The Deals Developers Are Analyzing Today | Q2 2026 Edition

A quarterly read on early-stage feasibility activity with our friends at TestFit

A quarterly read on early-stage feasibility activity with our friends at TestFit

We're going long on print. This October, we are releasing the first edition of Thesis Driven in physical

Which deal types are getting funded, which LP relationships are holding, and what real estate GP capital markets actually look like right now.

Hat tip to our friends Jennifer Wenzel & George Zhang (Texas Teachers) and Baylor Miller Daggmill (Alliance Global Advisors) for their work in this PREA piece which helped immensely in writing this letter.

| “You Americans are so f*cking entrepreneurial.”

This half-amused quote came from a recent call with a large, India-based real estate developer. They were referring to the U.S. real estate capital markets–specifically the emerging standardization of “GP investing” and how “we Americans” always seem to find new ways to generate alpha in the hardest of environments.

And it’s true. American investors are relentlessly creative when it comes to finding new ways to outperform the market. In a real estate market environment where compressed asset level returns have left many investors bored and on the sidelines over the past 24 months, creative capital seeking higher octane returns have begun moving upstream—from owning properties to owning the platforms that own them.

These investments into and alongside GPs are not new, but they are evolving. And they’re introducing a variety of new terms and concepts that–until recently–lacked consistent definition:

These structures all offer a share of the GP promote (and sometimes fees) alongside traditional LP economics on the invested capital, creating a blended return profile that can look more like 3-8X MOIC rather than the 2-3X typically targeted by traditional value add and opportunistic LP returns.

But while investor interest is accelerating, most GPs aren’t yet prepared to capture it. Few have standardized terms, articulated growth strategies, or built the reporting and governance frameworks these investors now expect.

In this Thesis Driven letter, we’ll break down:

