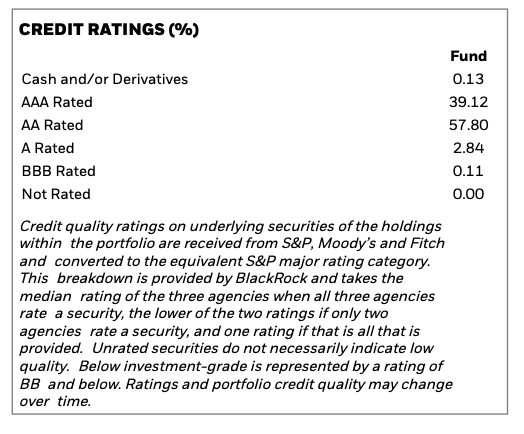

Take, for example, the iShares CMBS ETF, which aims to track a broad index of CMBS. The portfolio is overwhelmingly AAA and AA rated securities. The ETF is a mechanical buyer of highly rated bonds, and money market funds and the growing pool of insurance capital are in the same boat. This strong bid from mechanical buyers drives the cost of capital down for top-rated issues, reinforcing the pricing advantage of highly rated CMBS across the broader CRE lending market.

Mezzanine and junior investors take a more skeptical view. Josh Nester, a portfolio manager at a CMBS-focused hedge fund Polpo Capital, says, “We look at every loan from the bottom up, regardless of rating.”

Firms like Polpo recognize that rating agencies apply conservative assumptions that may not reflect actual performance, creating opportunities where bonds are "overrated" relative to true risk. These investors conduct independent underwriting, often disagreeing with agency loss projections and believing they can identify mispriced risk. For BB and B buyers, the rating is a starting point for negotiation and pricing, not gospel.

Sponsors and borrowers view ratings primarily as a cost of market access rather than meaningful risk assessment. They need strong ratings to achieve efficient execution—better ratings mean tighter spreads and lower all-in borrowing costs, which can materially impact the feasibility of a project.

Typically, sponsors work closely with rating agencies during the pre-sale process, sometimes structuring deals specifically to achieve desired ratings, whether through additional credit enhancement, loan modifications, or strategic pool composition. The relationship can become adversarial when agencies demand changes that increase costs or reduce proceeds, particularly when those changes affect leverage or execution timing.

Borrowers work to engineer high ratings to lower their cost of capital by tapping into large capital flows from passive buyers, while many active investors treat ratings as only a starting point for their own analysis. The result is that ratings are less a precise measurement than a shared shorthand the market relies on.

Investors, both active and passive, use ratings to communicate high-level portfolio breakdowns to their LPs and stakeholders. A pension fund can efficiently report "85% investment-grade exposure" without explaining the underlying loans in each position. Borrowers use ratings to signal deal quality and market their transactions. "AAA-rated senior notes" convey legitimacy and attract capital.

The 2008 crisis exposed the dangers of over-reliance on this system, but it didn't produce a viable alternative. Regulatory reforms increased scrutiny and tightened standards, yet the fundamental structure of issuers paying agencies to rate their deals remains intact.

This ultimately creates a productive tension: rating agencies exert enormous influence over capital allocation in commercial real estate, while sophisticated investors treat their assessments as inputs rather than conclusions.

Ratings simultaneously constrain and enable capital flows. They impose discipline by establishing baseline risk expectations that borrowers must meet. At the same time, they create opportunities for alpha generation by investors who believe they can assess risk more accurately than the agencies. That interplay is one of the forces that keeps the CRE debt market functioning.

And this balance is particularly critical today as the CRE market faces structural headwinds. The work-from-home paradigm has permanently shifted office demand patterns, creating winner and loser properties. Interest rates have risen sharply, testing debt service coverage ratios. Retail properties face ongoing e-commerce competition.

In this environment, the ability of ratings to differentiate among properties that have durable fundamentals and those that face structural challenges determines which borrowers can raise capital and at what cost. Overly broad or compressed ratings that fail to distinguish between prime and secondary assets create perverse incentives and misallocate capital.

Moreover, ratings serve as the primary communication mechanism by which market risk gets priced across the CRE landscape. Even borrowers who never access the public securitization market are indirectly affected by CMBS ratings because those ratings influence how banks and insurance companies price their own loan products.

A downgrade to office CMBS in a particular submarket signals diminished fundamentals that cascade through all debt pricing in that area. Conversely, ratings improvements unlock cheaper capital. This means the direction of ratings, and the trend upward or downward, has profound implications for which asset classes and geographies attract capital investment and which face funding constraints.

Ratings must be imperfect enough to allow market participants to disagree and deploy capital based on differentiated views, yet reliable enough that institutions can use them as operational shortcuts and market signals remain valid. Lose that balance, and the market begins to move on distorted signals rather than real fundamentals.

When this tense equilibrium holds, the CRE market can price risk, adjust to new realities, and recover from shocks. When it doesn’t, capital misfires.

Falling birth rates, shifting migration, and an aging population are already reshaping demand across real estate, faster than most of the market has priced in

How a generation of superstar chefs and obsessed diners remade urban neighborhoods, inflated rents, and priced themselves out of the streets they made desirable.

How autonomous vehicles will break the economics of convenience retail

Stacks of documents, repetitive workflows, and massive economics make mortgage lending an obvious target for AI, but adoption has been slow.

Covering the future of real estate and the people creating it