Who is Investing in Real Estate Tech? 2026 Edition

Our annual list of firms actively investing in real estate technology companies

Our annual list of firms actively investing in real estate technology companies

One week out, the people building the next generation of real estate assets are gathering in one room. Thesis Driven&

Inside Left Lane’s strategy transforming distressed offices into boutique hospitality assets across America’s growth cities

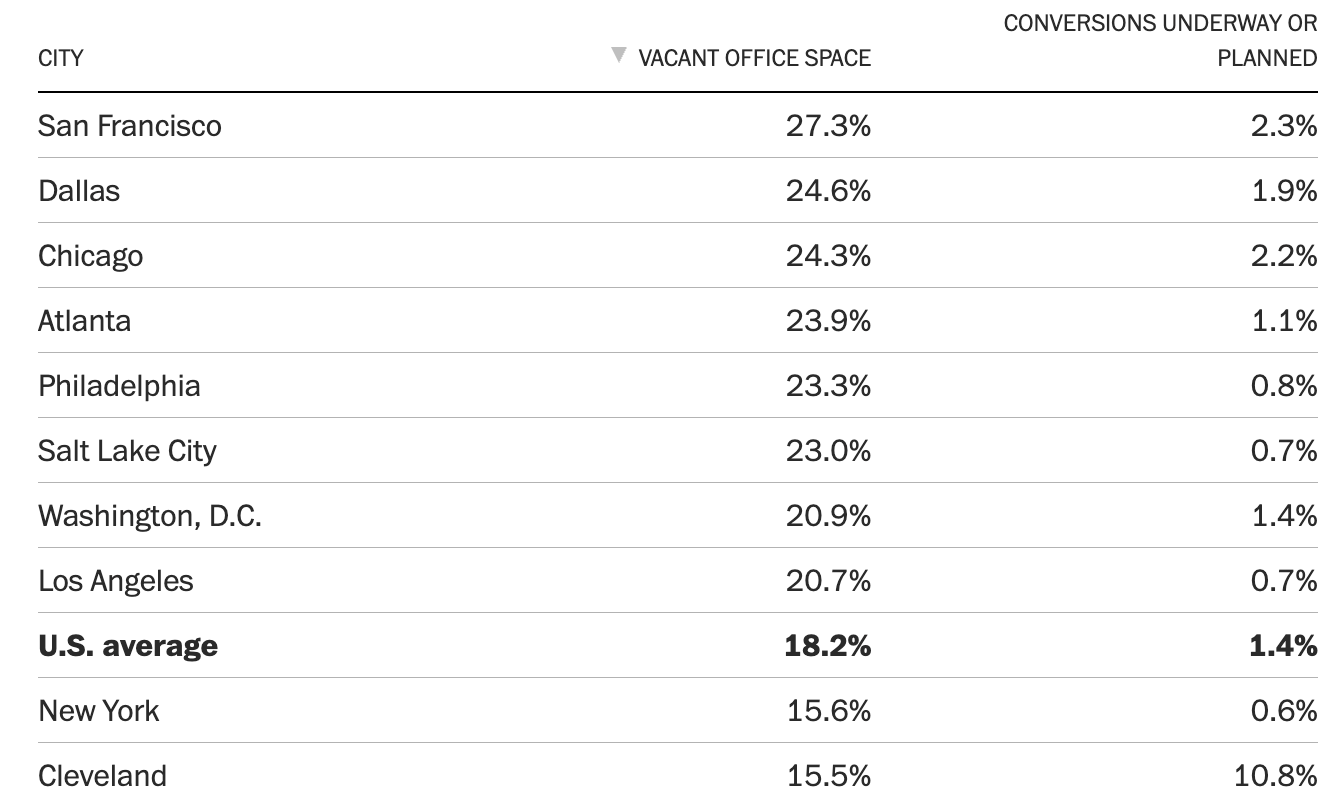

When 2020 headlines first flashed the collapse of the office market, the response from the investment community was enthusiastic: “This is it–the generational adaptive reuse moment!”

Analysts sketched out endless conversion scenarios:

If a building had four walls and a roof, someone had a slide explaining how it could become the next hot asset class. Values were plunging and lenders were panicking–setting the stage for creative developers to buy broken office buildings cheaply, then turn them into something new.

But fast forward five years and that hasn’t really happened. Once investors got past the headlines and into the floorplates, they discovered a more sobering reality: very few office buildings can be converted economically. The wrong shape. The wrong depth. The wrong windows. The wrong zoning. The wrong demand story.

The theoretical “conversion wave” shrunk as teams realized how narrow the viable universe actually was. But over the past five years, a small number of groups have been able to capitalize, matching the right distressed acquisition strategy with the right operating model.

Among them is Left Lane Development, a NYC-based, vertically integrated developer and hospitality operator that has targeted a buy box to acquire distressed, historic office buildings in walkable districts of high-growth secondary markets–like Savannah & Pittsburgh–with the architectural bones to become luxury boutique hotels and residences. Then, they layer on a full-stack operating model capable of converting, positioning, and running those hotels as luxury properties.

It’s a story that is rare in today’s environment: charismatic real estate generating high returns with minimal entitlement and execution risk. This letter breaks down how they’re doing it:

When remote work emptied commercial corridors and refinancing challenges piled up, analysts began modeling everything from office-to-apartments in Midtown Manhattan to office-to-data-centers in Cincinnati. Dozens of conference panels and white papers promised a once-in-a-generation buying opportunity.

But once detailed underwriting began, the theses narrowed fast, and we learned most office assets simply don’t transfer.

Too deep a floorplate, and layouts stretch guests or residents too far from natural light. Too many structural columns, and demolition to reconfigure space makes the economics fall apart. Mechanical systems and facade conditions often require costly replacement. And in many cities, zoning remains optimized for a monoculture of workers who are no longer there.

In short: distress alone doesn’t create feasibility. For an office building to convert efficiently, several conditions need to align. And they are more practical than theoretical:

Only a small portion of the distressed office buildings in the U.S. meet this physical criteria for feasible conversion. The ones that do are typically older, pre-war structures designed around access to natural light (before office economics shifted toward larger, deeper floorplates optimized for desk density). These buildings have character and proportion that work better for human-scale uses than for contemporary office layouts.

Geography narrows the field further. In cities such as Savannah, Pittsburgh, Providence and Phoenix–places experiencing population and visitation growth–downtown office stock is often both under-utilized and architecturally compatible with alternative uses. These are environments where more people are spending time, but fewer are doing so inside traditional office space.

The combination creates a clear mismatch: many of the office buildings no longer serving their original purpose are located exactly where demand is emerging for different types of activity–not just during the workday but into evenings and weekends.

That dynamic creates a narrow category within the broader distress (call it “small-scale historic office”) where conversion isn’t about stretching for yield or creativity for its own sake–it’s simply the most economically rational path forward.

Once you narrow the universe to buildings that physically can be converted, the next question is whether they should be, i.e., the economics support the investment. That is where most office conversion strategies fail. It’s also where a few succeed.

A look at the creation of a families-only Dallas country club

Alpaca Real Estate is building private equity with AI at the core. How the platform works and what it signals for the asset class.

The opco-propco opportunity in Tier 1 purpose-built student housing

Exploring micro-multifamily investing with Groma in this week's Buy Box

Covering the future of real estate and the people creating it