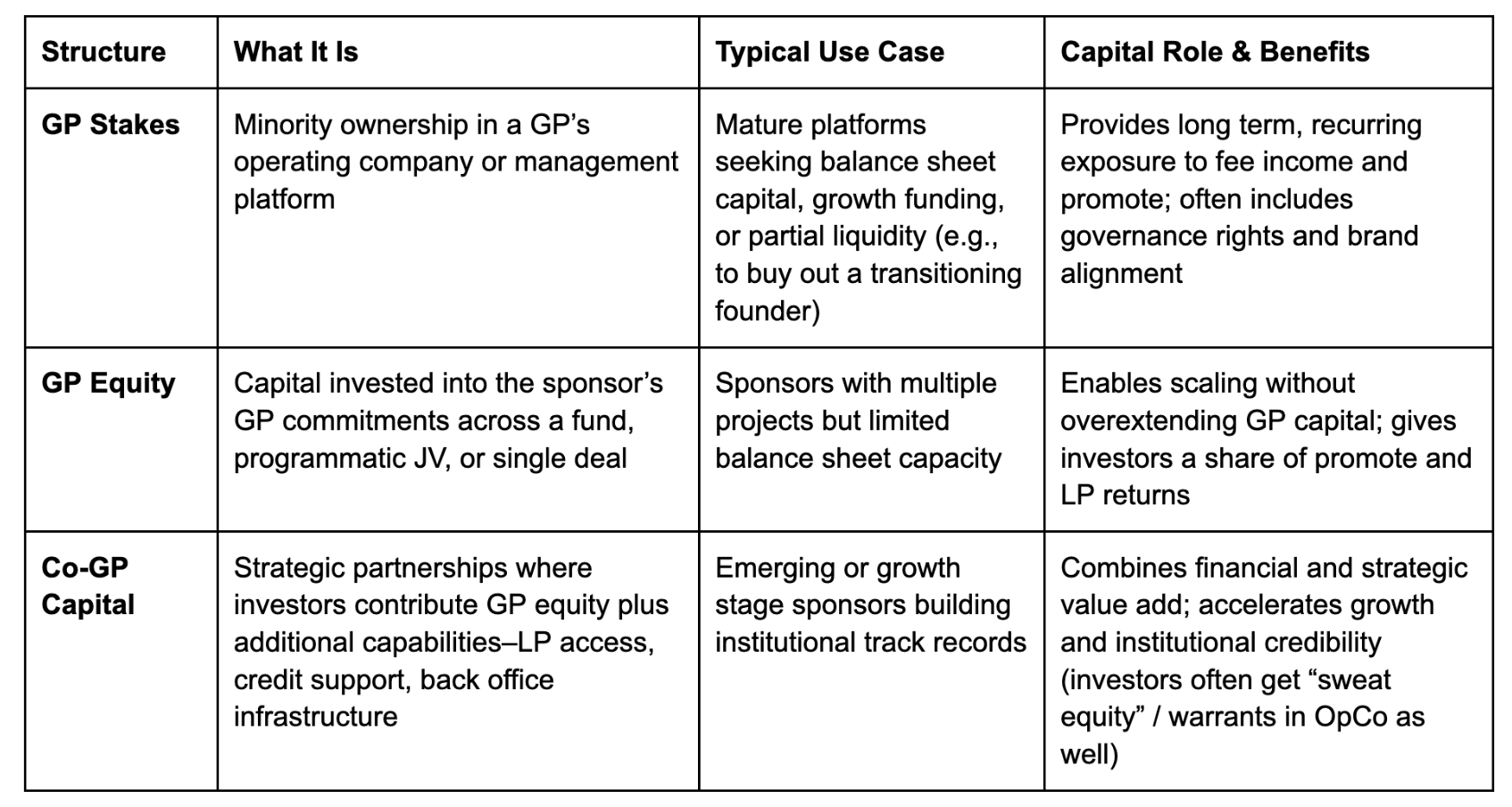

As investors move upstream–from owning assets to owning the platforms that buy & develop them–the first step is understanding the different ways capital can engage with a GP. While the term “GP investment” gets used loosely, it actually spans a spectrum of structures that vary widely in purpose, risk, and return profile.

At one end are GP stakes, where investors buy an equity piece of the sponsor’s operating company or management platform (like an investment in any other private company). At the other are co-GP partnerships, where investors join at the deal level, taking an active role in execution. Between them sits GP equity, a flexible structure that funds a sponsor’s GP commitments across multiple projects or funds.

Here’s a simplified view of the landscape:

Each of these models represents a different way to participate in the economics of a GP, primarily by sharing in fee income, promote, and enterprise value growth. But their risk profiles vary. GP stakes offer steady, annuity-like exposure to management fees, while co-GP structures are more deal-driven and performance-dependent.

Importantly, these aren’t mutually exclusive. A platform might use GP equity to fund its commitments today, then sell a GP stake later to institutionalize its balance sheet or provide liquidity to founders. Likewise, a co-GP partnership might evolve into a platform-level joint venture once the relationship and track record are proven.

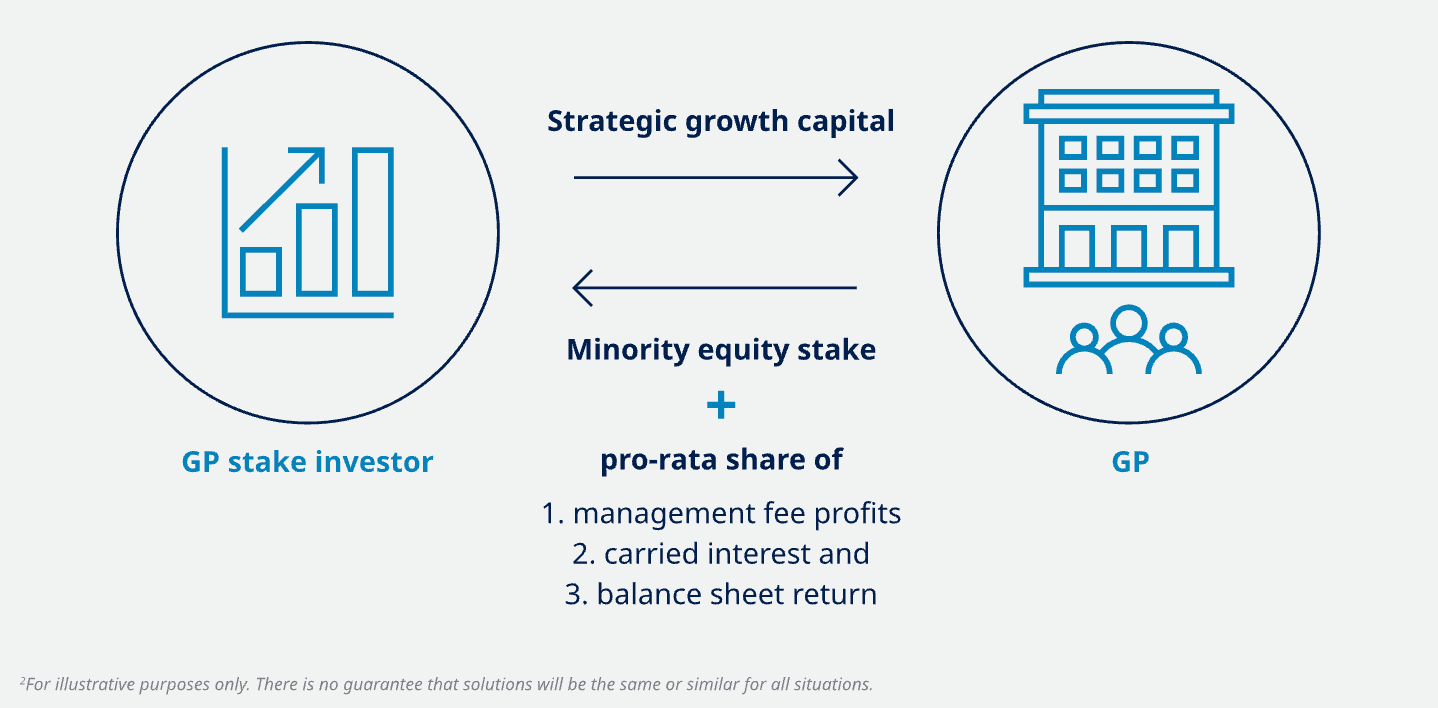

Visual of GP Stakes Model (Source: Blue Owl)

That evolution is part of what makes the GP layer so interesting right now: it’s not a single asset class–it’s an ecosystem of investment structures that can be stacked in different ways. And as the market begins to formalize these structures, investors are learning how to price risk, underwrite enterprise value, and create liquidity in what used to be a purely private, relationship-driven corner of the market.

As the GP investment ecosystem matures, it’s drawing interest from a diverse mix of capital sources, each with its own motivations, risk tolerance, and definition of success.

What unites them is the recognition that value is migrating from the property level to the platform level. But how that value is captured depends on who’s writing the check.

Institutional PERE Funds

Large PERE groups were the first to professionalize GP stakes investing. Specialized platforms like Petershill Partners, Bonaccord Capital Partners, and Wafra now raise dedicated vehicles to buy minority interests in real estate managers.

Their theses are pretty simple: recurring fee-related earnings (FRE) and carried interest participation can provide durable, long duration cash flow that behaves more like private equity than real estate.

These investors typically target mature GPs with institutional AUM, stable fund franchises, and governance infrastructure already in place. They bring permanent capital, brand association, and distribution reach–but require transparency, reporting discipline, and succession planning in return.

Family Offices

Family offices have become the most active new entrants into the GP investment space. They’re increasingly funding GP equity and platform-level growth capital for operating sponsors–often because their own wealth was built by buying or building operating companies. That background typically makes them more comfortable underwriting a business or platform than a single real estate asset.

They’re also drawn to the control, alignment, and strategic influence that GP investments provide. And with longer investment horizons and fewer institutional constraints, family offices are often better-suited partners for growing GPs than traditional institutional capital.

For many, these investments represent a hybrid between direct real estate ownership and private equity venture: tangible assets below, scalable enterprise above.

Entrepreneurial Co-GP Allocators

A new cohort of mid-sized sponsors and investment entrepreneurs is emerging as co-GP capital. They bring not just money, but LP relationships, balance sheet strength, and operational resources–effectively acting as accelerators for new or growth stage platforms.

In these partnerships the emerging operator or developer gains credibility, deal capacity, and access to institutional LPs; while the co-GP gains upside participation and early stage enterprise optionality. The trade-off is shared control, shared governance, and shared promote.

The typical profile of these entrepreneurs is a senior real estate private equity professional with established LP relationships who wants to build something more entrepreneurial. They’ll often partner with four to five operating platforms, bring a different LP base to each strategy, and build a personal track record with partial control of these vehicles–ultimately positioning themselves to raise a larger discretionary fund and scale the platforms that prove most compelling.

High Net Worth Investors

At the earliest end of the market are high net worth individuals (HNWIs) and small syndicates. They typically provide deal-by-deal GP equity or seed capital for first-time sponsors–often backing entrepreneurs they know personally. While their checks are smaller, their impact on the ecosystem is outsized as they help managers build track records and proof of concept that unlock larger capital later.

Looking ahead, we expect to see a growing network of “real estate angels”–these HNWIs willing to take early GP risk in exchange for asymmetric upside–as GP investment opportunities and return profiles become better understood and more widely standardized.

For operating sponsors, the rise of GP-level investing represents an invitation to rethink what their business actually is and how it gets valued.

Historically, real estate GPs–especially operators & developers–have not thought much about the enterprise value of their operating company, i.e., how their fee streams & promotes would be valued in an acquisition by a third party.

But as a larger market emerges for strategic acquisitions based on FRE, successful GPs in the coming cycle will probably look less like project aggregators and more like platforms–scalable enterprises that combine people, process, and brand into a repeatable engine for value creation.

For example, a sponsor who can show a recurring 1-2% asset management fee stream on $500 million of AUM, outline a path to double that AUM within three years, and demonstrate the scalability of overhead and team capacity is suddenly speaking the same language as private equity investors. Those predictable fees become the foundation for valuing the business itself–often trading at 8-12X FRE in institutional GP stakes transactions.

Why GPs Are Attractive Now

For established fund managers, GP stakes capital can provide balance sheet strength to pursue new strategies, seed new funds, or create internal liquidity.

Example: A $2 billion multifamily fund manager sells a 20% GP stake to an institutional investor at a 10x multiple on fee-related earnings, using the proceeds to seed a new credit platform. The investor receives a share of recurring management and performance fees and a board observer seat for oversight.

For emerging operators and developers, GP equity or co-GP capital can fund the “missing middle”–the 5 to 10 percent of GP commitments that limit growth.

Example: A regional build-to-rent developer raising a $200 million joint venture brings in a family office to fund its 10% GP commitment. In exchange, the family office earns a proportional share of promote economics and receives approval rights over material partnership decisions.

And for newly formed platforms, strategic co-GP partners can offer credibility, structure, and distribution that accelerate the path to institutional readiness.

Example: A first time industrial outdoor storage operator partners with a seasoned co-GP who contributes GP equity, introduces institutional LPs, and provides accounting and asset management infrastructure. The co-GP receives a preferred return on capital plus a negotiated share of promote once the platform scales.

Yet capturing this capital requires more than a strong deal pipeline. Sponsors need to present themselves as investable businesses: with standardized economics, documented track records, and transparent governance. In other words, investors aren’t just evaluating assets–they’re underwriting teams, systems, and strategy.

As investors move up the capital stack, sponsors need to meet them there.

That means learning to think–and communicate–like a company that can be valued, not just execute deals. The GPs that attract institutional, family office, or strategic GP investments aren’t necessarily the biggest; they’re the ones that have learned how to tell their story through the lens of enterprise value.

The most important shift is mindset. Many sponsors have built impressive track records but have never formalized what makes their platform investable. GP investors are looking for platforms with scalable processes, transparent governance, and predictable economics—where fee streams, promotes, and balance sheet income form a coherent business model rather than a patchwork of transactions.

At the heart of this is the ability to clearly articulate fee structures and growth visibility. Investors want to understand:

Sponsors that can show a clear path to expanding recurring fee income–by growing AUM, adding new strategies, or layering new operating capabilities–create the transparency that GP investors need to underwrite future value. So the ability to explain your “fee story” in concrete, defensible terms is becoming as important as explaining your development pipeline or IRR assumptions.

Equally important is structure and alignment. Investors want to see governance frameworks, incentive systems, and promote waterfalls that ensure teams stay motivated and capital stays protected. Small but important decisions to highlight as well are vesting promote, capping preferred returns, and how you’re standardizing co-GP terms.

Finally, sponsors must build visibility. The most investable GPs will be the ones that communicate a clear thesis and demonstrate domain authority through thought leadership–via traditional marketing materials as well as social channels (e.g., Linkedin, Substack), content-focused learning opportunities (e.g., webinars, roundtables) and more evolved IR functions (e.g., adding videos & case studies to investor email campaigns & newsletters).

While still in its early innings, the GP investment market is maturing fast. What began as a handful of opportunistic balance sheet deals is becoming a defined capital markets ecosystem with its own language, valuation conventions, and investor classes. Over the next decade, expect GP investing to evolve from a creative niche into a mainstream asset class via:

1. Standardization and Liquidity

We’re already seeing GP-level terms–carry splits, preferred returns, and governance rights–begin to standardize across transactions. As more groups like Texas Teachers and Alliance Global Advisors publish frameworks, underwriting methodologies are converging. This standardization is the prerequisite for the next step: liquidity.

Secondary platforms and continuation vehicle markets will eventually allow investors to trade minority GP interests, just as LP stakes trade today. Once that happens, capital will flow faster, valuations will stabilize, and the GP layer will feel less like venture and more like private equity.

2. Hybridization of Managers

Boundaries between “fund GPs” and “operator GPs” will continue to blur. Developers are launching discretionary vehicles; institutional managers are acquiring operating companies; family offices are seeding verticals that combine both. The winners will be the ones who can integrate OpCo-PropCo models–tying together operations, technology, and real estate capital into cohesive ecosystems that generate both yield and enterprise value.

3. The Rise of Private Wealth Capital

Family offices, RIAs, and HNWIs are quickly professionalizing their approach to GP investing. Expect the emergence of “GP investment clubs” and syndicate vehicles that pool smaller checks into platform-level opportunities. Technology platforms and data transparency will accelerate this trend, giving private wealth investors access that’s been traditionally reserved for institutions.

4. Technology and Brand as Multipliers

As more capital competes to back GPs, differentiation will hinge on two things: data and brand.

Sponsors that use technology to streamline reporting, manage investor relations, and drive operational insight will command premiums. So will those that build visible, trusted brands through content, community, and transparency.

5. Consolidation and Exit Paths

Finally, as the market deepens, expect roll-ups, mergers, and strategic acquisitions among GPs. Just as asset management platforms consolidated in the 2000s, today’s fragmented operator universe will begin to cluster under larger, diversified banners seeking scale, distribution, and liquidity.

The bottom line: GP investing is no longer a niche idea. It’s becoming a natural next step in how real estate capital markets evolve. The most valuable firms in the years ahead won’t just own properties; they’ll build and manage the platforms that create outsized value in those properties, programmatically. So the sponsors who start thinking this way now–treating their business as an investable enterprise & brand–will be best positioned to grow and attract the capital shaping the next generation of real estate platforms.

For more on positioning your platform for GP-level capital and the LP relationships that fund it, join Thesis Driven's Raising Capital from Large Real Estate LPs workshop or explore the full workshops library.

-Paul Stanton

How a new model for rural communities built on shared identity is driving both demand and backlash

Small, founder-led experiential resorts are achieving high occupancy and premium pricing, but they don’t fit traditional capital models.

A data-driven approach to unit mix, layouts, amenities, and marketing helped one Gowanus Wharf project lease faster and at higher rents in a crowded market

How CERES is bringing the European “gourmet cluster” model to U.S. residential development, with food and culinary culture at the center of daily life

Covering the future of real estate and the people creating it